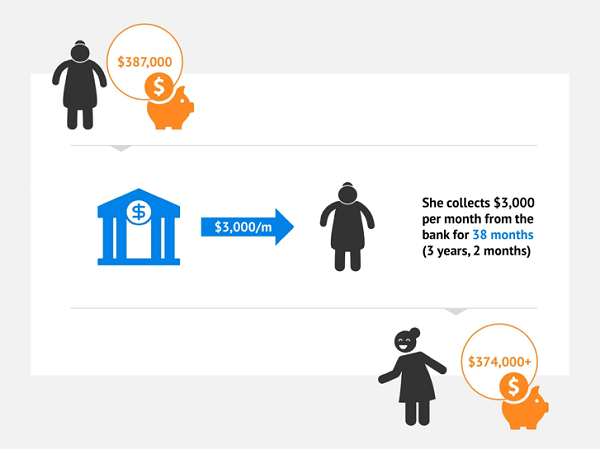

Three years ago, he explained how he was using my “retire on monthly dividends” strategy to help this nice grandmother.

“She brought me $387,000,” he told me originally. “And wants to take out $3,000 per month for ten years.”

Well, so far, so good for grandma. She’s now 38 months into her $3,000 per month dividend gravy train. To date, she’s taken out a fat $114,000 in spending money.

And that nest egg? Well, it’s still going strong. She’s still sitting on more than $374,000 after three-plus years and $114,000 worth of withdrawals.

Grandma’s Monthly Dividend Gravy Train

Her fat dividend check shows up every 30 days, neatly coinciding with her modest living expenses. And her portfolio holds many monthly dividend payers, dishing income that adds up to 6%, 7% and even 8% or more per year.

What if you need more than $3,000 per month in dividends? No problem. Here are five steps you can follow to make sure you are banking at least $5,000 or more in monthly dividend income on a six-figure portfolio.

Step No. 1: Buy Closed-End Funds (CEFs)

There are a few stocks that pay monthly dividends, such as Realty Income Corp (O). But, generally speaking, they don’t pay enough to make your monthly checks matter.

For example, Realty Income yields 3.6% today. You could pile $500,000 into shares, but you’re only making $1,500 per month.

Exchange-traded funds (ETFs) are also going to leave you short on yield. These popular vehicles are too well-known for their own good. They are priced “efficiently,” which means it’s tough to get a bargain.

But you and I are not running billions of dollars, so we do not require the “liquidity” of the big ETFs. We can buy smaller funds that manage “just” a billion dollars. For example, Aberdeen’s Asia-Pacific Income Fund (FAX) is a CEF that yields a fat 7.7% and pays its dividends monthly.

CEFs are underappreciated vehicles. Their smaller stature and fund size (FAX has a modest $1.07 billion in assets) means we can find bargains there. As I write, FAX trades at a generous 11% discount to the value of its assets. In other words, we can buy this 7.7% payer for just 89 cents on the dollar.

Step No. 2: Look for CEFs That Are Discounted

When buying CEFs, our ability to demand these discounts is a great advantage. We are paying less than face value for perfectly good assets.

Matisse Capital’s Eric Boughton shared his firm’s research on CEF discounts at the Inside Fixed Income conference I recently attended. (Boughton conducted the study in partnership with University of Oregon’s Lundquist College of Business).

He explained that if you’d taken the 600-plus CEFs in existence since 2008, and simply only bought the funds trading at discounts to their net asset values (NAVs), you’d have earned 11% per year. (This assumes you “rebalance” monthly to sell any funds that swing to premiums and then buy newly discounted funds instead.)

Eleven percent per year is pretty good, especially given the lack of thought required to execute on this strategy. Of course, taxes will be a problem with the monthly buying and selling, but we can get around that by simply cherry-picking the very best CEFs so that we don’t have to be constantly flipping shares.

Step No. 3: Follow the Money

Rewinding back to FAX, we can see that it has no problem funding its distribution, for two reasons.

First, the discount helps. FAX is not actually “on the hook” for 7.7% per month. That’s what we bargain hunters receive, when we purchase FAX at a discount.

The managers running FAX only care about their own NAV, or the portfolio of bonds that the fund holds. They need 7% yields (it becomes 7.7% for us after the double-digit discount), and they can fund them two ways:

- Via NAV gains, and/or

- Big bond yields.

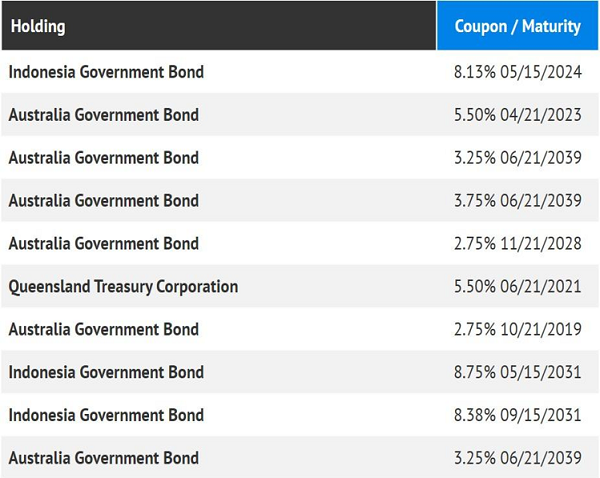

It’d be plenty challenging for the folks at Aberdeen to find 7% bond yields if they had to focus on the US and Europe only! Fortunately, FAX’s “mandate” lets it dabble in Asia, and management takes advantage of this by buying secure bonds like these that yield up to 8.75%:

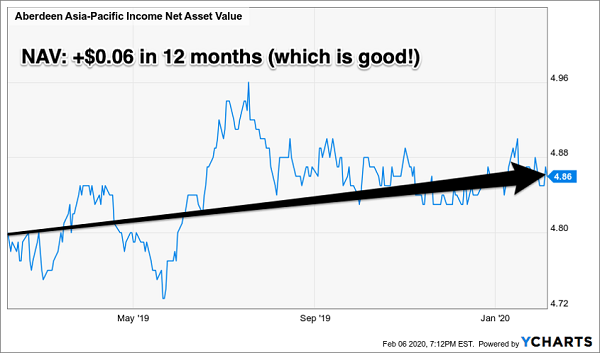

Step No. 4: Follow the NAV

How do we really know if a fund is investing profitably? Simple: Look at the NAV. In FAX’s case, its NAV is steady, and that’s exactly what we want to see. It means that the fund is able to pay its distributions from income and profits without having to tap its NAV like a piggy bank:

FAX Boosts NAV While Paying Fat Dividend

Step No. 5: Don’t Be Cheap About Fees

Most investors are conditioned by their experience with mutual funds and ETFs to search out the lowest fees, almost to a fault. This makes sense for investment vehicles that are roughly going to perform in-line with the broader market. Lowering your costs minimizes drag.

Closed ends are a different investment animal, though. On the whole, there are many more dogs than gems. It’s an absolute necessity to find a great manager with a solid track record. Great managers tend to be expensive, of course — but they’re well worth it.

The stated yields you see quoted, by the way, are always net of fees. It’s the cash you receive.

To learn more about generating monthly dividends as high as 8%, click here.