It’s no secret that the baby boomers’ generation is facing a financial crisis, and a recent article by Real Investment Advice says the crisis will affect more Americans than the subprime crisis in 2008: The pension and retirement crisis.

There are three “legs” to the retirement “stool” (check your risk of running out of money here): Social Security, private pensions and personal savings like a 401(k) plan. According to a recent report for National Retirement Planning Week, none of those three legs are in great shape for the boomers.

- The average Social Security check is about $14,000 per year

- 23% of boomers ages 56-61 expect income from a private pension

- 38% of older boomers expect a pension

- 45% of boomers have ZERO in personal savings for retirement

I previously discussed the pension issue in the “Unavoidable Pension Crisis.” To wit:

“Using faulty assumptions is the lynchpin to the inability to meet future obligations. By over-estimating returns, it has artificially inflated future pension values and reduced the required contribution amounts by individuals and governments paying into the pension system.”

This is a critically important point to understand as it is why a vast majority of Americans are trapped in the same “quicksand” as pension funds and don’t realize it.

For years, Wall Street has espoused the “myth of compounded average returns.” This is the same myth which has not only infected pension funds, but has led to the same false sense of future financial security in personal retirement planning nationwide. An article from IBD further perpetuates this myth:

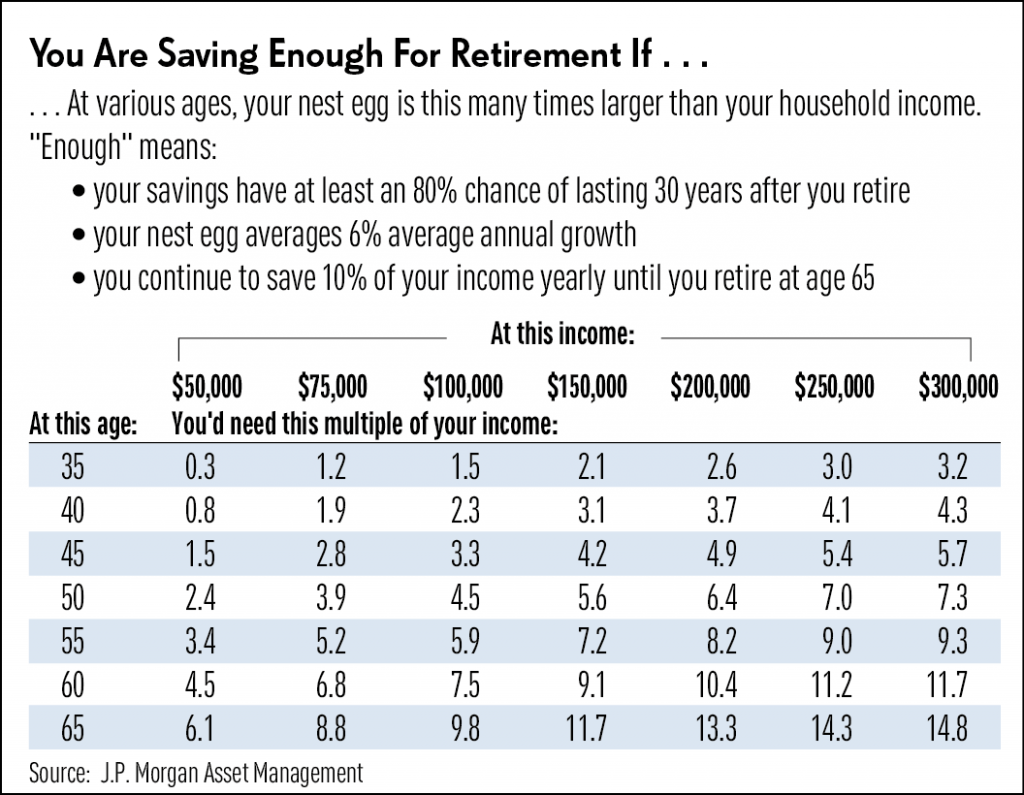

“J.P. Morgan says ‘enough’ means the nest egg is big enough to have at least an 80% chance of surviving 30 years in retirement.’

The financial firm’s number crunchers also assume that, before retirement, you keep kicking in 10% of your income each year to your nest egg. In addition, they assume that your retirement portfolio grows an average of 6% a year before retirement and 5% a year in retirement.”

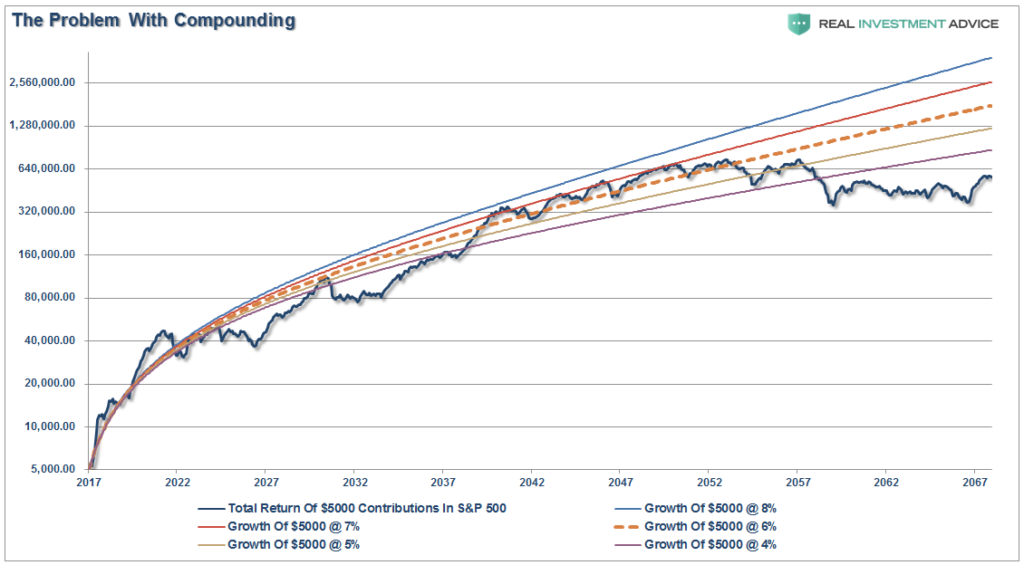

And there it is. The biggest mistake you are making in your retirement planning by buying into the “myth” that markets “compound returns” over time.

They don’t. They never have. They never will.

The chart below shows a compounded return rate of 4-8% with $5,000 annual dollar cost averaging (DCA) contributions made monthly (as noted above 10% of $50,000 which is roughly the median wage), and using variable rates of return from current valuation levels. (Chart assumes 35 years of age to start saving and expiring at 85)

Just as with “pension funds,” the issue of using above average rates of return into the future suggests one can “save less” today because the “growth” will make up for the difference.

Unfortunately, it just doesn’t work that way.

Financial Insecurity in Retirement

While we can argue about market returns, compounding rates, etc., in order for any of that to matter we have to assume Americans have money, or savings, to invest to begin with.

A new report by Forbes states that 23% (nearly one in four) Americans are saving not even one penny from their paychecks.

As part of its 2019 Savings Survey, First National Bank of Omaha examined Americans’ habits, behaviors, and priorities when it comes to saving, monthly spending, and retirement planning. The findings showed that nearly 80% of Americans live paycheck to paycheck.

The 2018 Planning & Progress Study gathered data in an online survey from over 2000 Americans over the age of 18. In that survey, they found:

- 78% said they were “extremely” or “somewhat” concerned about affording a comfortable retirement.

- 66% said there was some likelihood of outliving retirement savings.

- 21% have no retirement savings at all

- 33% of baby boomers have between $0 and $25,000 of retirement savings

- 75% of Americans reported a lack of confidence in receiving Social Security benefits and …

- 46% admitted to taking no steps to prepare for the likelihood they could outlive their retirement.

Medium reported that:

“According to a survey from Gallup, 43 percent of adults between the ages of 50 and 64 expect to rely on Social Security during retirement. This number has been steadily increasing since 2001. However, only 24 percent of respondents in the 2018 Planning & Progress Survey believe it’s extremely likely that Social Security will even be available when they plan to retire.”

That fear is likely not so misplaced as Reason noted:

“Social Security will be insolvent and unable to pay the full value of promised benefits by 2035—that’s one full year later than previously expected—and Social Security’s costs will exceed its income by 2020, according to a new report published Monday by the program’s trustees.

At the end of 2018, Social Security was providing income to about 67 million Americans. About 47 million of them were over age 65, and the majority of the rest were disabled. If nothing changes, the Social Security Trust Fund will be fully depleted by 2035 and the program would impose across-the-board cuts of 20 percent to all beneficiaries.”

Meanwhile, demographics are blowing up the basic premise of how Social Security is funded. There were 2.8 workers for every Social Security recipient in 2017. That’s down from 3.3 in 2007, and that’s way down from the 5.1 workers per beneficiary that existed in 1960.

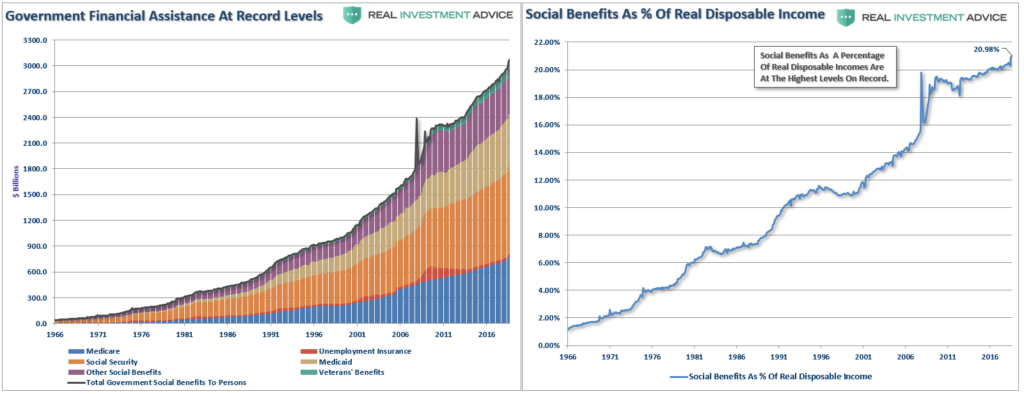

Furthermore, the two programs function mostly as a giant conveyor belt to transfer wealth from the young and relatively poor to the old and relatively rich, allowing the average person (who now lives to be 78) more than a decade of taxpayer-funded retirement. As I have shown previously, welfare now makes up the highest percentage of disposable personal incomes in history despite record low unemployment, rising wage growth, and the longest economic expansion in U.S. history.

Those entitlement programs are also the primary drivers of our national debt, which just hit $22 trillion, and the deficit, despite tax reform is now pushing in excess of $1 Trillion, which has never been seen during an economic expansion.

Won’t Or Can’t

Asking people to save “more” really isn’t an option.

The lack of savings, of course, is directly related to the rising cost of living versus the lack of wage growth over the last 35-years which led to a massive surge in debt to maintain the standard of living.

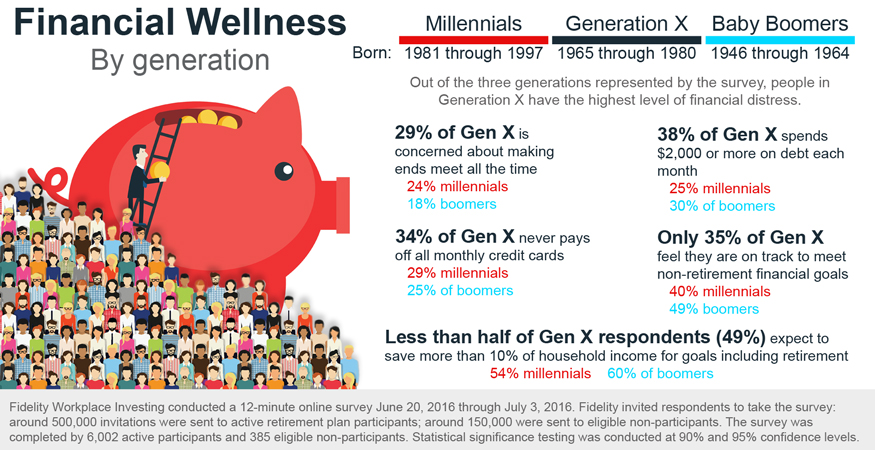

Fidelity provided some further insights into the savings problem which shows it permeates Boomers, Generation X’ers, and Millennials:

“Generation X is squarely in middle age and beset on all sides by bills. Many in Generation X have dependents at home—84% in the survey said they have at least one. They may also still be paying off their own student debts — just more than one in four survey respondents from Generation X says he or she is still paying for his or her own education.

There are all kinds of money problems, but the solutions are generally the same: Save more, spend less, or find a higher-paying job—or maybe all three. But this is easier said than done.”

The massive shortfall in “savings” is going to be a problem in the future.

But everyone saves money in their 401(k) plan?

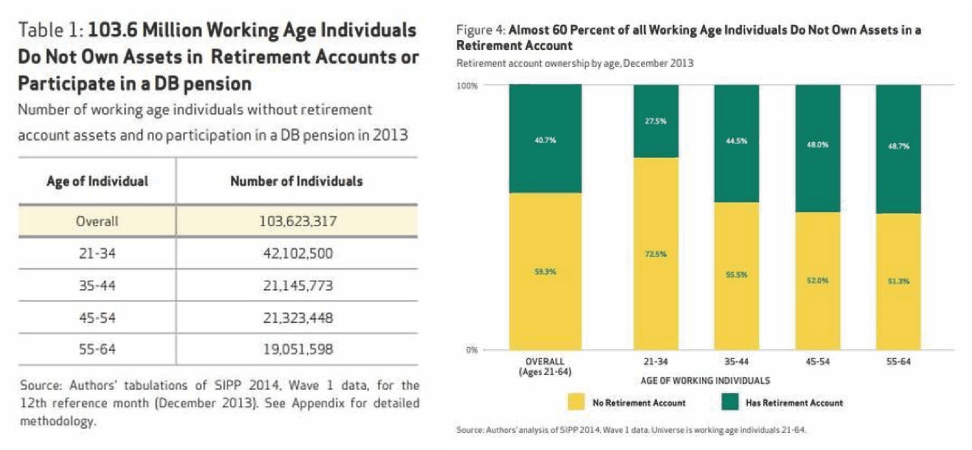

A report from the non-profit National Institute on Retirement Security which found that nearly 60% of all working-age Americans do not own assets in a retirement account.

Here are some additional findings from the report:

- Account ownership rates are closely correlated with income and wealth. More than 100 million working-age individuals (57 percent) do not own any retirement account assets, whether in an employer-sponsored 401(k)-type plan or an IRA nor are they covered by defined benefit (DB) pensions.

- The typical working-age American has no retirement savings. When all working individuals are included—not just individuals with retirement accounts—the median retirement account balance is $0 among all working individuals. Even among workers who have accumulated savings in retirement accounts, the typical worker had a modest account balance of $40,000.

- Three-fourths (77 percent) of Americans fall short of conservative retirement savings targets for their age and income based on working until age 67 even after counting an individual’s entire net worth—a generous measure of retirement savings.

The Unsolvable Problem

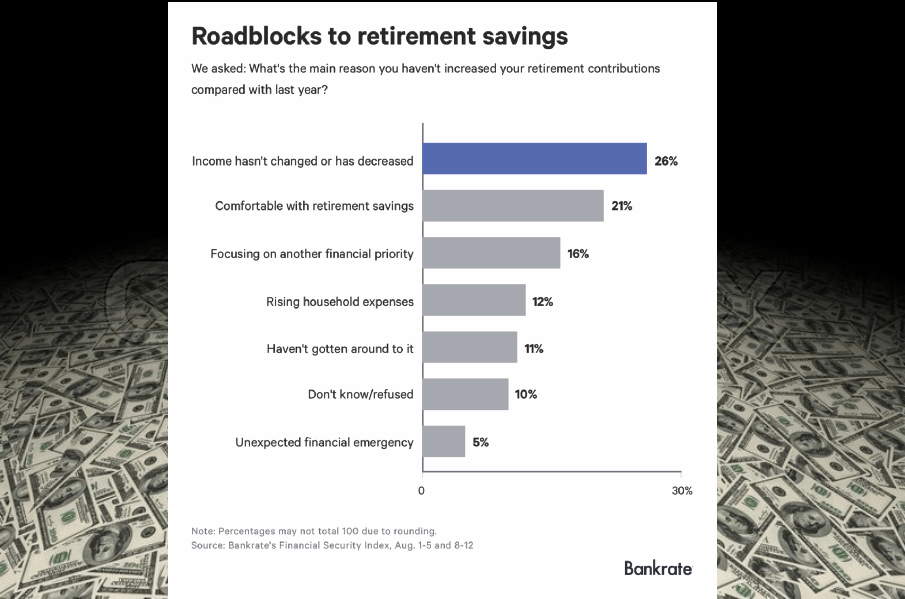

A survey from Bankrate.com touched on the issue.

“13 percent of Americans are saving less for retirement than they were last year and offers insight into why much of the population is lagging behind. The most popular response survey participants gave for why they didn’t put more away in the past year was a drop, or no change, in income.”

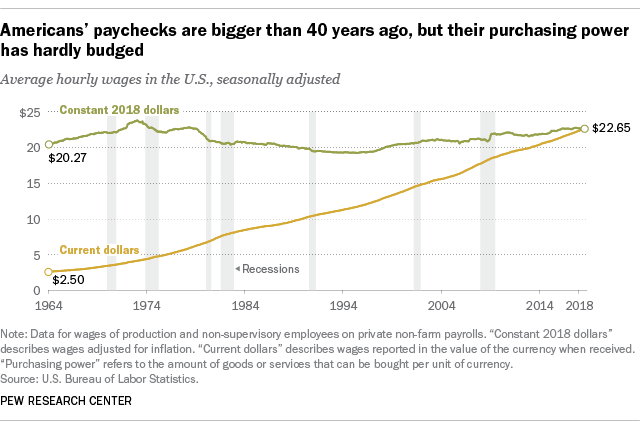

The cost of living has risen much more dramatically than incomes. According to Pew Research:

“In fact, despite some ups and downs over the past several decades, today’s real average wage (that is, the wage after accounting for inflation) has about the same purchasing power it did 40 years ago. And what wage gains there have been have mostly flowed to the highest-paid tier of workers.”

But the problem isn’t just the cost of living due to inflation, but the “real” cost of raising a family in the U.S. has grown incredibly more expensive with surging food, energy, health, and housing costs.

- Researchers at Purdue University recently studied data culled from across the globe and found that in the U.S., $132,000 was found to be the optimal income for “feeling” happy for raising a family of four.

- Gallup also surveyed to find out what the “average” family required to support a family of four in the U.S. (Forget about being happy, we are talking about “just getting by.”) That number turned out to be $58.000.

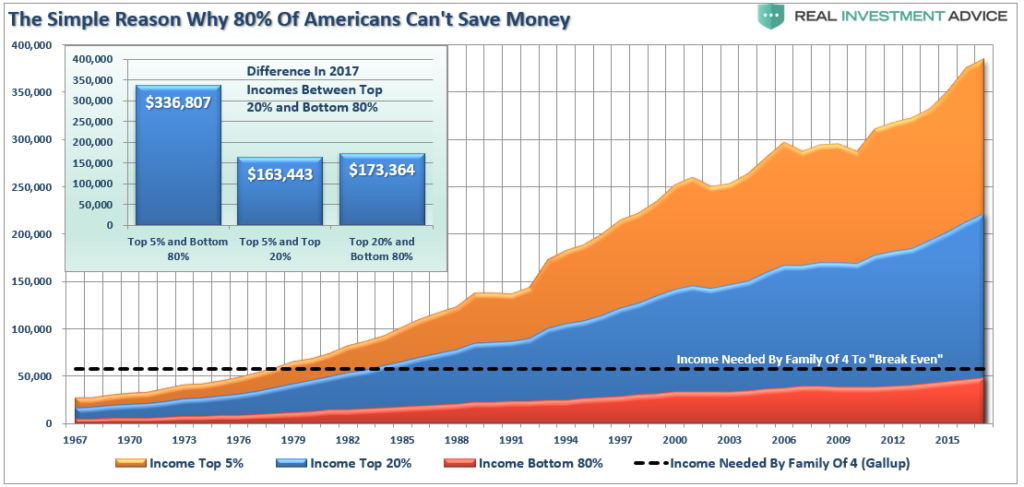

The chart below shows the “disposable income” of Americans from the Census Bureau data. (Disposable income is income after taxes.)

So, while the “median” income has broken out to all-time highs, the reality is that for the vast majority of Americans there has been little improvement. Here are some stats from the survey data which was NOT reported:

- $306,139 – the difference between the annual income for the Top 5% versus the Bottom 80%.

- $148,504 – the difference between the annual income for the Top 5% and the Top 20%.

- $157,635 – the difference between the annual income for the Top 20% and the Bottom 80%.

If you are in the Top 20% of income earners, congratulations. If not, it is a bit of a different story.

Assuming a “family of four” needs an income of $58,000 a year to just “make it,” such becomes problematic for the bottom 80% of the population whose wage growth falls far short of what is required to support the standard of living, much less to obtain “happiness.”

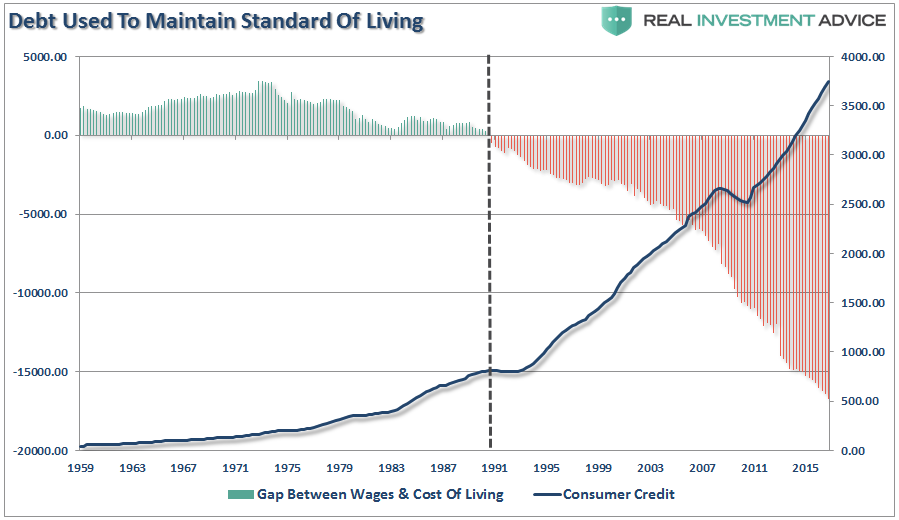

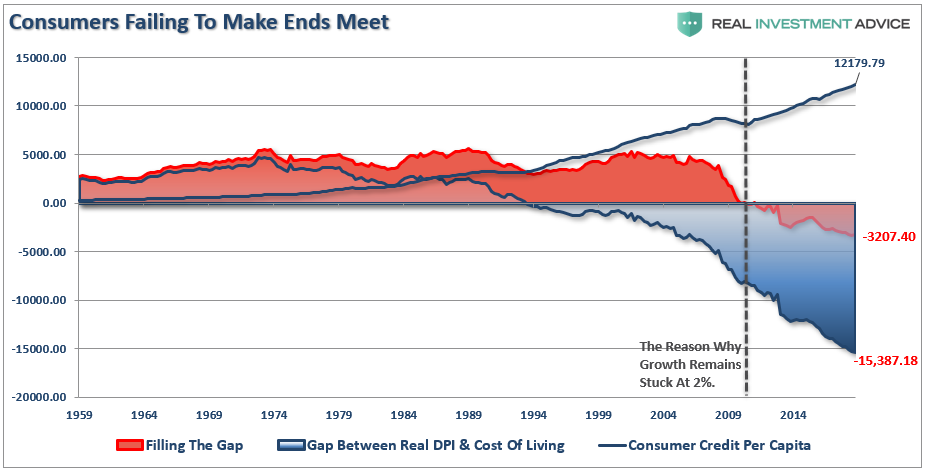

The “gap” between the “standard of living” and real disposable incomes is more clearly shown below. Beginning in 1990, incomes alone were no longer able to meet the standard of living so consumers turned to debt to fill the “gap.” However, following the “financial crisis,” even the combined levels of income and debt no longer fill the gap. Currently, there is almost a $3200 annual deficit that cannot be filled.

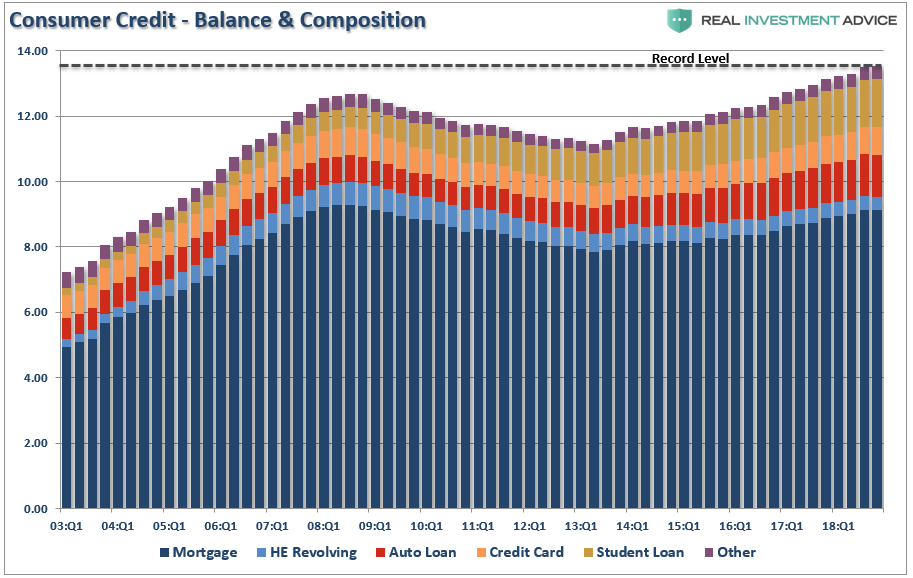

This is why we continue to see consumer credit hitting all-time records despite an economic boom, rising wage growth, historically low unemployment rates.

The mirage of consumer wealth has not been a function of a broad increase in the net worth of Americans, but rather a division in the country between the Top 20% who have the wealth and the Bottom 80% dependent on increasing debt levels to sustain their current standard of living.

With the vast amount of individuals already vastly under-saved and dependent on social welfare, the next major correction will reveal the full extent of the “retirement crisis” silently lurking in the shadows of this bull market cycle.

For the 75.4 million “boomers,” about 26% of the entire population heading into retirement by 2030, the reality is that only about 20% will be able to actually retire.

The rest will be faced with tough decisions in the years ahead.

The good news is that if Alexandria Ocasio-Cortez is correct, none of this will be a problem if climate change kills everyone in the next 12 years.