Managing Editor’s Note: Charles wrote about Realty Income back in March 2021. Since then, its stock has improved to a “Bullish” 61 rating in our Stock Power Ratings system, so Charles updated his original story to show you why O is a perfect stock for this market. — Chad Stone, managing editor, Money & Markets

Let’s take a look at one of my all-time favorite dividend stocks — the “Monthly Dividend Company” itself, Realty Income Corp. (NYSE: O).

Realty Income is quirky because it pays monthly dividends instead of quarterly. But that’s great if you use the dividends to pay your regular monthly expenses.

Its stock also looks terrific for this bear market.

I look for three things in a dividend stock:

- I like a competitive This doesn’t mean the highest yield on offer because that’s a recipe for a dividend cut. But in a world where the 10-year Treasury bond yields around 3%, a 4% dividend yield is pretty darn good.

- I also look for dividend growth well above the rate of inflation. If our goal is to hold the stock for years or even decades, a rising dividend is the only guarantee that you don’t lose purchasing power to the ravages of inflation.

- Finally, I like stability. I want businesses that are future-proof. Stable income requires stable businesses to produce dividends.

Realty Income checks all of these boxes.

Why O Is Perfect for the Bear Market

Realty Income sports an attractive 4.6% dividend yield. And it’s raised its dividend 115 times since entering the public market in 1994. If that’s not stable consistency, I don’t know what is.

Realty Income is a triple-net real estate investment trust (REIT). That’s a technical way of saying that it doesn’t actually do anything. The tenants pay all taxes, insurance and maintenance expenses. The landlord’s responsibility is limited to opening the mailbox once per month to collect the rent check.

Looking back, 2020 was awful for brick-and-mortar retail properties due to forced closures and other COVID-19 restrictions. But not all retail is the same.

Realty Income’s portfolio is weighted to “inflation-proof” properties, like grocery and convenience stores, which together make up a little over 20% of the portfolio. Its largest tenants by percent of total portfolio annualized rental revenue at the end of 2020 are:

- Walgreens, 4%.

- 7-Eleven, 3.9%.

- Dollar General, 3.9%.

- FedEx, 2.9%.

Here’s what is important to remember. To start, Realty Income’s tenants are established national chains with access to financing. These are not mom-and-pop operations.

Prior to the pandemic, this stock hit a high just shy of $85 per share. Today, it trades for around $65.

I just wrote about Kellogg’s status as a stock to ride out this bear market, and Realty Income looks like another solid candidate in that camp.

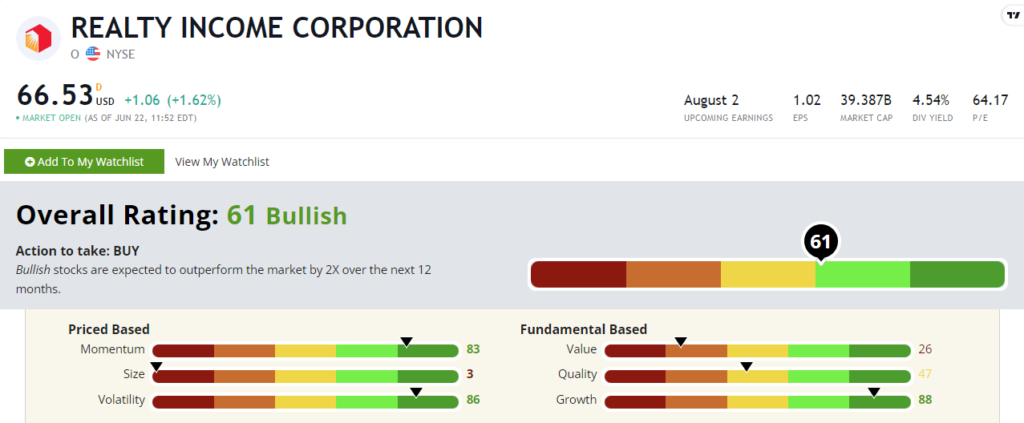

Realty Income’s Stock Power Rating

When I first wrote about Realty Income, it did not rate well. Quirky accounting hurts REITs within Adam O’Dell’s proprietary Stock Power Ratings system.

But things have changed for O in recent months. And I want to focus on three factors that are promising for Realty Income going forward in this bear market.

Realty Income now rates a “Bullish” 61 out of 100 in our system. That means it’s set to double the overall market performance over the next 12 to 24 months.

Realty Income’s Stock Power Rating on June 22, 2022.

Volatility — This is where Realty Income has improved in a huge way. The stock now rates an impressive 86 on our volatility factor. Investors looking for defensive plays amid the stock downturn are jumping into O stock.

Momentum — Realty Income’s momentum factor score has also improved in a big way since I first talked about it. The stock now boasts an 83 momentum factor rating. While the S&P 500 has lost more than 21% of its value in 2022, O is only down around 6% this year. This shows that investors who want safety are moving money into this stock.

Growth — Realty Income, despite being a conservative REIT, is actually quite the growth dynamo, rating an 88 on our growth metric. Its model of accumulating standalone, high-traffic real estate is a simple one. But it’s one that is scalable, and Realty Income’s execution has been fantastic over its life as a public company.

Bottom line: If you’re hunting for a workhorse dividend payer during this bear market, Realty Income is worth a good look.

To safe profits,

Charles Sizemore

Co-Editor, Green Zone Fortunes

Charles Sizemore is the editor of Green Zone Fortunes and specializes in income and retirement topics. He is also a frequent guest on CNBC, Bloomberg and Fox Business.

Story updated on June 22, 2022.