Today is Thursday, and you know what that means.

I’ll be reviewing the stocks that recently passed the “Bullish” threshold on my Green Zone Power Ratings system.

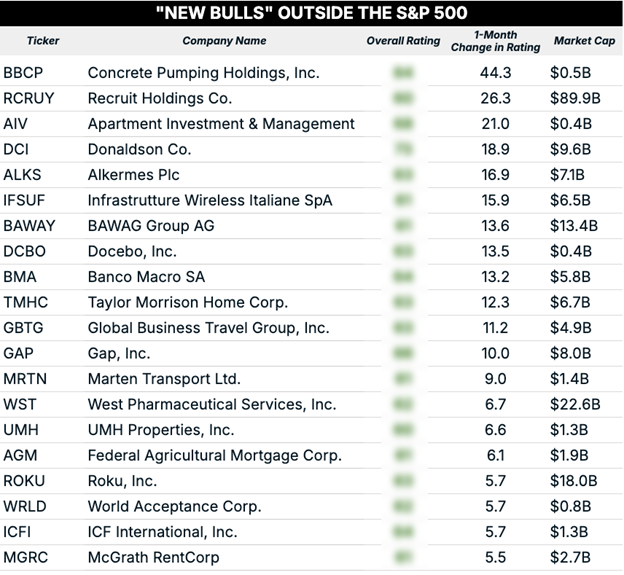

Interestingly, there were no new additions from the S&P 500 Index this week, but there were plenty of newly “Bullish” small-cap and international stocks that popped up.

So, let’s jump into it!

I ran a screen for the top 20 stocks with the largest score increases over the past month, and this is what made the cut:

Most of the new bulls this week aren’t what I would consider household names, but there were two stocks I’m betting you’re familiar with: iconic American clothing chain Gap, Inc. (GAP) and video streaming pioneer Roku, Inc. (ROKU).

Both stocks are former leaders that have struggled to regain their magic.

We’ll start with Gap. Launched in 1969, the store has been a fixture in American shopping malls for well over half a century.

Yet its annual revenues of $15.4 billion are actually lower today than they were back in 2004. Sales have been stagnant for over 20 years, and that doesn’t account for inflation.

Brands go in and out of style, and unfortunately, Gap’s core brands of Gap, Old Navy and Banana Republic just haven’t resonated with shoppers like they used to.

But could that be changing?

Let’s see what my system says…

Gap’s “Bullish” overall rating is driven primarily by its “Strong Bullish” value and quality factor ratings of 98 and 87, respectively. The company is highly profitable… and its stock is cheap.

But before you aggressively pile into the stock, keep in mind that it rates a very average 41 on its momentum rating. I recommend being patient and waiting for a more established uptrend.

Roku is also an interesting case study. Netflix, YouTube and other streaming services are currently the dominant medium for most viewers.

But streaming content didn’t just magically appear out of thin air. Roku was one of the early pioneers who built the devices that made streaming possible.

Roku was a revolutionary company… but its lack of a competitive moat held it back. Smart TVs offered access to streaming services without the need for an additional set-top box, before screentime largely shifted to mobile phones.

Roku was doomed to obsolescence. Right?

Wrong.

To start, demand for its hardware has remained surprisingly strong. Part of this is because most built-in smart TV software is horrendous.

Major TV manufacturers are notorious for failing to update their systems, and after a few years, many viewers find themselves adding a Roku, Amazon Fire TV Stick or an Apple TV to extend the usable life of the TV.

Of course, Samsung’s use of a subpar operating system is hardly a durable long-term business model for Roku. The company knows this, which is why it pivoted to licensing its software to TV manufacturers.

So, is Roku intriguing enough to buy?

The stock rates a “Strong Bullish” 81 on its quality factor, which makes sense. Software licensing is a profitable, capital-light business and as Roku transitions from hardware to licensing, I would only expect this to improve.

The stock also rates as “Strong Bullish” on its growth and momentum factors, with ratings of 98 and 82, respectively.

The stock isn’t cheap… and it tends to be volatile. But it’s been trending in the right direction for the past three years.

Bullish on Argentina

Banco Macro SA (BMA) might not be a household name, but it should be familiar to longtime Green Zone Fortunes subscribers. I recommended this Argentine bank a little over two years ago, and our position is up more than 100%.

We bought in just months after President Javier Milei took office and started his libertarian transformation of Argentina. And we’ve benefitted as Argentine assets have been repriced to something closer to a “normal country” valuation.

So, do BMA shares still have upside after the move?

Even after its 100% move, my system indicates Banco Macro is still almost ridiculously cheap. It rates a “Strong Bullish” 94 on its value factor. It also rates a “Bullish” 64 on its quality factor.

If you already own Banco Macro, I wouldn’t recommend selling it any time soon. But if you’re looking for a new entry point, I might recommend a little caution.

The bank’s momentum factor rating of 35 suggests the shares are slightly out of favor right now. You might want to wait for a more defined uptrend before putting new capital to work.

To good profits,

Adam O’Dell

Editor, What My System Says Today