A new year is on the horizon, and that means some changes coming to the U.S. Social Security program in 2020.

While most of these changes may be considered fairly minor, it’s still good to be in the know on how your current (or future) benefits may change as the calendar rolls over to a new decade on Jan. 1.

It’s also an example of how a program that provides benefits to more 64 million individuals, a third of which are buoyed above the poverty line by Social Security alone, is constantly adapting to changes in America’s economic situation.

Here are three ways Social Security is changing (for better or worse) in 2020.

1. Social Security Beneficiaries Are Getting a ‘Raise’

Starting off with the good (depending on how you look at it), Social Security is set to increase monthly benefit checks by 1.6% in 2020. This “cost-of-living adjustment” is a chance for the Social Security Administration to reassess benefits to ensure they are keeping up with economic factors like inflation.

That means a $24-per-month raise to the average benefit check of $1,503, according to the Social Security Administration. But 2020’s COLA is down considerably from the 2.8% increase beneficiaries saw in 2019.

Furthermore, the Senior Citizens League has found that Social Security’s buying power is down 33% since the year 2000, and that’s because the CPI-W inflationary index isn’t a good representation of what seniors actually spend their money on from month to month.

It also doesn’t help that Medicare Part B premiums are increasing by another 7% in 2020, which will eat up a good portion of that COLA bump, especially if you are on the lower end of the income scale for Social Security.

2. Social Security Will Tax More Income in 2020

Social Security is mostly funded by a 12.4% payroll tax that drew in $885 billion of its $1 trillion collected in 2018. The maximum taxable earned income (wages and salary, not investment income) for 2019 was $132,900, so any wages above that number was safe from the tax.

Social Security is mostly funded by a 12.4% payroll tax that drew in $885 billion of its $1 trillion collected in 2018. The maximum taxable earned income (wages and salary, not investment income) for 2019 was $132,900, so any wages above that number was safe from the tax.

That number is going up $4,800 in 2020, though, to $137,700. While this doesn’t affect 94% of the American population, high-income earners will have to contribute a bit more to the program. That’s only up to an extra $595, but it could help bring in a little more for Social Security that is projected to be insolvent by 2035.

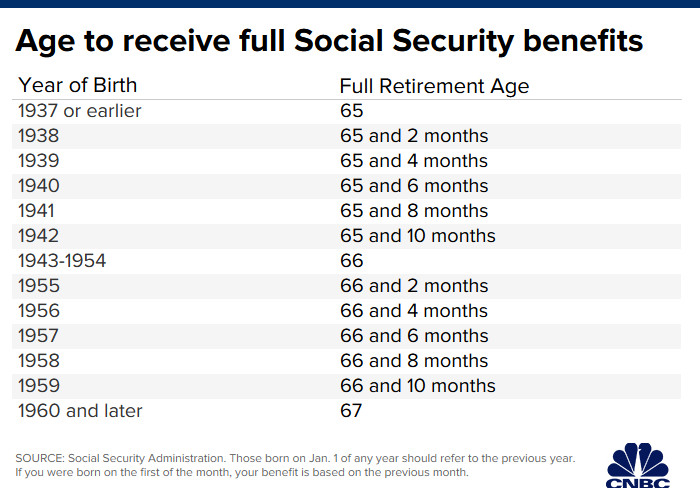

3. High-Income Earners Will See Larger Social Security Benefits at Full Retirement Age

So while high-income earners will probably have to contribute a bit more each year with an increase in the payroll tax cap listed above, they will also see an opportunity for a larger benefits check at full retirement age.

The Social Security Administration defines the full retirement age as the exact age that you can start receiving your full benefits check from the program. For most people this is between ages 66 and 67, depending on when you were born. Check out this chart to find your full retirement age, per CNBC:

The SSA announced that the maximum monthly Social Security check will be rising $150 to $3,011 in 2020, which means that if you earned enough in your 35 years the administration uses to calculate your benefits, you’ll be getting a decent monthly raise. That’s up to an $1,800 extra per year, and it means the maximum you could receive from the benefits program jumps to $36,132.

Some Social Security changes are coming, and that may mean good, or bad things for your wallet in 2020.

• You can find all of the latest and most important news about Social Security here on Money and Markets.

For our friends: Anyone who wants to grow and protect their money in retirement needs to hear this. For the first time publicly, Bill O’Reilly comes clean about what happened to his money.