Matteo Salvini is a very smart politician. And after months of speculation and relentlessly rising popularity, Salvini finally pulled the plug on his party’s support for the current Italian government.

Over the past 18 months his rise to power in Italy has seen him play for fools some of the biggest players in the field and come out the other side with a nearly unheard of popular mandate for a nominally right-wing politician.

First, it was Silvio Berlusconi whom Salvini partnered with in last year’s campaign, hitching his newly rebranded Lega party with Berlusconi’s Forza Italia and the Brothers of Italy. This was a formidable center-right coalition to challenge the status quo, nominally.

But a strange thing happened by election day: The junior partner, Lega, was the higher vote-getter, and Forza Italia the fading stalking horse for Brussels.

After a suitable break-up period, Salvini ditched Berlusconi at the altar for Luigi Di Maio of Five Star Movement (M5S) and cobbled together a coalition of Euroskeptics no one in Brussels or Rome were happy with.

This was always a marriage of convenience. Moreover, the entrenched power brokers in Rome were not about to allow these upstarts to derail the European project.

So they saddled the new guys with a Troika of Technocrats to keep a lid on things. The Troika I’m talking about is President Sergei Mattarella, Prime Minister Giuseppe Conte and Finance Minister Giovanni Tria.

Now that Salvini has withdrawn Lega’s support for the current government, the real political fight can begin. The current arrangement was always a stopgap measure, a way to prime the electoral pump and set the terms of engagement. It was the warm-up band, not the headline attraction.

That starts now.

In the past year, M5S’s support has collapsed from above 30% to just 17%. Lega’s has skyrocketed from 15% to 38%-40%, depending on the poll.

Prime Minister Conte is dutifully doing his job protecting the current arrangement, which is the best of a bad set of cases for the EU. According to Bloomberg, Conte is going to fight Salvini’s withdrawal of support. This is the same Conte who threatened to resign after the European elections over Salvini’s proposed economic agenda.

“He wants to go to elections to make the most of his party’s current support,” Conte said in an online video message. Nevertheless, “it’s not up to the interior minister to summon Parliament, it’s not up to the interior minister to decide the timing of a political crisis when much more important actors are involved.”

Those “more important actors” involved are the European Union and the Italian Deep State, wedded to a United States of Europe, support for which stretches back more than a century.

Conte was willing to bring down the government when Lega was polling 30-32% and there was no path to them gaining a full majority in parliament. Now, he won’t budge because Salvini is likely to win that elusive majority.

Conte will try and hold up the vote in Parliament on dissolving government. Salvini may have to go around him. And if both leaders of the Democrats and M5S are telling the truth then there is a majority to bring a motion of no-confidence in Conte to the table, according to the same Bloomberg article.

After Conte stands President Mattarella, who will try to engage parties to put a different government together before allowing another vote. That won’t happen. But, Mattarella will drag his feet unless the current parliament impeaches him.

What Salvini has done is to fully expose who is blocking the reforms Italians obviously want. A government without the support of the people cannot stand for long. Both Mattarella and Conte will fold regardless of the pressure on them not to.

The fallout here is as follows. As long as it looks like Salvini will not get his new election the markets will err on the side of stability. The euro will continue to levitate just above the breakdown line at $1.11 despite a rising dollar and yen (more on that in a minute), and deteriorating financial and economic conditions.

But once the reality sets in, only then will the pressure mount to the point of no return. The same is true of Boris Johnson’s fronting to the world he’s prepared for a no-deal Brexit. Markets want to believe that there’s a compromise because “cooler heads” usually prevail.

But what happens when they don’t?

The Italian debt markets are a complete fantasy. They have been for years but this year they went from urban legend to full-blown fairy tale.

A recent report from ZeroHedge laid out who has been the mysterious buyer of Italian junk sovereign debt in 2019 since the ECB withdrew support, Japan.

Something that has not broken down in recent months has been Italian bonds, whose yields have bizarrely been tumbling despite the lack of ECB support, although overnight it emerged just who was the buyer of first and last resort was when Bloomberg reported that Japanese investors bought the largest amount of Italian sovereign bonds since at least 2005 in June; purchases of Italian government securities climbed to 278.8b yen ($2.6b), the highest since comparable data became available in 2005, according to Japanese balance-of-payments released Thursday.

Japanese investors bought ridiculous amounts of the riskiest paper. Japan. Mrs. Watanabe. Really?

This is likely Japanese banks acting as proxies for the Bank of Japan, who were acting as proxies for the ECB and the IMF, who bought these bonds to stuff them into a hole for a few months where no one was looking.

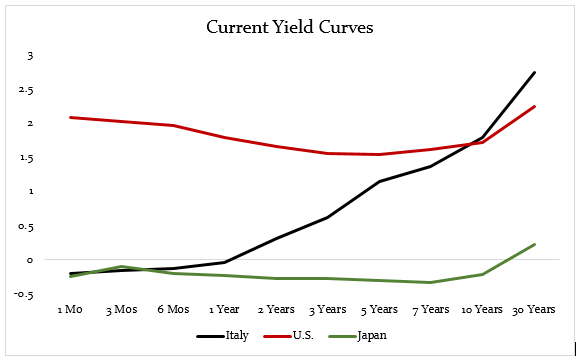

And this is where the real danger is right now. The global safe haven trade in play has, as ZeroHedge noted, included Italian debt that has no business trading at negative yield spreads to similar-maturity U.S. debt. See the chart below. This is after a near-50-basis-point correction in the past 24 hours.

Did Mrs. Watanabe finally realize that paying even more for the privilege of holding savings in euros was not a good deal? And this against a backdrop of a weakening EUR/JPY cross.

These were losing money positions intended to support a political pressure campaign against Salvini to oust him from power.

So as long as the euro can’t rally, pushing sovereign bond yields lower only highlights both the fear building in the financial system, which has little to do with the Fed, and the insanity of the ECB’s policy.

At some point you simply reach a limit of stuffing money into corners of the walls of the financial world.

And while Donald Trump would look at this and yell at the Fed for not lowering rates enough, the truth is that this is the picture of intervention failing to keep the fragile Italian banking system from collapsing and spilling over into Germany.

Only because Germany’s entire yield curve is trading at negative yields is this situation capable of continuing. But this is what Europe has to do to continue projecting the image that all is well, even though it isn’t.

Salvini just called the ECB’s bluff on who really is in financial trouble. Because never forget the axiom: When you owe the bank a thousand dollars it’s your problem — but when you owe the bank 132.5% of GDP, it’s their problem.

Make no mistake, Italy is the ECB’s problem.

It is precisely because Salvini has provoked this political crisis that Italian bond yields are bolting higher, forcing even more scrambling to maintain control behind the scenes.

If you wanted your catalyst for what triggers the unraveling of Europe, Salvini may have just pulled it by demanding a divorce from his shotgun wedding with M5S and the Italian Troika.

• Money & Markets contributor Tom Luongo is the publisher of the Gold Goats ‘n Guns Newsletter. His work also is published at Strategic Culture Foundation, LewRockwell.com, Zerohedge and Russia Insider. A Libertarian adherent to Austrian economics, he applies those lessons to geopolitics, gold and central bank policy.