As we approach the start of earnings season next week, something is stirring in the earnings per share (EPS) guidance data, and it’s coming from exactly where you’d expect.

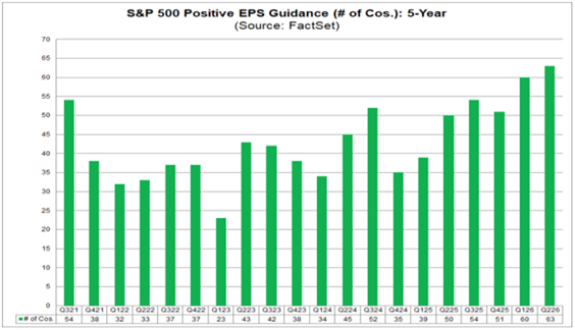

Start with the big picture. Sixty-three S&P 500 Index companies have issued positive EPS guidance for the quarter — the most in five years, and a near triple off the sorry low of 23 back in early 2023.

That’s impressive on its own. But the real story emerges when you break the numbers down by sector.

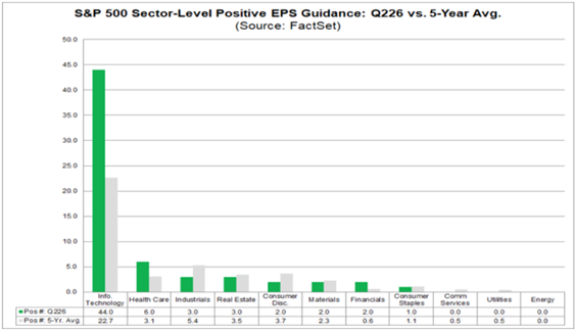

You see, this isn’t a broad-based case of corporate confidence. Of those 63 optimists, 44 are Information Technology companies.

Forty-four.

In other words, roughly seven of every 10 positive earnings guidance across the S&P 500 is coming from a single corner of the market. — That’s nearly double the sector’s five-year average of roughly 23.

No other slice of the market is even in the conversation: health care musters six, industrials and real estate three apiece and a long tail of sectors that round to a shrug. Energy and utilities? Zero.

Guidance is the closest thing corporate America has to a poker tell.

Companies don’t talk up a quarter unless they’re fairly sure they can back it up — guide high and then whiff, and the selling is immediate and merciless.

So when the chipmakers, cloud platforms and software shops raise the bar on themselves this aggressively, all at once, it’s worth asking what they see.

AI demand that still hasn’t found its ceiling? Are margins finally catching up to two years of spending? Or the kind of swagger that tends to show up right before a quarter reminds everyone that expectations cut both ways?

That’s the tension heading into next week. And there’s a slate of names lining up on both sides of it.

“Bullish” Earnings to Watch

These stocks are expected to beat their EPS from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are 10 companies that made this week’s list:

Here’s the irony of this season’s setup: the optimism lives in tech, but the season opens with the banks — and this time they look ready to make the most of the spotlight.

Next week’s slate of expected beaters reads like a lineup card from the financials dugout: Wells Fargo & Co. (WFC), The PNC Financial Services Group (PNC), M&T Bank Corp. (MTB), U.S. Bancorp (USB), Citizens Financial Group Inc. (CFG), State Street Corp. (STT), Fifth Third Bancorp (FITB) — lenders large, regional and specialized, nearly all carrying EPS estimates above where they printed a quarter ago.

Wall Street isn’t asking for anything heroic here. It’s asking them to keep doing what recent quarters suggest they already are.

The engine is net interest income.

The regional-bank complex spent 2023 and 2024 getting squeezed as deposit costs chased rates higher; that vice has loosened.

With the curve behaving and funding pressure easing, the spread between what these banks earn and what they pay has room to widen — and it flows straight to the bottom line.

That’s the quiet story behind the sequential bumps at PNC ($4.46 versus $4.14) and M&T ($4.66 versus $4.13). Neither needs a miracle, just a trend that doesn’t break.

Wells Fargo is the most interesting name on the board.

With the asset cap finally behind it, Wells Fargo can grow its balance sheet again for the first time in years — and a $1.72 estimate against $1.60 is exactly the modest boost a bank posts when it has a tailwind and every reason to prove the story’s real. Guide-and-beat is practically the playbook.

None of this is a promise — one ugly line in the credit-loss provision can undo a quarter, and “beats EPS” and “stock goes up” aren’t the same sentence.

But if you’re hunting for where next week’s positive surprises cluster, start with the group that reports first and, for once, walks in with the wind at its back.

Now, let’s look at the potentially “bearish” earnings calls for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter decline in earnings.

Here are 10 companies that passed this screen:

And here’s the twist. The same week that looks so friendly to Main Street lenders looks trickier for Wall Street’s trading houses — because the other half of the banking world reports too, and its estimates all point down.

Goldman Sachs (GS) is pegged at $14.47, down from $17.55 last quarter. Morgan Stanley (MS) $2.93 versus $3.43. BlackRock Inc. (BLK), JPMorgan Chase & Co. (JPM) and Citigroup Inc. (C) all sit below their levels from three months ago.

Some of that is just the calendar — the first quarter is seasonally the fat one for trading and underwriting, so a sequential step-down is normal. But it raises the bar: after a blistering run in capital-markets revenue, these franchises have to prove the momentum didn’t peak.

With a soft trading print or a thinner deal pipeline, the “investment banking is back” story gets a much harder look than the regionals will.

The health care and insurance names carry a different risk. Elevance Health Inc. (ELV) is expected at $6.21 against $8.00, and the whole managed-care group has spent this year fighting a medical-cost trend running hotter than anyone modeled — and there the miss usually arrives as a guidance cut, which the market punishes far more than a soft quarter.

The Travelers Cos. Inc. (TRV) ($5.15 versus $7.78) sits in the same boat: one active stretch of catastrophe losses can turn an insurer’s quarter in a hurry.

Then there’s Netflix Inc. (NFLX), the one true tech name here and the one where expectations have become the enemy.

At $0.79 against $1.23, it’s a stock priced for perfection with almost nowhere to go but sideways on good news and straight down on anything less. When a name has run this far, “fine” is a disappointment.

This isn’t a slate of broken businesses. It’s a slate of high bars, tough comparisons and stocks where the whisper number matters more than the printed one. If next week delivers a scare, it most likely starts here.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, What My System Says Today