Let’s cut the Fed-babble and call things how they really are. Because what happened last week means a lot for our dividends — and whether we’ll be able to count on them in the future.

(In a moment, we’ll hit up three stocks that are perfect buys in today’s “Fed-driven” economy — they pay dividends up to four times bigger than those of the S&P 500.)

Last week we learned that:

- The economy is roaring, with GDP up 6.4% in March from a year ago — that’s the kind of number you expect from a developing country like Vietnam, not the world’s biggest economy, yet …

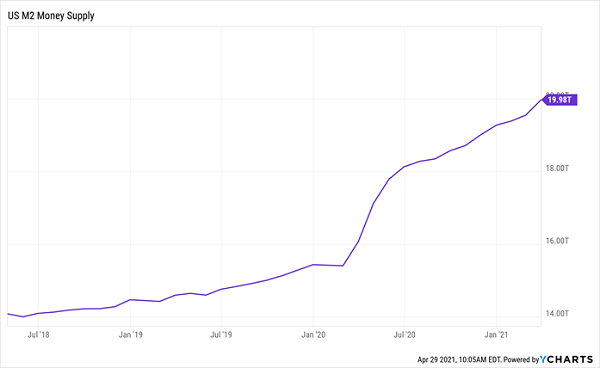

- The Fed’s money printer will STILL go “Brrrrrrr…” Fed Chair Jerome Powell made no bones about it after last Wednesday’s Fed meeting: His massive bond purchases and zero-point-nothing interest rates are here to stay. That’s even though 22% of all greenbacks out there were conjured up in just the past 13 months!

Powell’s Mountain of Fiat Cash Grows

It doesn’t take a Cornell economics degree to see what this means: INFLATION.

It’s already here. The consumer price index (CPI) jumped 2.6% in March from a year ago, pole-vaulting over the Fed’s 2% goal.

Even Powell admits it, but he also says this inflationary tango will be “transitory,” lasting only a few months, as this year’s CPI stacks up to last year’s crushed economy. But you and I both know inflation is rising faster than Powell admits. Have you bought gas for your car lately? How about building materials? Or groceries?

Look, some people might think Powell can tame the inflation dragon he’s unleashed, but there’s no way I’d bet my retirement on it — and you shouldn’t, either.

Inflation Surges, You Win. Inflation Slows, You Win

So today we’re going to look at one contrarian investment that’s a classic “win either way play”: real estate investment trusts (REITs).

These “landlords” own properties ranging from cell towers to self-storage facilities. They’re a savvy play during an inflationary period because:

- They simply rent out space — so they’re not facing price pressures, such as for labor and raw materials — to nearly the same degree as companies that produce goods.

- Their dividends outrun inflation, partly because Uncle Sam gives them a hall pass on corporate taxes so long as they pay 90% of their profits as dividends. The typical REIT yields 3.3% today, more than double the S&P 500 average. Plenty pay way more, and the lower yielders tend to grow their payouts fast.

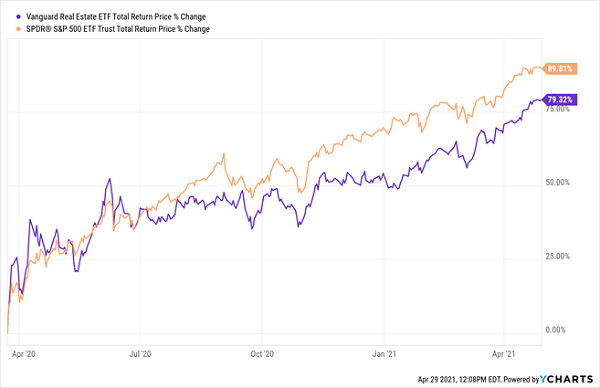

- They’re still undervalued: REITs have outpaced the market for long stretches over the past several years, but they’re well behind the S&P 500 since the March 2020 crash, suggesting they have room to run.

Our REIT Buy Window: Still Open

This chart tracks REITs’ performance through the benchmark Vanguard Real Estate ETF (NYSE: VNQ), and as you can see, the gap between it and the SPDR S&P 500 ETF (NYSE: SPY) is narrowing.

I expect REITs to break past their common-stock cousins shortly, making now a good time to buy. Here are three that should be on your radar:

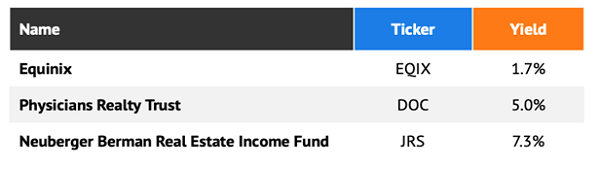

Inflation-Proof REIT Play No. 1: Equinix

Equinix (Nasdaq: EQIX) is a pioneer in the data-center space, having been established back in 1998. Today it boasts 210 data centers across 55 cities and five continents.

The REIT has been a standout during the pandemic, with its services vital to supporting scores of employees toiling away from home. That trend isn’t going away, and neither are the others the trust is dialed into, such as surging e-commerce and the continued growth of the Internet of Things.

Funny thing is, most people have come to see the stock mainly as a lockdown play and have discounted its importance to the post-COVID-19 world. As a result, it’s pulled back lately, giving us an opportunity to pick up this growth REIT at mid-2020 prices:

EQIX Goes on Sale

That’s absurd for a firm that saw revenue jump 10% in the first quarter, while adjusted funds from operations (FFO, the best metric for REIT profitability) soared 21%. For all of 2021, management is calling for $24.76 of FFO, up 12% from a year ago on a normalized and constant-currency basis. Those are huge numbers for a steady landlord like Equinix.

Even so, as dividend investors, we might be tempted to bypass Equinix due to its low current yield of 1.7%. That would be a mistake, because that figure masks the fact that management has hiked the payout 64% in the last five years. As a result, folks who bought then are yielding 3.5% on their shares — double today’s yield.

We can expect plenty more upside: The payout accounts for just 47% of FFO, which is shockingly low in the REIT space, where payout ratios in the 80% to 90% range are usually quite sustainable, due to REITs’ steady rental income.

The shares trade at 28-times forecast FFO today, which is par for the course for Equinix, and considerably less than you’d have paid a couple months ago, thanks to the pullback in the stock.

Inflation-Proof REIT Play No. 2: Physicians Realty Trust

Physicians Realty Trust (NYSE: DOC) owns 275 medical offices that are almost all leased (96% as of this writing) to major health systems across the US.

Like Equinix, it’s in the “sweet spot” of REITs: DOC’s health-care tenants saw high demand through the pandemic and will continue to do so post-COVID-19, with people laser-focused on their health.

Management remains focused on facilities providing outpatient care. This was a smart move pre-pandemic and it’s an even smarter move now: Demand for these services is soaring as hospitals look to free up capacity.

Outpatient care’s steady growth will keep demand for DOC’s offices high, and we get some additional support from its long lease terms, with only 28% of its tenants up for renegotiation through 2025.

DOC yields 5% and its payout accounts for 88% of 2020 FFO. That’s quite manageable for a REIT with the steady rental income DOC boasts. The REIT is also fairly priced at 18-times 2020 FFO.

Inflation-Proof REIT Play No. 3: Neuberger Berman Real Estate Income Fund

I generally prefer to buy my REITs individually, but I know many folks prefer to do so through a fund. If that’s you, do yourself a favor and avoid REIT ETFs. Go with a closed-end fund (CEF) like the Nuveen Real Estate Income Fund (NYSE: JRS) instead.

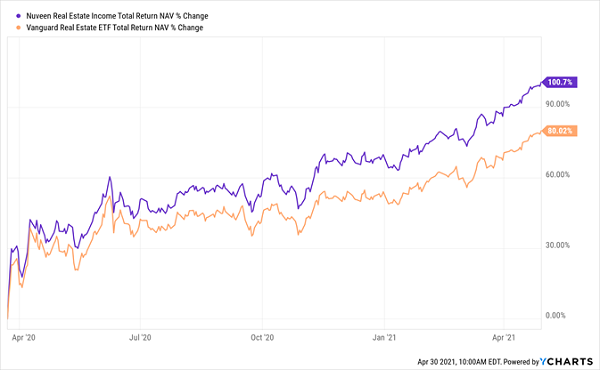

For one, real estate CEFs are actively managed, and Nuveen is a long-established player in the CEF space, with plenty of experience. And management has shown its REIT-picking chops, with the fund’s net asset value (NAV, or the value of its underlying portfolio) cruising well ahead of VNQ on a total-return basis coming out of the selloff:

JRS Rolls Past the Benchmark

There are two other reasons to go with JRS over an ETF: dividends and discounts.

First, the dividend: JRS yields 7.3% today, more than double what VNQ pays, and you can also grab JRS at a discount: The fund trades at a 6% discount to its NAV, so we’re getting its portfolio, whose top holdings include Equinix and other well-known REITs like warehouse owner Prologis (NYSE: PLD) and Public Storage (NYSE: PSA) for 94 cents on the dollar. (It also devotes 28% of its portfolio to preferred shares, which pay strong dividends and offer more stability than regular stocks.)

Discounts like these are a quirk of CEFs — they don’t exist anywhere else — mainly because a CEF’s share count is largely fixed, allowing investors to bid the fund up and down in ways totally unrelated to NAV.

Finally, the discount makes JRS’s dividend safer: Its 19-cent quarterly payout only works out to 6.8% of NAV (or what management must earn to cover it). That’s considerably less than JRS’s 7.3% yield on market price — or the dividend we get!

To learn more about generating monthly dividends as high as 8%, click here.