For all the talk about 2020 being a transformative year, very little new actually happened. The COVID-19 pandemic just sped up trends that had been in place for years.

Working from home? I’ve done that off and on for almost 20 years. Streaming video? Well over a decade. Electronic signatures? Please! You give me a piece of actual paper to sign, and I’m going to consider you as frozen in time as an Amish farmer in a horse buggy. I’ve been using DocuSign for years.

The death of retail was harped on to no end in 2020. But again, there wasn’t much new there. I was already doing 75% of my buying online long before the pandemic. COVID-19 just moved that needle closer to 95%.

If you’re an income investor, you can’t let your portfolio get frozen in time. Many high-yielding dividend stocks are in “old economy” companies, whereas the fastest-growing tech stocks tend to be stingy with their dividends (if they pay them at all).

This brings me to our dividend stock of the week, International Paper Co. (NYSE: IP). On the surface, International Paper would look like one of those ossified old-economy stocks destined for a slow decline into irrelevance. It’s paper, for crying out loud.

But the reality is much different. If you believe in the long-term growth of online shopping, then International Paper should be in your dividend portfolio.

What International Paper Company Is

IP isn’t a “paper” company. It’s primarily a packaging company. According to company estimates, packaging products should account for about $17 billion in sales for the full year 2020, whereas paper products made up about $4 billion. And the company is in the process of selling off its legacy paper business, which will make it a pure-play on packaging.

If you believe that the ever-growing stacks of Amazon boxes will only continue to grow on the doorsteps of America, then it makes sense to own a high-yielding packaging company like IP. You’re getting a consistent 4.1% dividend while riding one of the most powerful trends of our lifetime.

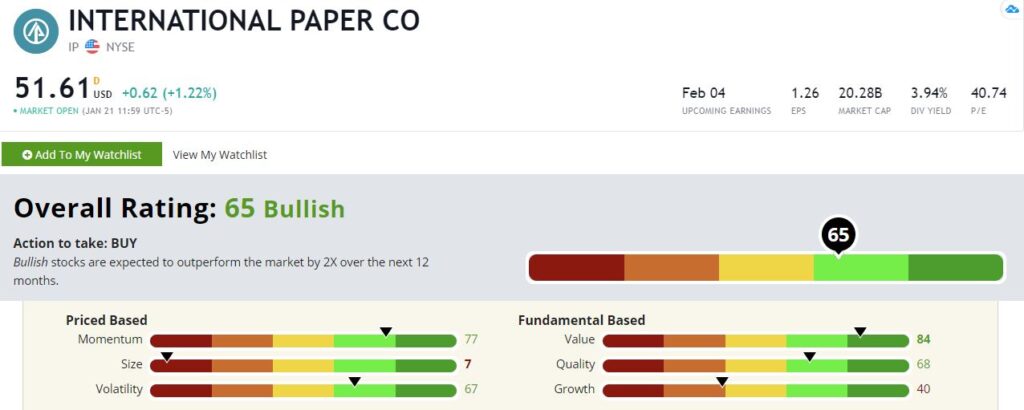

Let’s see how IP stock stacks up using Adam O’Dell’s six-factor Green Zone Ratings model.

IP Stock Rating

Its overall score of 65 puts IP stock in “bullish” territory of our system. Bullish stocks (rated 61-80) are expected to enjoy returns of around double the S&P 500’s return over the following 12 months, based on our research.

International Paper Co.’s Green Zone Stock Rating on January 21, 2021.

Let’s dig a little deeper to see what is driving that score.

Value — IP stock rates highest on value, scoring an 84. This means that the stock is cheaper than all but 16% of the stocks in our universe, and that isn’t a surprise. The raging bull market of recent years has almost exclusively focused on tech and growth names. Old economy stocks like International Paper aren’t in high demand. But with a juicy 4% dividend, I don’t expect IP to stay unloved for long.

Momentum — And in fact, it seems that investors are already flocking to the stock. IP scores a very respectable 77 based on momentum. The stock has been trending higher since March and shows little sign of slowing down.

Quality — We focus primarily on debt management and profitability in our quality metric. IP stock scores well here at 68. And following the spinoff of its paper division, I believe the quality score will move higher as the company shed’s slower-growing product lines.

Volatility — Low-volatility stocks tend to outperform high-volatility stocks over time. So, a higher score on this metric means that the stock is less volatile. International Paper scores a 67 here, meaning it is less volatile than all but 35% of the stocks in our universe.

Growth — If IP has a weakness, it would be growth. The stock rates at a 40 here, putting it in the bottom half of stocks we rate. But IP’s growth prospects should improve once it sells its paper division.

Size —IP loses points on size, scoring just a 7. All else equal, smaller stocks tend to outperform larger ones. And given that International Paper is a $20 billion company, we won’t see a small-cap bounce here.

Bottom line: In International Paper, you have a solid dividend payer in the process of streamlining its business to focus on the most profitable lines. It also happens to be on the right side of one of the greatest trends of our lifetime in the move to e-commerce.

And that reminds me … I need to go and pick up a few Amazon boxes off my porch.

To safe profits,

Charles Sizemore is the editor of Green Zone Fortunes and specializes in income and retirement topics. Charles is a regular on The Bull & The Bear podcast. He is also a frequent guest on CNBC, Bloomberg and Fox Business.