The Federal Reserve raised interest rates from 2 percent to 2.25 percent Wednesday while signaling another hike is likely coming this December, followed by three more planned for 2019.

That’s not exactly great news.

In fact, it’s the biggest signal yet that another market crash is coming, according to a recent article in Forbes magazine.

As the stock market is hitting record highs, the current interest rate is the highest it’s been since … April of 2008, just before The Great Recession.

According to Forbes, “soft landings after rate hike cycles are as rare as unicorns.”

Forbes argues that periods of low interest rates help create credit and asset booms:

• By encouraging more borrowing by consumers, businesses, and governments

• By discouraging the holding of cash versus spending and speculating in riskier assets & endeavors

• Investors can borrow cheaply to speculate in assets (ex: cheap mortgages for property speculation and low margin costs for trading stocks)

• By making it cheaper to borrow to conduct share buybacks, dividend increases, and mergers & acquisitions

• By encouraging higher rates of inflation, which helps to support assets like stocks and real estate

These artificial credit conditions, or “malinvestments,” come crashing down once interest rates hit normal levels.

According to Forbes:

Though it can be difficult to tell precisely which investments or businesses are malinvestments in a central bank-distorted economy, a quote by Warren Buffett is extremely applicable: “only when the tide goes out do you learn who’s been swimming naked.” For the purpose of this discussion, “the tide going out” refers to rising interest rates. The mass failure of malinvestments in an economy as interest rates rise typically results in recessions or banking/financial crises.

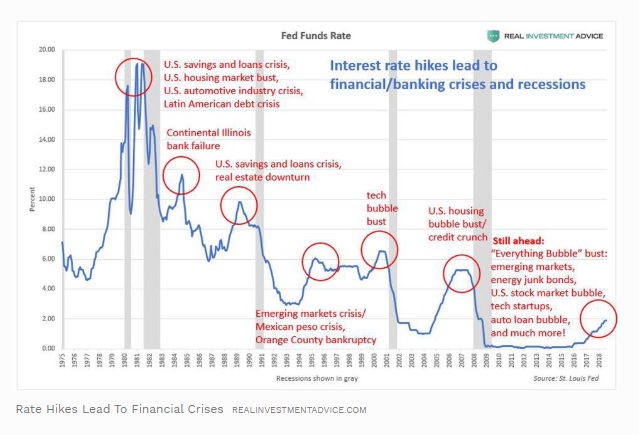

Forbes then breaks down a list of historic recessions and financial crises that immediately followed interest rate hikes.

Late-1970s/early-1980s Rate Hike Cycle

• 1980 recession: A 6-month recession that concentrated in housing, manufacturing, and the automotive industry.

• 1981 – 1982 recession: A 16-month recession in which 2.9 million jobs were lost.

• U.S. savings and loans crisis: 1,043 out of the 3,234 savings and loan associations failed as the interest rate at which they could borrow rose above the fixed interest rates on the loans that they had issued. In addition, savings and loan institutions were limited by interest rate ceilings, which caused them to lose deposits to higher-earning commercial bank accounts.

• U.S. housing market bust: Mortgage rates surged as high as 18%, which caused housing affordability to sink. As a result, existing-home sales fell by 50% from 1978 to 1981, affecting the whole industry – including mortgage lenders, real estate agents, construction workers, etc.

• Automotive industry crisis: Similar to the situation in housing,higher interest rates made automobile financing much more expensive. As a result, automobile sales plunged, causing 310,000 jobs (or one-third) in the industry to be cut.

Mid-1980s Rate Hike Cycle

• Continental Illinois bank failure: In 1984, Continental Illinois became the largest bank failure in U.S. history (until Washington Mutual’s failure in 2008). Rising interest rates and bad loans to Texas and Oklahoma oil & gas producers strongly contributed to the bank’s demise.

Late-1980s Rate Hike Cycle

• Early-1990s recession: An 8-month recession in which 1.623 million jobs were lost.

• U.S. savings and loans crisis: Higher interest rates and the U.S. real estate downturn caused a continuation of the savings and loans crisis that began in the early-1980s.

• U.S. real estate downturn: Rising interest rates caused a downturn in both commercial and residential real estate.

Mid-1990s Rate Hike Cycle

• Emerging markets crisis/Mexican peso crisis: Low U.S. interest rates in the early-1990s made higher-yielding emerging markets assets more attractive to investors. As U.S. interest rates rose, Mexico and other emerging economies experienced painful readjustments and currency devaluations.

• Orange County, California bankruptcy: Bad bets on highly leveraged interest rate derivatives bankrupted the county as interest rates rose.

Early-2000s Rate Hike Cycle

• Early-2000s recession: An 8-month recession in which 1.59 million jobs were lost after the tech bubble burst.

• Tech bubble bust: Higher interest rates helped burst the late-1990s tech bubble that was centered around internet-related companies, dot-coms, the telecom industry, etc.

Mid-2000s Rate Hike Cycle

• Great Recession: An 18-month recession in which 8.8 million jobs were lost after the U.S. housing and credit bubble burst.

• U.S. housing bubble bust/credit crunch: Low interest rates after the early-2000s tech bust led to the formation of a bubble in housing and credit. When interest rates rose again in the mid-2000s, housing prices and mortgage-backed securities plunged.

Forbes goes on to say the current “everything bubble” that’s formed after a decade of low interest rates will burst, though, we don’t know exactly when, likely ending in an even worse manner than before.

The current interest rate hike cycle won’t end any differently than the others discussed in this piece – if anything, it will likely end in an even worse manner because interest rates were held at record low levels for a record period of time. The coming recession, crisis, and bear market will be proportionate to the unprecedented imbalances and distortions that have built up in our economy.