Peloton Interactive Inc. (Nasdaq: PTON) is a “story stock” for the pandemic.

As a maker of premier home exercise equipment, it is well positioned to profit as Americans are stuck in their homes and desperate for a little exercise.

Peloton’s exercise bikes and treadmills come with large touch screens that make exercise more interactive. Rather than watch a TV from across the room or listen to music, users can choose a live or on-demand personal trainer video to push them along.

Peloton is known for its high-end stationary bikes. But the company likes to position itself as an innovative technology and media company — the “Netflix of fitness,” if you will.

In addition to paying a couple thousand dollars for Peloton equipment, customers also pay subscription fees of $39 per month for the streaming workout programs.

It’s an interesting concept. But thus far, it’s been an unprofitable one. Peloton is expected to report a modest profit during quarterly earnings in September. But up until this point, it hasn’t been in the black.

Let’s see how Peloton’s stock rating stacks up using Adam O’Dell’s Green Zone Ratings system.

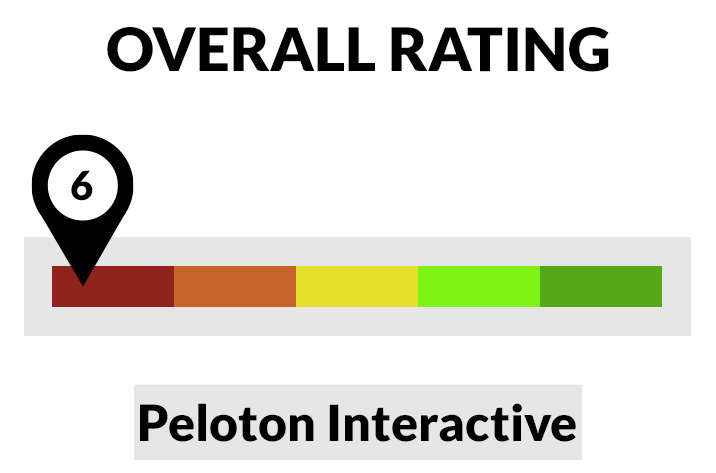

Peloton Stock Rating

Yikes … It’s not pretty. Peloton rates as a 6, meaning that fully 94% of the stocks in our universe rate higher.

- Volatility — Stocks with lower volatility tend to perform better over time. Peloton rates a 41 on volatility, which is pretty middle of the pack. While the stock doesn’t experience huge price swings, it isn’t getting any medals for stability, either.

- Momentum — Peloton had a fantastic run following the COVID-19 outbreak, soaring over 200% in the months following the March lockdowns. But shares were stagnant prior to the outbreak, and they have traded sideways for most of the past two months. Peloton scores a 34 on momentum, meaning around two-thirds of the companies in our universe rate higher. To be fair, our rating here is skewed due to Peloton not having a full year’s worth of trading history. It only went public in September of last year.

- Quality — Peloton rates a 28 on quality. Its low margins, cash flows and returns on equity, assets and investment really drag it down here. Peloton is young and not yet profitable. At this stage, this is a low-quality company that got bailed out by a global pandemic.

- Growth — Peloton rates low on growth, at 20. It’s possible that the company’s explosive sales growth of the past two COVID-driven quarters isn’t fully reflected in the ratings numbers yet.

- Value — This is not a cheap stock. Peloton rates an 18 on value. Its price-to-sales ratio is worrisome, coming in at 7.

- Size — Smaller stocks tend to outperform larger stocks over time. Alas, Peloton gets no boost based on size. It rates a 9, which means it is larger than 91% of other stocks we rate.

Takeaway: Peloton’s products were exactly what Americans needed when they were stuck in their homes for months on end. But is this a durable trend or a short-term windfall? Could Peloton’s stock rating be adjusted up?

That remains to be seen. Based on our Green Zone Ratings system, though, Peloton doesn’t look like a long-term winner.

Money & Markets contributor Charles Sizemore specializes in income and retirement topics. Charles is a regular on The Bull & The Bear podcast. He is also a frequent guest on CNBC, Bloomberg and Fox Business.

Follow Charles on Twitter @CharlesSizemore.