If you wanted to get into the tech boom in recent years, buying well-known stocks such as Apple Inc. (Nasdaq: AAPL) or Alphabet Inc. (Nasdaq: GOOG) was a smart move.

Buying and holding shares of AAPL five years ago would have returned 438% to date.

On GOOG, you would have made 283%.

But in other sectors, the big names often don’t result in the best returns.

Academic research concludes that small companies beat large ones over the long run.

Using chief investment strategist Adam O’Dell’s proprietary six-factor Green Zone Ratings system, I found a small-cap stock that rates in the green in nearly every factor we use to rate stocks. This infrastructure stock jumped 361% in the last year. (Those Big Tech gains I shared above were over five years!) And this one still has strong upside potential.

We are “Strong Bullish” on this stock, which means it is poised to crush the broader market by at least three times over the next 12 months.

I’ll show you why you should act on this stock today.

Small-Caps Beat the Pants off Big Boys

Adam designed this model to rate stocks on the six factors proven to drive market-beating returns.

We run it daily on a universe of more than 8,000 stocks and generate an “Overall Rating” for each one.

These ratings range from 0 to 100, where 0 is “worst” and 100 is “best.” Anything rating over 80 is “Strong Bullish,” meaning we expect it to beat the market by a factor of three over the following 12 months.

Adam has written about all six factors — and as he’s pointed out, when it comes to the size of stocks, you get paid a “premium” to invest in small companies. The research is clear that you can make more money buying small-cap stocks than the big names.

The iShares Russell 2000 ETF (NYSE: IWM) tracks the stocks in the Russell 2000 — an index of U.S. small-cap stocks.

In the last 12 months, IWM boasts total returns of 51%. The S&P 500, which holds the largest companies, returned just 43% in that time.

This spread between small-cap and large-cap stocks will get wider in the coming months and years.

Investors can find big profits in this separation.

A Small-Cap Infrastructure Play: Intrepid Potash Inc.

Intrepid Potash Inc. (NYSE: IPI), based in Denver, Colorado, produces and sells potassium chloride and salt used in several applications:

- Fertilizer

- Components for drilling and fracturing fluids used in oil and gas wells.

- Nutrients in animal feed.

- Road and walkway treatment.

- Metal recovery.

The company also produces magnesium and water used in agriculture, animal feed, and the oil and gas industry.

Its Intrepid Trio product is a mix of potassium chloride, magnesium and sulfur that improves water efficiency and increases resistance to pests and diseases in plants.

From 2017 to 2019, the company saw a rise in its total annual revenue. Over those three years, Intrepid increased its top-line revenue by 25%.

COVID-19 stopped oil and gas exploration and curbed agriculture expenditures. The company’s total revenue dropped below its 2018 revenue figures.

However, oil and gas activities are returning to pre-COVID levels, and farmers are more confident spending money to bolster their operations.

Projections suggest Intrepid will benefit from this return to normal. It expects total revenue to hit $229.5 million by the end of this year and jump to $247.9 million by the end of 2022 — a 65% increase in top-line revenue from 2020 to 2022.

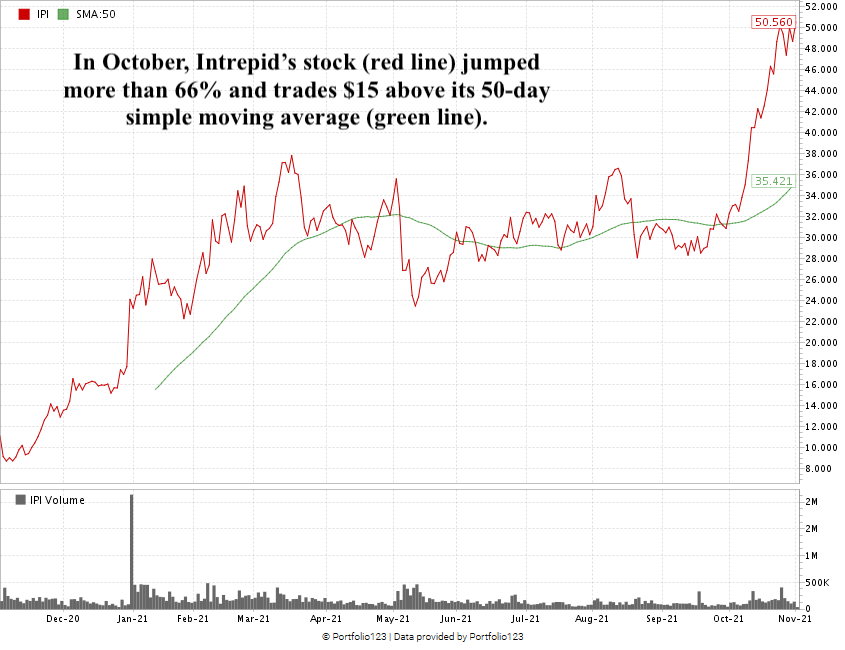

Intrepid’s stock skyrocketed from $16 per share at the start of this year to over $37 in mid-March — a 137.5% jump in three months.

After bouncing between $24 and $36 in the fall, the stock took off and gained more than 66% in October — and over 361% in 12 months!

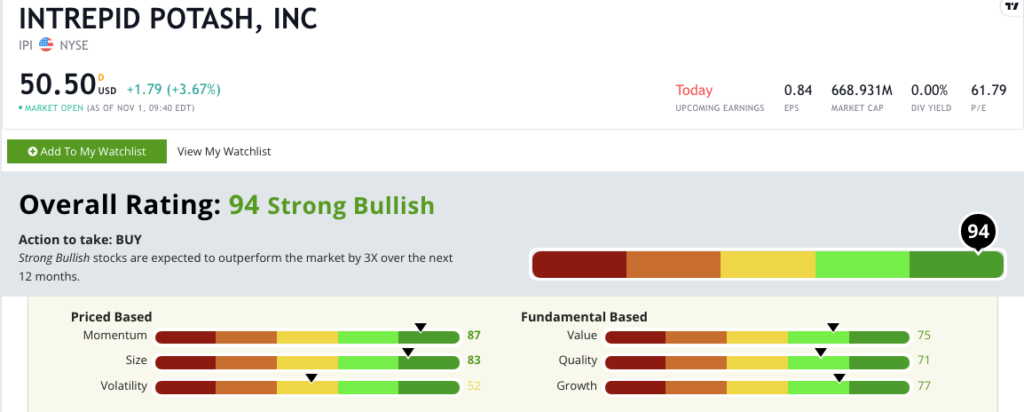

Intrepid Potash’s Stock Rating

Using Adam’s six-factor Green Zone Ratings system, Intrepid Potash scores a 94 overall. That means we are “Strong Bullish” on the stock and expect it to outperform the broader market by three times in the next 12 months.

Intrepid Potash's Green Zone Rating on Nov.1, 2021.

Intrepid Potash’s stock rates in the green in five of our six factors:

- Momentum — Intrepid’s big run in October — a 66% upswing — indicates that it’s in line for what Adam calls “maximum momentum.” The company scores an 87 on momentum.

- Size — The company’s market cap of $668.9 million makes it the perfect size for all the stocks we rate. It scores 83 on this metric.

- Growth — The company’s prior quarter sales growth rate of 46.2% and prior quarter earnings per share growth rate of 313.9% earn it a 77 on growth.

- Value —Intrepid trades with a price-to-sales ratio of 2.8 compared to the mining industry average of 15.5. Its price-to-book ratio is 1.5, while its industry peers average 3. The company earns a 75 on value.

- Quality — The company’s returns on assets, equity and investments are all in the green while industry peers average double-digit negatives. Intrepid earns a 71 on quality.

Intrepid scores a 52 on volatility, which is neutral, but its run to a new 52-week high suggests it’s starting a run for maximum momentum.

Bottom line: We’ve established that small-cap stocks outperform larger ones. I don’t think that will change anytime soon.

Sectors such as oil and gas, infrastructure, and agriculture move closer to pre-COVID-19 levels of spending and activity.

So why not look for a stock that ticks all those boxes?

Intrepid Potash Inc. is a stock to add to your portfolio.

Safe trading,

Matt Clark, CMSA®

Research Analyst, Money & Markets

Matt Clark is the research analyst for Money & Markets. He is a certified Capital Markets & Securities Analyst with the Corporate Finance Institute and a contributor to Seeking Alpha. Prior to joining Money & Markets, he was a journalist and editor for 25 years, covering college sports, business and politics.