Before I get into the “bullish” and “bearish” earnings for next week, I want to analyze estimates for the upcoming quarters.

We are nearing the end of this earnings season, so analysts are starting to make their projections for the first quarter of 2026 and beyond.

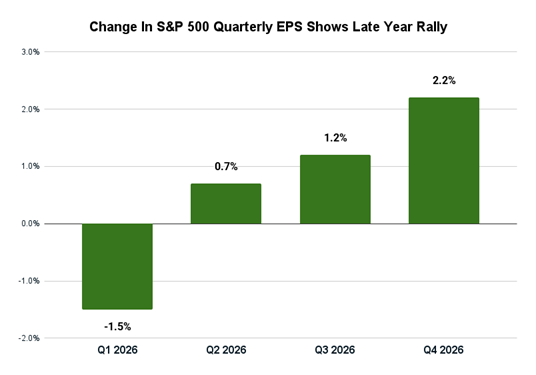

Two things stand out here:

- Analysts are starting to factor in concerns about inflation, tariffs, artificial intelligence (AI) and geopolitical instability – lowering earnings estimates for S&P 500 Index companies by 1.5%.

- The same analysts believe the concerns about all of those things are short-lived, as they are pushing estimates up through the fourth quarter.

Now, these projections have to be taken with a grain of salt.

Analysts typically reduce earnings estimates during the first two months of a quarter.

In the past five years, the average decline in S&P 500 earnings per share (EPS) estimates during the first two months of the quarter is 1.2%.

Over the past 10 years, that average decline jumps to 2.4%.

That means the latest analyst revisions appear to be right in line with data going back a decade.

The big question is whether the estimate for next quarter is cause for concern, and the answer is no.

As you can see, analysts do this all the time, so it is almost to be expected.

We’ll be able to gauge concern when the new earnings season kicks off in a few weeks.

Kroger Comes In Better Than Expected

Last week, I highlighted Cincinnati, Ohio-based grocery store chain The Kroger Co. (KR).

Expectations were that Kroger would report EPS of $1.20… nearly $3 better than the previous quarter.

However, I was feeling even more optimistic about the company because consumer spending has been on the rise – which directly benefits companies like The Kroger Co.

That thesis turned out to be correct.

Yesterday, KR reported earnings of $1.28 per share on $34.73 billion in quarterly revenue.

While revenue came in below expectations, Kroger ultimately beat earnings estimates.

As a result, KR shares were up more than 4% during midday trading yesterday.

Now, let’s examine potentially “bullish” earnings for next week…

“Bullish” Earnings to Watch

These stocks are expected to beat their previous quarter’s EPS. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are 10 companies that made this week’s list:

With consumer spending ticking higher, the uptrend has convinced analysts that retailers like Ulta Beauty Inc. (ULTA) and Dick’s Sporting Goods Inc. (DKS) will surpass their previous quarter’s earnings.

It helps that both companies tend to do better during the holiday season, which is the quarter they will report on next week.

While they are at opposite ends of the retail spectrum, I believe both will come in above their EPS estimates, proving that American consumers have not pulled back on their discretionary spending.

Beats by either or both of these companies should bolster their ranking on Adam’s Green Zone Power Ratings system.

Now, let’s look at potentially “bearish” earnings for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We target companies that a large group of Wall Street analysts expect to report a quarter-over-quarter decline in earnings.

Since we are nearing the end of the earnings season, I expanded this screen to include companies not listed on the S&P 500.

Here are five companies that passed this screen:

What stands out here is that three of these five are biopharma companies.

I mentioned in a recent podcast that I felt the biotech sector has been a bit of a sleeping giant.

As it turns out, that was a good call.

The SPDR S&P Pharmaceuticals ETF (XPH) has risen 24% over the last 12 months compared with a 17.4% gain for the S&P 500.

The main issue is that relatively new biotech companies must spend money on research and development without earnings.

Without a drug on the market, they can’t make any money.

I believe that’s what we are seeing with the three biopharma companies on our list here. All three are relatively small (with fewer than 230 employees) and somewhat new…

Sutro Biopharma Inc. (STRO) is the oldest, established in 2003, while the other two were founded in the last 10 years.

Analysts are right on about all three of these companies… Their negative earnings will get worse this quarter.

That will cause each of them to fall further on Adam’s Green Zone Power Ratings system.

That’s all from me today.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets