By now, you know I’m a huge fan of real estate investment trusts (REITs). If you’re building an income portfolio, REITs are all but mandatory. There are precious few corners of the market where you can find high current yields and steady, inflation-beating dividend growth. REITs are one of those corners.

REITs are able to pay market-crushing high yields in large part because they’re exempt from federal income taxes, so long as they distribute at least 90% of their net income. Every dollar not paid in income taxes is available to pay out as a dividend.

The IRS has taken a rather broad view of what qualifies as “real estate” these days to benefit from REIT taxation. You can buy REITs that invest in billboards, cell towers … or prisons!

Even document storage and secure shredding facilities can be rolled into a REIT structure. That’s the case with Iron Mountain Inc. (NYSE: IRM).

If you work in an office setting, you’re likely familiar with Iron Mountain. It manages most of the ubiquitous secured shredder boxes, and you’ve likely seen stacks of file boxes with the Iron Mountain logo.

Iron Mountain’s core business is secure document storage. It stores millions of boxes for hundreds of thousands of companies and other organizations spread across the world.

This is a stable business that pretty much runs itself once the initial legwork is done. After paying to move literal tons of paper, no company ever wants to look at that paper again. They’ll pay Iron Mountain until the end of time to keep it out of sight and out of mind … yet still available in the event it’s needed for an audit.

And Iron Mountain is looking beyond the age of paper. The company is building out its cloud storage business to provide the same level of secured storage for digital documents.

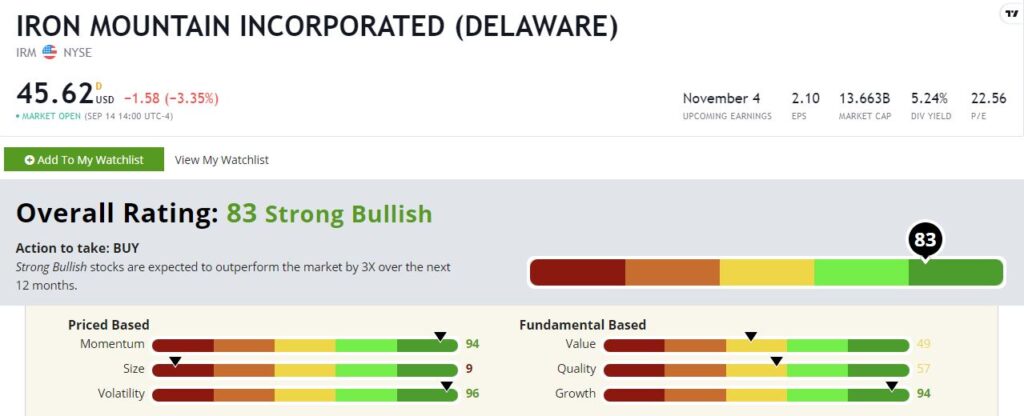

Iron Mountain’s Dividend and Stock Rating

At current prices Iron Mountain yields a competitive 5.2%, and the company raises its dividend most years. Over the past five years, the dividend has been raised by a cumulative 28%, outpacing inflation by wide margin.

Iron Mountain Inc.’s Green Zone Rating on September 14, 2021.

Iron Mountain rates a “Strong Bullish” 83 out of 100 on our Green Zone Ratings system. Let’s dig a little deeper into those details.

Volatility — Iron Mountain’s business is stable, and that is reflected in the stock’s high rating on our volatility factor at 96. The higher the rating here, the lower the volatility. So, this means that Iron Mountain is less volatile than all but 4% of the stocks in our universe. That’s an attractive characteristic in a dividend stock. We like stable and boring.

Momentum — Despite the low overall volatility, Iron Mountain rates well on our momentum factor as well, with a score of 94. The shares have more than doubled off of their pandemic lows. Investors seem to be attracted to the high dividend, the stability of the core business, and the growth potential of its cloud storage unit.

Growth — Likewise, IRM rates a 94 on our growth factor. In a world in which tech stocks dominate the growth discussion, it’s impressive to see Iron Mountain rate well here. We measure growth over varying time horizons, and Iron Mountain is competitive across the board. Particularly of note is that the company rates a 94 on its compound annual growth rate of earnings. Not only is Iron Mountain growing, but it’s managed to maintain that growth for a good stretch.

Quality — REITs don’t rate all that well on our quality score because earnings are depressed by accounting quirks. REITs also carry a lot of debt in most cases. It is what it is, and we know that going into the analysis. Iron Mountain is no exception, rating a respectable but not remarkable 57 on our quality factor.

Value — The same is true of our value factor. REITs seldom look cheap by traditional value metrics due to funky accounting. Nevertheless, IRM rates are about average here at 49. That’s OK.

Size — Iron Mountain has grown into a large REIT with a market cap of $13 billion. It rates a 9 on our size factor.

Bottom line: Iron Mountain’s torrid momentum won’t last forever. I expect the shares to cool off in the coming months. But the high 5.2% yield should put a nice floor under the stock price in a world in which most bonds yield less than 2%. It’s also promising to see Iron Mountain fleshing out its cloud storage business as companies focus on digital record storage.

P.S. Live on September 23, Adam O’Dell will reveal the details of a simple two-day trade we believe is the fastest way to grow money ever devised. It’s a big claim. Can we prove it? Find out on September 23 by signing up for the event here.

To safe profits,

Charles Sizemore

Co-Editor, Green Zone Fortunes

Charles Sizemore is the co-editor of Green Zone Fortunes and specializes in income and retirement topics. He is also a frequent guest on CNBC, Bloomberg and Fox Business.