We’re in a bear market, and not all income investments are safe.

Even bonds have taken a pounding this year. Surging inflation and the Federal Reserve’s harsh response to it have pushed bond prices lower and yields higher.

I’m a big believer that dividend stocks are the superior income vehicle over time. Most dividends are taxed at a better rate than bond interest, dividend payouts come every quarter rather than twice a year and — most importantly — their yields rise over time.

Fixed income (like bonds) is just that: fixed income. It stays the same over the life of the investment.

Dividends are tied to profits. As long as a company is growing and profitable, its dividends should grow in line with those profits. (The decision to raise the dividend is up to a company’s board of directors, but they will often keep dividend growth in line with expected profit growth.)

That’s great, but not all dividend stocks are created equal. There’s one traditional dividend sector loved by the proverbial widows and orphans that I recommend you stay away from: utilities!

Avoid Utility Dividend Stocks

I’ll be straight with you.

I hate the utilities sector.

Once in a blue moon I find a company in the space I like (such as companies with appealing renewable energy developments). But as a general rule, the utility sector is full of heavily regulated, slow-growth behemoths.

As a case in point, let’s take a look at Duke Energy Corp. (NYSE: DUK).

DUK is one of the largest utility stocks in America and a mainstay in a lot of retirement portfolios. At current prices, it yields 3.6%. That’s not half bad by the standards of today’s stock market!

But Duke Energy’s dividend growth is middling at best, averaging about 3% over the past decade.

Let’s compare than to one of my favorite dividend growth machines: conservative retail real estate investment trust (REIT), Realty Income Corp. (NYSE: O).

Realty Income’s yield is a little higher at 4.2%. On top of that, its dividend growth has topped 5.8% per year over the past decade. O is close to doubling DUK’s growth rate.

What would you rather own? A premier REIT with a growing portfolio of 11,200 high-traffic properties spread across more than 1,000 high-quality tenants … or an electric utility that can’t grow much faster than the population it serves.

I think the answer is obvious.

Why DUK Is a Dividend Dud

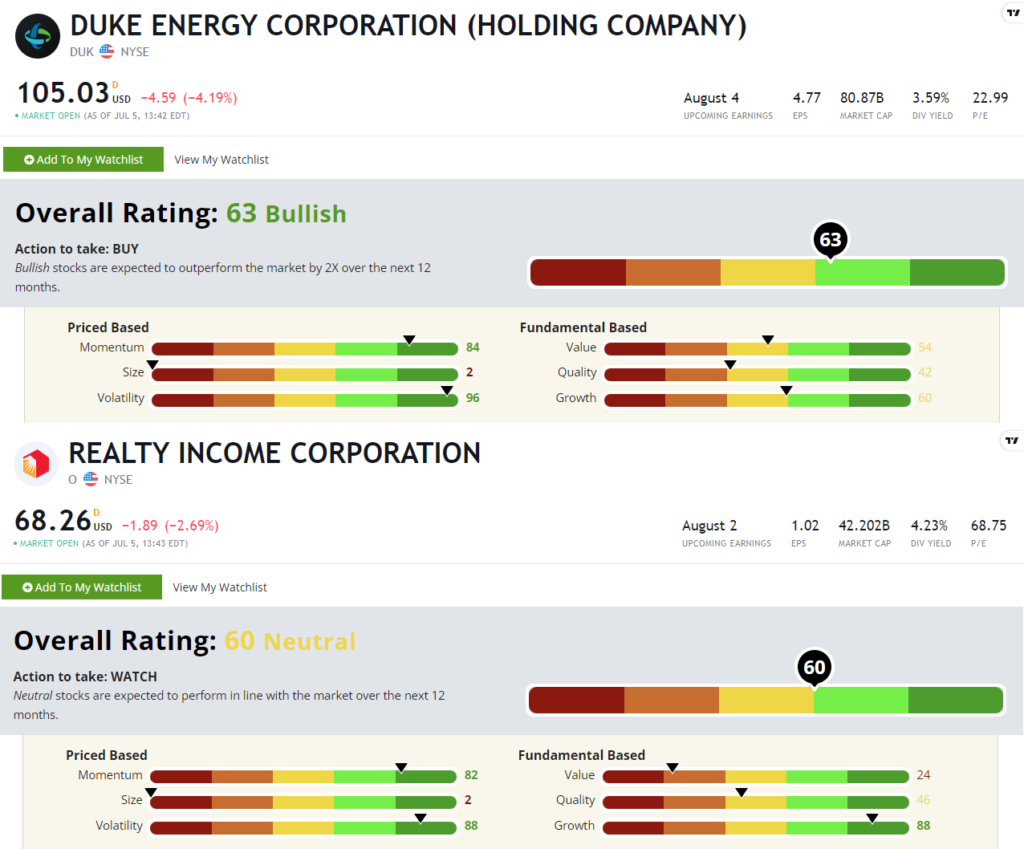

DUK rates a little higher than O on our Stock Power Ratings system right now.

Duke and Realty Income’s Stock Power Rating on July 5, 2022.

But a little digging reveals what’s going on.

On our growth factor, Realty Income rates an 88 out of 100, and DUK rates a 60. This is huge when you are looking for dividend stocks with months and years of growth potential.

These stocks both sport lackluster value and quality factor ratings, but REITs are penalized on these metrics due to strange accounting and the fact that they carry heavier debt loads. Realty Income’s ratings would be higher here without these accounting quirks.

Duke Energy stock rates as well as it does within our system because of its low volatility and its high momentum. But the ongoing bear market has created a lot of that momentum, as investors flock to defensive stocks like utilities. O’s ratings on those metrics are just behind DUK, so it’s not like the latter is exhibiting market-crushing momentum right now or anything.

Bottom line: You should always diversify your income portfolio. And I suppose it won’t kill you to have a utility stock or two in the mix.

But you’re going to be better off in REITs and other dividend growth stocks in most cases. These have a much better chance to keep pace — and even beat — inflation over time.

To safe profits,

Charles Sizemore, Co-Editor, Green Zone Fortunes

Charles Sizemore is the co-editor of Green Zone Fortunes and specializes in income and retirement topics. He is also a frequent guest on CNBC, Bloomberg and Fox Business.