After a disastrous end to January which saw the Dow Jones shed more than 600 points last Friday, U.S. markets re-opened this week with a vengeance. China’s market reopened along with a massive liquidity injection by the People’s Bank of China (PBoC), and that sent U.S. stocks soaring, taking back all the ground lost and inching to a new all-time high on the Dow Jones Industrials.

It didn’t hurt matters that the matter of impeaching President Donald Trump was finally laid to rest and the president’s State of the Union address was a huge hit beyond his base. Markets seemed to sense that the political insanity that has paralyzed D.C. for the past few months is behind it and the risk of a catastrophic outcome was gone.

That gave bulls enough of a lift to buy the dip. Risk-on was the trade early in the week as equities made big gains, gold was shellacked to retest the 2018 high, previous resistance and oil bears took profits off the table.

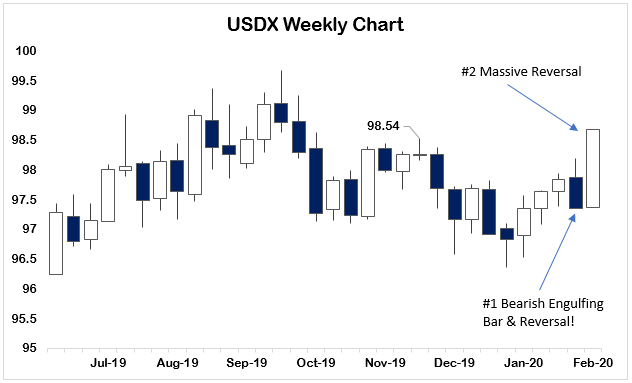

But to me, the big story of the week was the U.S. dollar. And this is where that increase in political stability becomes a two-edged sword. The dollar sold off hard last week alongside U.S. equities, throwing a significant technical signal to the downside (see chart point No. 1).

After a three-week uptrend the dollar paused, and last Friday’s action should have had bulls running for the hills — but that’s not what occurred. As the coronavirus story got worse and China returned to the market, the dollar caught a big bid.

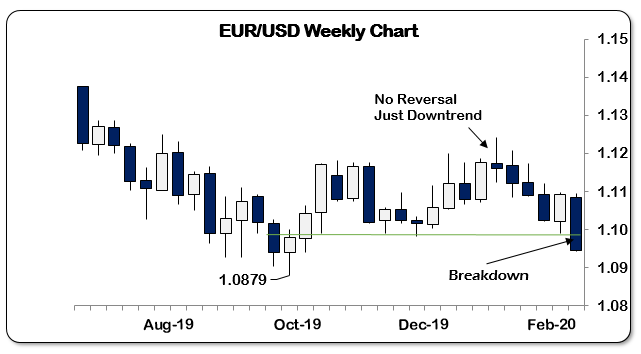

And at the same time, the euro collapsed. In my mind, last Friday’s big dollar sell-off was about keeping the euro from printing a bearish January closing price below $1.10, which would have started a stampede coming into February.

That rally corralled that stampede for all of 48 hours, because once Europe opened on Sunday evening the euro began sliding.

The result was the rally this week in the dollar negating not only last week’s breakdown but also busting through the November high of 98.54 in the process. (see above chart point No. 2). This is an instance of back-to-back reversal signals indicates a huge change in sentiment as the market ended one week thoroughly mispositioned and forced a complete rethink by traders of the situation.

And the situation in China is far worse than anyone wanted to believe a week ago. With hundreds of millions of people under quarantine, the effect on global supply chains will be real and lasting as we push through the rest of Q1.

So if that’s the case, why are U.S. equity markets rallying?

Well, in truth, they aren’t. They are now in a violent chopping pattern with volatility rising. After making a new all-time high on Thursday, stocks couldn’t follow through on Friday to close out the week.

Expect a lot of this schizophrenic behavior as capital sloshes from stem to stern trying to figure out where it should best be deployed in this age of central bank heroin.

The central banks are still desperate to keep a lid on volatility to extend the lie that they have things under control, but if that’s the case then why is the Fed still having to deal with repo market interventions being oversubscribed and the rate creeping back up toward its target Fed Funds rate and IOER (Interest on Excess Reserves)?

And the longer this goes on the more the pressure builds up within the financial markets for another explosion of risk like we saw last September when SOFR blasted out to above 10%, which precipitated the Fed intervening in the repo markets and monetizing $60-80 billion in short-term debt.

They’ve lost control over the short end of the yield curve.

And any external shock to the global flow of dollars and the ability of people to service their dollar-denominated debts is a potential catalyst for the next crisis. I’m not convinced this coronavirus is the new plague of biblical proportions, but the response to it has been substantive enough to induce panic dollar hoarding globally.

Go back and look at the chart above, if you don’t believe me.

And when that kind of panic begins to settle in people will buy assets of high quality and liquidity regardless of price. When the panic begins, lower quality assets get sold and sold with impunity.

We’re in the slow-motion part of the stampede, there’s restlessness and the smart money is getting prepared now.

The breakdown in the euro is important. $1.10 was a major support level on both the weekly and monthly charts. This week’s close definitively below that ($1.0946) is a signal things are getting worse there and that will put upward pressure on bonds yields.

We saw a huge rally in core European debt over the past two weeks as German bunds rallied hard, but that move is likely over and to me looks like a classic “false move,” which gets a majority of players on the wrong side of the trade because of a market misread or central bank intervention, which provides the energy for an opposite move later.

And the ECB, unlike the Fed, doesn’t have the tools to create money at will to provide liquidity. With this definitive move in the U.S. dollar, stocks will churn alongside gold, oil and copper and stay under extreme pressure, and the euro will continue crashing, putting upward pressure on rates there as carry-trades unwind.

This week’s price action is telling me the most prudent course is to raise cash and get defensive before the stampede begins.

• Money & Markets contributor Tom Luongo is the publisher of the Gold Goats ‘n Guns Newsletter. His work also is published at Strategic Culture Foundation, LewRockwell.com, Zerohedge and Russia Insider. A Libertarian adherent to Austrian economics, he applies those lessons to geopolitics, gold and central bank policy.