Welcome to another earnings Friday.

We are just a few days away from the second-quarter earnings season, which kicks off next week. So, we have a bit to get to today.

But first, I ran across some interesting earnings data I wanted to talk about.

If you follow earnings relative to share prices, you know that the market is a little fickle.

A company can report strong earnings, but its share price falls because its forward guidance (earnings projections for the next quarter or year) is lower than what Wall Street expected.

It works the other way, too. A company can report lackluster earnings, but its share price rises because its forward guidance was better than expectations.

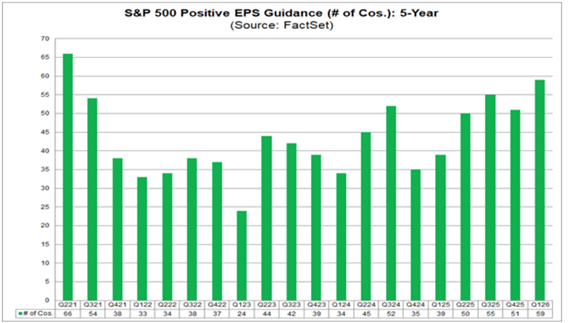

The folks at data firm FactSet compiled the number of companies in the first quarter that reported positive second-quarter guidance.

To some surprise, more companies in the S&P 500 Index provided positive guidance for the second quarter than in any quarter in the last five years.

A total of 59 companies said their earnings would be higher in the coming quarter. The last time that many companies reported higher guidance was second-quarter 2021.

On a sector level, the information technology sector had the highest number of companies issuing positive earnings per share (EPS) and revenue guidance for the quarter.

Regardless of how it pans out, it should be another interesting earnings season.

Now, before I jump into “bullish” and “bearish” earnings for next week, let me reflect on an earnings call I made last week…

DAL Surprises Analysts… and Me

Sometimes analysts don’t always get it right… me included.

Last week, I singled out Delta Air Lines Group (DAL) for potential “bearish” earnings. Analysts estimated that Delta would report EPS of $0.61, down from $1.86 in the previous quarter.

My estimation was that the recent jump in jet fuel costs — nearly $100 a barrel in a month — would eat into the airlines’ earnings.

Travel is up, but fares are too, so companies like Delta can cover the additional fuel costs.

Here’s what I said, specifically:

Therefore, I can see Delta coming in right at, or even slightly below, the median EPS estimate of $0.61 for the quarter.

Now, before I go falling on the sword, I wasn’t too far off.

Last week, Delta reported EPS of $0.64 on $14.2 billion in total revenue. So, I was partially correct… Delta came in right at estimates.

However, the company’s surprise was to the upside, which floored most analysts’ expectations, including mine.

The bigger surprise was that the company projected $1 billion in pretax profit for the second quarter, driven by increased travel demand, despite volatile fuel costs.

All I can say is that you can’t get them all right all the time.

Now, let’s examine potentially “bullish” earnings for next week…

“Bullish” Earnings to Watch

These stocks are expected to beat their EPS from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are nine companies that made this week’s list:

I’ll give you a hint… one sector will dominate both our “bullish” and “bearish” lists this week.

Of course, it’s the financial sector, as it will kick off the earnings season next week.

There is a slight difference… outside of one being “bullish” and one being “bearish”… and that is larger banks are projected to report “bullish” earnings, while smaller ones are not.

The big reason for that is that bigger banks, like Citigroup Inc. (C), State Street Corp. (STT), The Charles Schwab Corp. (SCHW) and Bank of America Corp. (BAC) have more diversified revenue streams and stronger loan growth than their smaller cousins.

Most notably, these larger banks have trading desks that serve institutional and retail investors. They make money on every trade they execute.

That trading desk income has been a big reason why larger banks are projected to see increases in EPS.

This quarter won’t be any different, as I project the five large banks that made our “bullish” list will meet or beat EPS expectations for the second quarter.

If that is the case, you can expect those bank stocks to climb higher on Adam’s Green Zone Power Ratings system.

Now, let’s look at potentially “bearish” earnings for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter decline in earnings.

Here are 10 companies that passed this screen:

As you can see, for the most part, the banks on our “bearish” list are smaller than the giants in the “bullish” list.

Again, most of the banks listed above don’t have as diversified revenue streams as those on the “bullish” list.

Therefore, their earnings are more dependent on interest income from loans and deposits. These traditional net margins have been shrinking of late, putting pressure on smaller banks to find profit.

While there may be a few surprises, most of the banks on this list will likely see quarter-over-quarter declines in EPS because of that lack of diversification.

That will put pressure on their overall ratings on Adam’s Green Zone Power Ratings system.

It should be an exciting week as the next earnings season kicks off.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets