There has been a lot of talk of an incoming recession, but many wonder when it will actually hit as the United States draws closer to its longest period of expansion ever, which it will hit in July.

There’s no big neon sign in Times Square flashing “RECESSION” when the time finally comes. The National Bureau of Economic Research’s Business Cycle Dating Committee makes the call, and the committee tends to wait about a year to announce the end of an expansion after analyzing various factors, according to Bloomberg. So by the time it’s confirmed, the U.S. may already be a few months into the downturn.

Overall, the country’s economy has been healthy throughout the first half of the year with increased consumer spending and a solid 3.2% GDP growth in the first quarter. But that doesn’t seem to be enough as investors expect the Federal Reserve to cut interest rates soon after a poor jobs report, an extended period of lower inflation and an ongoing trade war between the U.S. and China.

In a recent survey polling economists on Bloomberg, chances of a recession in 2019 grew from 25% to 30%. Here are a few factors that economists study when trying to determine when a recession will hit.

Per Bloomberg:

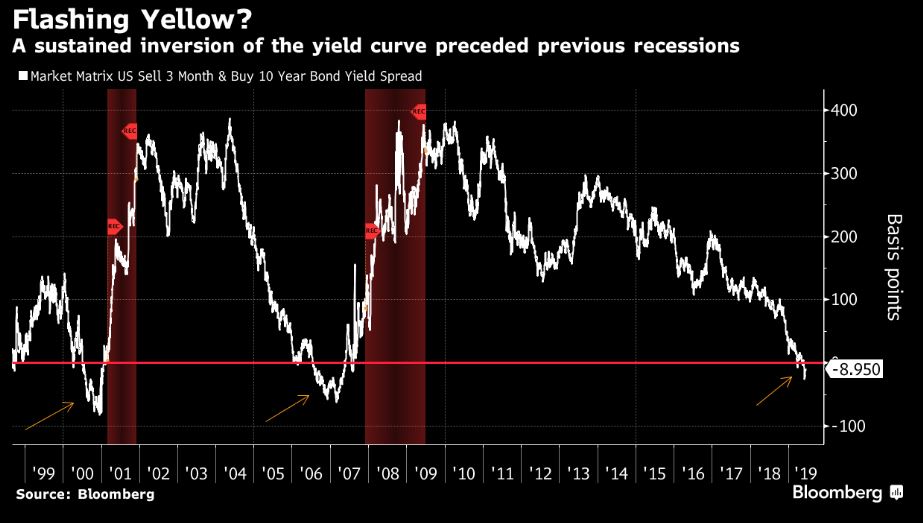

Yield Curve

The yield curve refers to the difference in rates between Treasuries with short-term and long-term maturities. Most of the time, long-term yields are higher because investors typically demand higher returns for locking up their money for a longer period. But when short-term rates are higher — known as an “inverted” curve — it’s a sign economic growth is expected to ebb, with policy rates eventually falling to cushion the slowdown.

The spread between three-month and 10-year securities has inverted before each of the last seven recessions, elevating such an event as a key signal of a future economic downturn. But it’s not automatic, and some argue central bank policies like quantitative easing have made the curve less of a direct predictor.

Credit Conditions

Another weather vane monitored by economists consists of whether borrowing conditions are getting tougher, especially for small- and medium-sized businesses. Surveys such as the Fed’s poll of senior loan officers and the National Federation of Independent Business’s gauge of credit conditions relay this type of information.

“If banks are tightening the spigot because of what they see as excesses out there and increasing risks and that sort of thing, that tends to be a leading indicator,” said Joshua Shapiro, chief U.S. economist at MFR Inc.

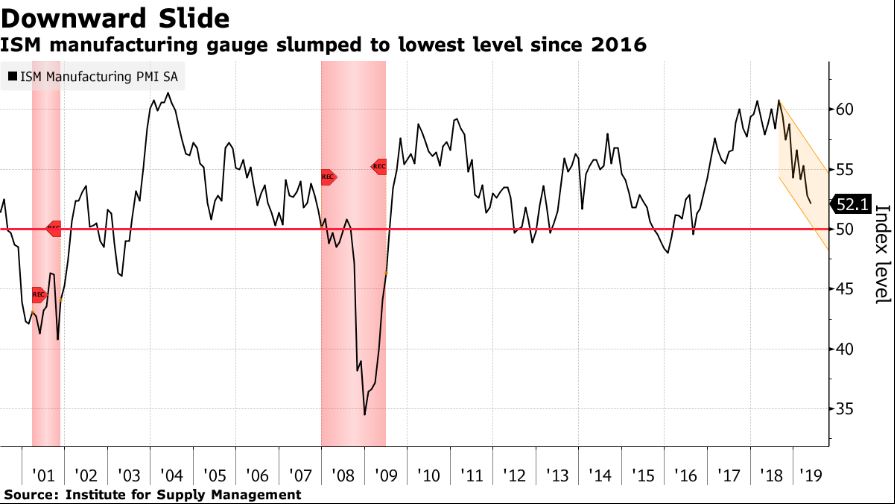

Business Sentiment

Surveys like those from the Institute for Supply Management offer a snapshot of economic activity among producers. In May, ISM’s manufacturing index fell to its lowest level since 2016 but still held above the 50 mark that indicates expansion.

The downward trend suggests “there’s been a lingering caution on behalf of businesses,” said Jesse Edgerton, senior economist at JPMorgan Chase & Co. “We have seen that already playing out in declines in capital expenditures, and then I think the big concern is whether it further turns into a slowdown in hiring.”

The ISM survey also contains some sub-indicators that can provide a look at what’s likely to happen like new orders and backlogs, while anecdotes in the report can flag risks like slowing demand or the negative impact of tariffs. Slow orders can precede layoffs if companies already have slack — or can be manageable if production is already stretched.

Still, manufacturing contracted in 2015 and early 2016 without pushing the economy into a recession.

Labor Signs

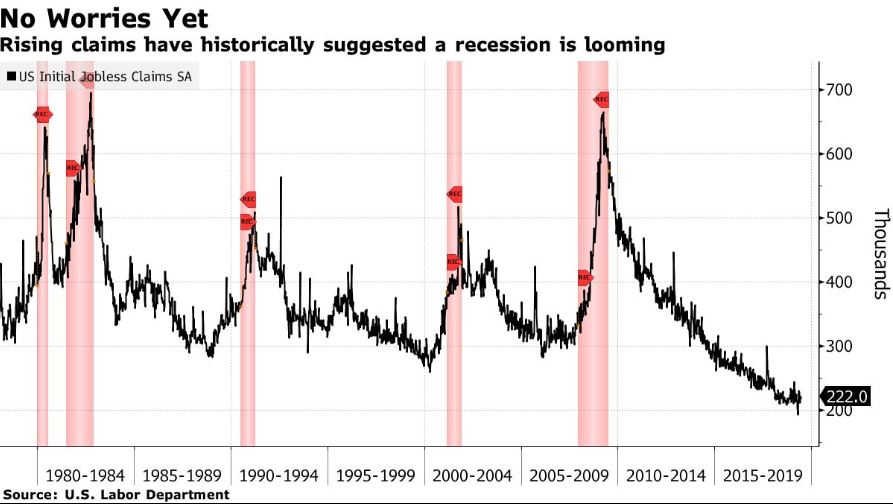

Monthly payroll data is often described as a coincident indicator — it does a good job at showing the health of the labor market in any given month. But by the time companies stop creating jobs or are even possibly laying off workers, economic weakness has already set in.

Initial jobless claims show how many Americans are applying to receive unemployment benefits and can give a sense of where the economy is headed. A significant and sustained pick-up in jobless claims suggests companies are boosting layoffs and a recession could be fast approaching.

A related leading indicator is temporary hiring. The logic goes: When times are good, businesses may recruit temporary hires to meet demand. When times are bad, temporary hires are often the first to go.

“As long as consumers and services hold, the economy holds,” said Simona Mocuta, senior economist at State Street Global Advisors.