I can’t stand financial planners.

I know I’m the dividend and income guy around these parts. But I have a different approach when it comes to nest eggs and preparing for the future.

You’ll see what I mean as we revamp my Investing With Charles video series.

To start, I want to settle a debate that’s made its rounds in the financial world: blue-chip stocks versus index funds.

Thank you, Joan, for the fantastic question that sparked this discussion! (Email Feedback@MoneyandMarkets.com if you have a question of your own.)

Let’s settle the score.

Check out the highlights of my discussion with Research Analyst Matt Clark below.

Index Funds vs. Blue-Chip Stocks

Matt: We’re going to talk about blue-chip stocks, retirement accounts and index funds. It’s right in Charles’ wheelhouse.

Joan emailed us and said:

I’m decades away from retirement. Should I be buying blue chip stocks in my retirement account now while they’re cheap? Or is it best to stick with safe index funds?

Charles, take it away.

Charles: That‘s a really good question.

I’ll start with index funds.

If index funds are what you have access to, then that’s fine. At the end of the day, index funds give you a nice sampling of the best of America … its best and biggest companies.

If you have either limited capital to invest or you’re talking about a menu of mutual funds in your 401(k) or whatever, then buying an index fund and being done is fine.

Now, index fund prices are on the high side today, even after this correction/bear market.

This isn’t a fat pitch moment for index funds.

But at the end of the day, if your time horizon here is years in the future, then there’s nothing wrong with buying index funds.

However (there’s always a however), I do lean toward picking out a portfolio of individual blue-chip names. There’s a couple of reasons for that.

The Problem With Index Funds

Charles: Look, index funds are good, but they have one structural problem: Most index funds are cap-weighted.

What that means in plain English is that fund managers weight the holdings of stocks by their size. So the biggest, most valuable companies are the biggest components of the fund.

These funds aren’t weighted by profitability or the stocks’ prospective value in the future.

They’re weighted by stock values today.

There is some logic to that. If you want a slice of the stock market, index funds offer that.

The problem is there’s always churn at the top. When you buy an index fund that’s heavily weighted toward those top names, you’re buying a collection of stocks that’s already done well in the past.

The biggest stocks in the S&P 500 are all worth over a trillion dollars now. You’re buying stocks that are already at the top.

Sure, they can continue to grow, but the best years of growth are behind them. You’re buying these companies when they’re already mature.

There are up-and-coming names as well. You’re not getting big access to them. You’re getting a very tiny, fractional piece of that company.

The biggest drawback to just buying an index fund is that you’re getting into the index after its big run.

Beyond that, an index fund is exactly what it’s designed to be. You’re getting the market.

You’re getting the good, the garbage and a little bit of everything in between.

Why settle for that?

Why settle for the good and the bad when you can cherry-pick a list of solid blue-chip stocks that you think should outperform the market?

Blue-Chip Stocks Can Beat the Index

Matt: Let’s talk about some of those stocks that are heavily weighted in an index fund.

Charles: Yeah, sure.

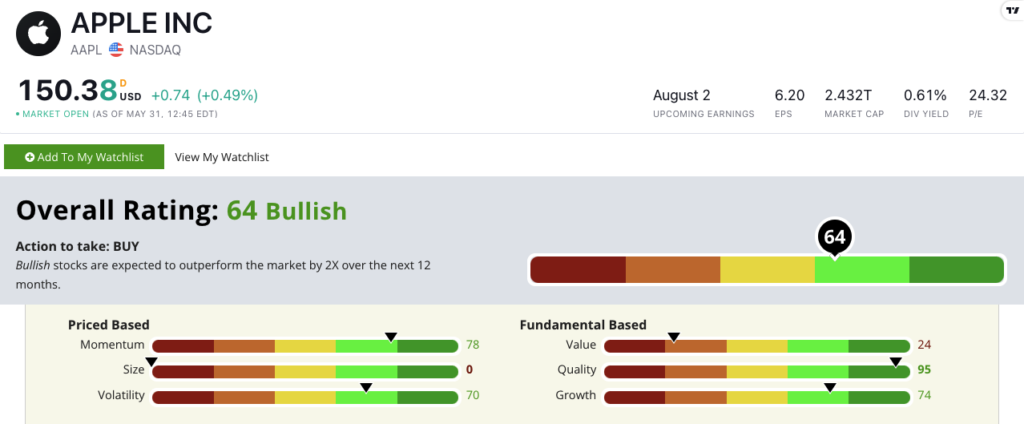

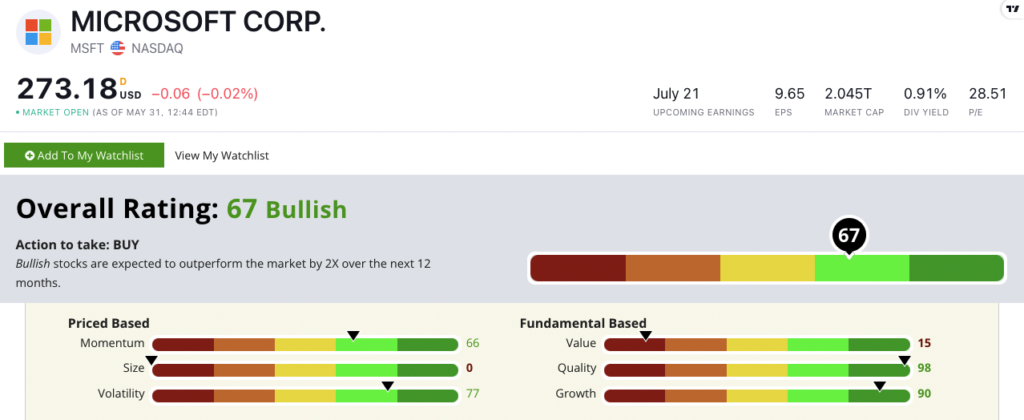

Looking at top holdings of index funds tracking the S&P 500, the companies that tend to make up the weight of the funds, the top two right now are Apple Inc. (Nasdaq: AAPL) and Microsoft Corp. (Nasdaq: MSFT).

These are great companies.

Who wouldn’t want to own Apple or Microsoft?

They’re fantastic blue-chip stocks and both rate “Bullish” on our Stock Power Ratings system.

Apple and Microsoft’s Stock Power Ratings on May 31, 2022.

Both rate over a 60. That’s solid.

But when you go down the list in these index funds, it’s not as attractive of a story.

Several huge companies are all “Neutral,” or even “Bearish” in a few cases.

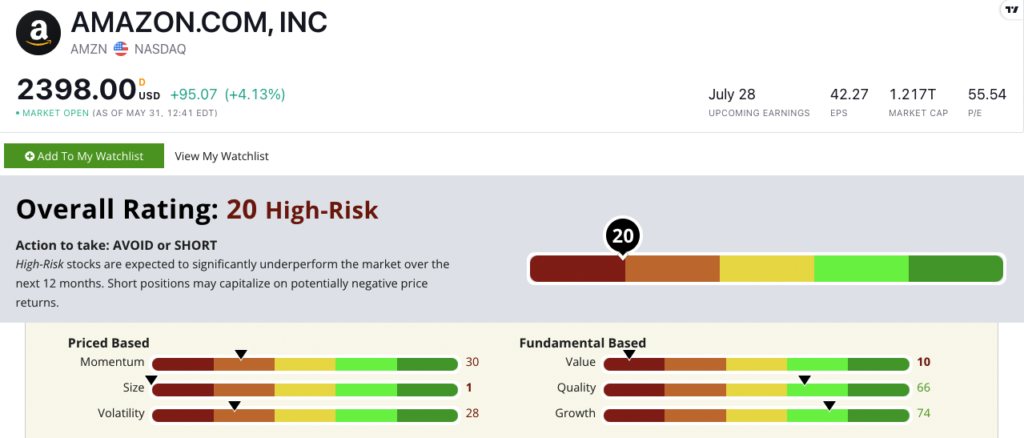

Amazon.com Inc. (Nasdaq: AMZN) is one of the best success stories in the last 50 years of American history.

Our model suggests this isn’t really the best time to back up the truck on AMZN.

Amazon’s Stock Power Rating on May 31, 2022.

If you’re buying an index fund, you’re buying a lot of Amazon stock. Our model suggests you should probably wait on that.

You can’t do this with most 401(k)s, but you can cherry-pick certain stocks in accounts like your IRA or Roth IRA.

If you’re the adventurous sort, you could even start with the entire list of the S&P 500 and remove stocks that didn’t make the grade for the time being in our Stock Power Ratings system. Then you can just focus on the ones that do rate well.

That’s a lot of homework, but my bottom line is that cherry-picking the best of the best makes sense.

Click here to watch the rest of Investing With Charles. Matt and I highlight a stock that I cherry-picked earlier this week for my dividend story.

Where to Find Us

Coming up this week, Matt will have more on The Bull & The Bear podcast, so stay tuned.

Don’t forget to check out our Ask Adam Anything video series, where Chief Investment Strategist Adam O’Dell answers your questions.

You can also catch Matt every week on his Marijuana Market Update. If you are into cannabis investing, you don’t want to miss his weekly insights.

Remember, you can email my team and me at Feedback@MoneyandMarkets.com — or leave a comment on YouTube. We love to hear from you! We may even feature your question or comment in a future edition of Investing With Charles.

To safe profits,

Charles Sizemore, co-editor, Green Zone Fortunes

Charles Sizemore is the co-editor of Green Zone Fortunes and specializes in income and retirement topics. He is also a frequent guest on CNBC, Bloomberg and Fox Business.