Today, I respond to a viewer who asked for an analysis of a major multi-state operator (MSO) in the cannabis market: Aurora Cannabis Inc. (Nasdaq: ACB).

Bruno from Portugal emailed me recently:

Good afternoon. First, thanks for the information shared in YouTube, which I follow. My question is very simple: Is Aurora Cannabis a good buy at the moment because it is at a very low price? Would love some credible predictions.

Bruno, thank you for your question! I hope things are going well for you across the Atlantic.

First, let’s get a little background on the company.

Aurora Cannabis Inc. Analysis

Aurora Cannabis produces and distributes cannabis in Canada and internationally. It produces various strains of dried cannabis, cannabis oil, capsules and topical kits for medical patients.

The company sells products under several brand names, including:

- Aurora

- Aurora Drift.

- San Rafael ’71.

- Daily Special.

- AltaVie

- And CanniMed.

Aurora Cannabis has a market cap of $302.9 million. That makes it the 15th largest cannabis company in the world based on market cap.

The company purchased $20 million of senior convertible notes to reduce its total debt. The total cash interest savings from the purchase is about $7.5 million.

Aurora also received EU GMP (good manufacturing practice) certification for its medical cannabis production facility in Germany. This gave it a leg up in the EU’s largest cannabis market.

This seems like good news, but let’s look at how ACB stacks up on our Cannabis Power Ratings system.

Aurora Cannabis scores a “Bearish” 35 on the ratings system.

This tells us we should avoid this stock — for now.

Remember, the ratings system ranks all cannabis stocks against each other using two metrics: stock momentum and value.

The stock scores a paltry 8 on momentum. On the other hand, investors selling ACB over the last 12 months have driven its value score up to a “Bullish” 83.

Let’s break down the value metrics.

Aurora Cannabis is a better value compared to its industry peers. The ratings system compares Aurora against the agriculture industry — which is viable, considering it cultivates its product.

The company’s price-to-sales ratio is 1.61, compared to the industry average of 3.64. ACB’s price-to-book value is 0.33, and the agriculture industry peer average is 1.08.

You can see that Aurora has “N/A” under price-to-earnings (P/E). This means the company has a negative P/E ratio.

Let’s dig into Aurora Cannabis’ revenue to see where it’s headed.

From 2018 to 2020, Aurora Cannabis’ total annual revenue jumped 327.3%.

However, sales declined in the following years.

By the end of this year, it’s expected that ACB’s total sales will be around $173 million — 17% lower than its high in 2020.

But those sales should turn around starting next year. By 2024, the company‘s total annual revenue is expected to grow to $204.3 million — or 18.1% higher than this year.

It’s going to be hard for Aurora Cannabis to turn a profit in the years to come.

Aurora Cannabis Momentum

Aurora recorded $48 million in sales for the first two fiscal quarters of 2022. However, those sales dropped to $40 million in its fiscal third quarter.

ACB Lacks Momentum

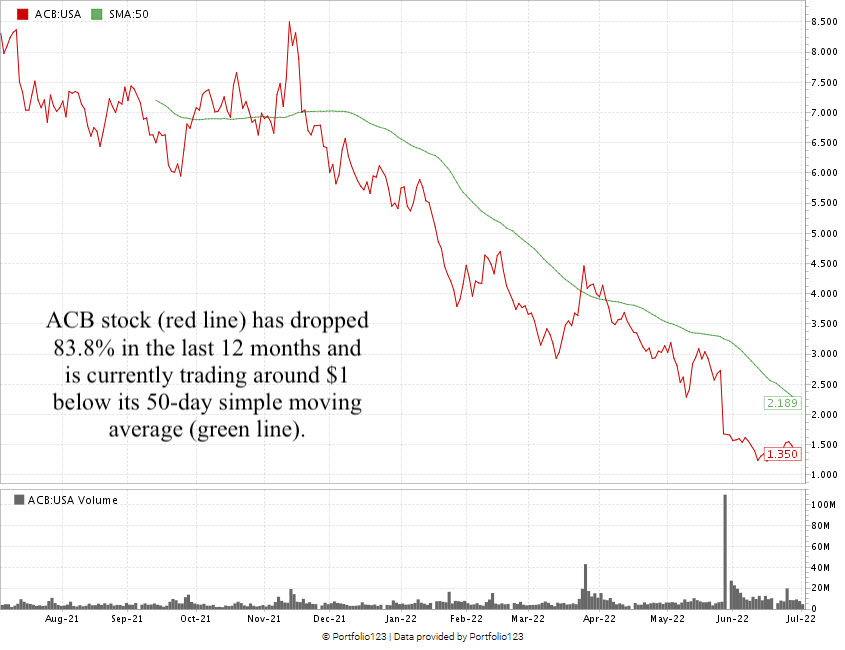

As I write, Aurora Cannabis stock has plummeted 83.3% over the last 12 months. That’s a more significant drop than many other cannabis stocks.

The stock dropped almost 40% at the end of May 2022, after it reported sales were down $8 million from the previous quarter.

The stock price is at its lowest level in history. It’s even lower than when ACB first entered the public market in 2015.

So, Bruno, to answer your question: Yes, ACB’s free-fall turned the stock into a great value. But I like stocks with a confirmed uptrend.

Aurora Cannabis doesn’t fit that description at the moment.

ACB’s Future Potential

You may be inclined to buy a dip here, but I don’t know if this is the end of ACB’s drop.

It is a good value at its current price, but you risk additional losses in the immediate future.

I think there is a good long-term prospect for ACB, especially with its recent facility approval in Germany. Still, institutional investors aren’t going to drive the price up just because of that.

They want to see much better sales for the company, and I don’t see that happening until 2023.

Bottom line: For me, it’s better to hold off and preserve some capital to buy in when there’s a confirmed uptrend in the stock.

That’s all for me this week.

One more thing: Any questions? You can get Money & Markets swag by submitting a question for me, Adam O’Dell or Charles Sizemore that we’ll use in any of our videos. Just send us your questions and feedback.

Where to Find Us

Make sure you subscribe to our YouTube channel and get notified each and every time we post a new video.

We have a lot of great weekly video features on our channel, including:

Ask Adam Anything — Where I get to sit down with Chief Investment Strategist Adam O’Dell and ask him any question (from you or me) and get his insights into the stock market.

Investing With Charles — Green Zone Fortunes co-editor Charles Sizemore and I talk about all things related to stocks and the economy, including comparing stocks to give you the best investment advice.

The Stock Power Podcast — Our weekly podcast where I show you the trends and analysis that moves the market.

All these series are on our YouTube channel.

Also, you can follow me on Twitter (@InvestWithMattC), where I’ll give you even more insights, not just in the cannabis market. You can also check out my new Stock Power Daily series on the Money & Markets website. I give you a new stock every day that I expect to outperform the market based on our proprietary Stock Power Ratings system.

Safe trading,

Matt Clark

Research Analyst, Money & Markets