I’m not a fan of shopping for a new car.

I go into a dealership knowing exactly what I want and, more importantly, how much I am willing to pay to get it.

The problem is that salespeople often want to get you into something either you don’t want or can’t afford. That’s where the higher margins are.

I’ve always stuck to my guns, but millions of Americans every year fall into the trap of buying something they can’t realistically afford.

I mention that because I came across interesting data related to auto loans. I’ll share that today and explain what it tells me about the broader economy.

Auto Delinquency Rates Hit High-Water Mark

When you take out a loan for a new vehicle … or anything for that matter … you are promising to pay back the principal (price of the item) plus interest.

Interest is where banks and other lenders make their money on the loan.

And because the Federal Reserve has raised its benchmark interest rate, banks and lenders have been forced to raise rates of those loans to keep making money.

The average interest rate on a five-year loan for a new vehicle was 3.87% in October 2022. As of September 2023, that average has almost doubled to 7.51%.

A $30,000 vehicle on a five-year loan with a 3.87% interest rate would cost you around $550 per month. Throughout the loan, you would pay an additional $3,044 in interest payments.

Today, with a 7.51% interest, that same vehicle costs over $600 a month with $6,076 in interest payments.

Higher payments, coupled with higher inflation across the board, have led to some chilling numbers in auto loan delinquencies.

Auto Delinquency Rates Hit High-Water Mark

When you take out a loan for a new vehicle … or anything for that matter … you are promising to pay back the principal (price of the item) plus interest.

Interest is where banks and other lenders make their money on the loan.

And because the Federal Reserve has raised its benchmark interest rate, banks and lenders have been forced to raise rates of those loans to keep making money.

The average interest rate on a five-year loan for a new vehicle was 3.87% in October 2022. As of September 2023, that average has almost doubled to 7.51%.

A $30,000 vehicle on a five-year loan with a 3.87% interest rate would cost you around $550 per month. Throughout the loan, you would pay an additional $3,044 in interest payments.

Today, with a 7.51% interest, that same vehicle costs over $600 a month with $6,076 in interest payments.

Higher payments, coupled with higher inflation across the board, have led to some chilling numbers in auto loan delinquencies.

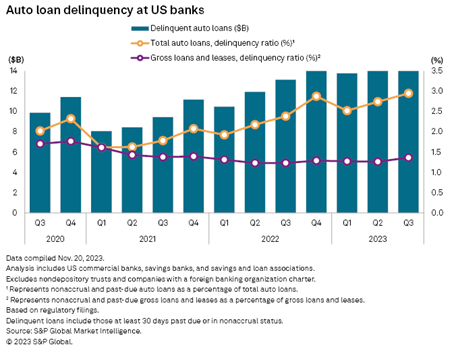

Source: S&P Global.

In the third quarter of 2023, the auto loan delinquency ratio jumped to 2.95% — up 20 basis points from the previous quarter and 56 basis points from the same time a year ago.

It’s the highest the ratio has been in a decade … all while U.S. banks trimmed back their exposure to auto loans by nearly $3 billion from the second to the third quarter.

It means that while banks were loaning less, more Americans were delinquent on their loan payments.

Americans have racked up debt to the point they can’t pay it all back.

What This Means for the Economy

This rise in auto delinquencies tells us a good bit about the overall health of the U.S. economy.

And it isn’t great.

Higher inflation is just one reason for the increase in delinquencies. Wages not keeping up with inflation is another, along with an increase in subprime (those with lower credit scores) borrowers.

As delinquencies increase, it indicates broader economic weakness.

These delinquencies suggest more Americans are forced to make tough choices when it comes to monthly expenses.

Gas and groceries are still more expensive than they were a year ago. And, because wage growth isn’t keeping up, these essentials continue to take a bigger cut from your paycheck.

The longer auto delinquencies increase, the worse it gets for the economy because it means even those with good credit are forced to let their car payments go.

The data is alarming … and it could reverse in the coming quarters.

For now, tracking auto delinquencies is important as it gives us a window into just what kind of a landing from high inflation we will experience.

Stay Tuned: A Top Theme for 2023

As we close out the year, Chad is going to look at some of the biggest themes of this year and how related stocks rate within our Green Zone Power Ratings system.

He’s starting off with a doozy tomorrow: tech layoffs.

Until then…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets