I’m always on my guard when there’s a holiday-shortened trading week. More often than not something crazy happens in an important market to try and “paint the tape” and create a false market signal to trade against, or push the market against the direction it wants to go.

I’m to the point where I don’t trust anything I see, good or bad, during a shortened holiday week like this.

Usually, that’s bad news for gold. Gold is almost always shellacked during China’s golden week, where its markets are closed in early October. With Christmas breaking up the trading week here it allowed more honest price action with U.S. markets closed and traders inattentive, if not outright off for the week.

In many recent Decembers, gold has been the plaything of larger market forces, seeing panic selling occur into year-end. With Christmas falling on a Wednesday this year it created a strange opportunity to trade around the holiday rather than use it to shorten the week.

And with the positive spin coming out of Washington about trade talks with China fueling a reflation trade into year-end, gold pushing higher had to happen if anyone was going to believe the rallies in commodities like crude oil, copper as well as the new highs in the equity markets.

I don’t know if there is any real correlation here, but I’m to the point where I don’t trust anything I see, good or bad, during a week like this. In the end it’s irrelevant if the usual suspects are in the gold market pushing it up or down. What’s important is whether there is anything technically significant in the price move.

Since this will be my last column for 2019, I thought it would be good to assess the state of the gold market with just a couple of trading days left before the calendar turns and I go see the new Star Wars movie for a third time.

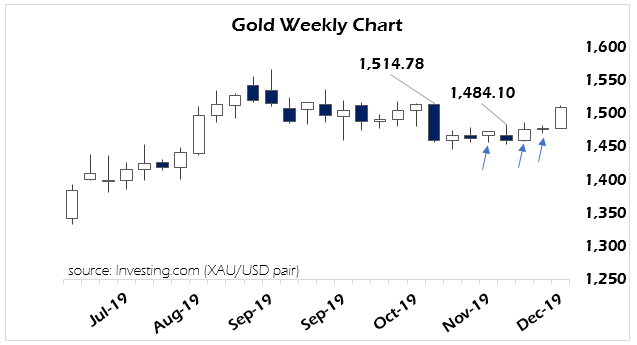

The big news this week was gold retaking the $1,500 level for the first time in two months. Gold has been either building a base or walking a tightrope for the past seven weeks, depending on your perspective.

But the signs were there that gold was closer to a breakout to the upside rather than a breakdown toward $1,400. The bulls kept supporting gold at higher and higher prices while volatility collapsed to nearly nothing (see chart, blue arrows).

Markets that can’t go down go up, and vice versa. When volatility drops to near-zero, something big is usually right around the corner.

All that had to happen was a definitive move above the most recent high at $1,484.10 (cash basis price, not futures) to get an explosion to the upside. That happened and short covering took over in a thin Christmas Eve market to take gold back above $1,500, with follow through when the U.S. markets reopened on Thursday.

But, that said, I remain unconvinced of this rally in gold without a close this week above what is clearly strong resistance at $1,515 per ounce. All this rally proves is that gold is not ready to break down. It’s not proved that it wants to go higher either.

When things like this happen, the next thing to do is go out in time a level and get the bigger picture.

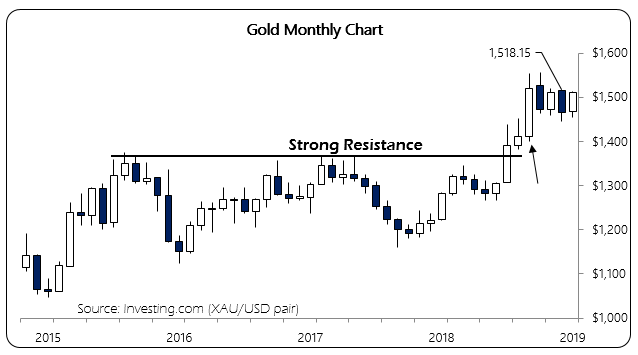

And at the monthly level gold is clearly been in a holding pattern for the past four months since peaking in early September. We’ve had a series of lower highs and lower lows each month, but within the context of the August bar (black arrow) this fall’s price action has all been nothing more than consolidation of this summer’s gains.

The key for gold going into these last trading days of the year will be closing above last month’s high of $1518.15. So far for December gold has traced an inside bar, where neither the previous high nor low were violated.

Inside bars in gold tend to be leading indicators of trend changes, so even if gold doesn’t best November’s high, that it didn’t violate November’s low is a positive sign. It indicates that the recent lows are likely to hold, and traders are getting comfortable taking gold higher after more consolidation.

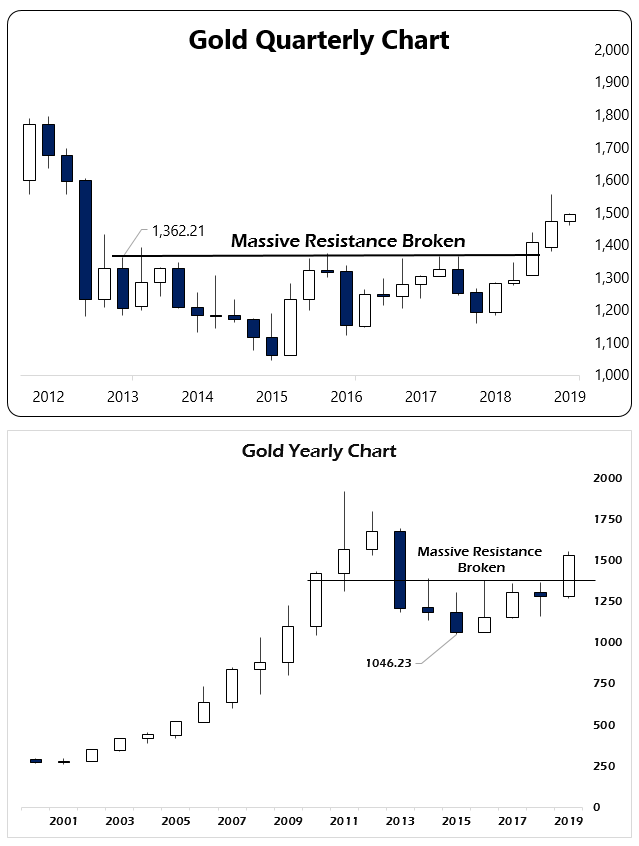

It doesn’t guarantee anything but given that 2019 saw the return to bullish quarterly and annual charts (see below) it raises the probability of a resumption of the near-term bull trend in Q1 of next year.

2019 was a great year for gold. It was also a good year for silver, now trading back above $18. Silver has a lot more technical work to do, which I’ll cover next week.

The geopolitical landscape is changing rapidly. Between dollar hoarding, which even the U.S. Treasury now has admitted is happening at a scale they don’t understand, and stock markets rising on fears of finding real yield as central banks cut rates again to stop a liquidity crisis in the offshore dollar markets at some point, something else has to give in the gold market.

It can’t continue forever as the plaything of bullion and central banks, primary dealers and prop traders. At some point, demand overwhelms synthetic supply and the price simply cannot be controlled. The Fed is learning that in the repo markets now.

Investors in 2020 will learn it from the gold and silver markets.

• Money & Markets contributor Tom Luongo is the publisher of the Gold Goats ‘n Guns Newsletter. His work also is published at Strategic Culture Foundation, LewRockwell.com, Zerohedge and Russia Insider. A Libertarian adherent to Austrian economics, he applies those lessons to geopolitics, gold and central bank policy.