The PGIM High Yield Bond Fund (ISD) trades at a huge discount that’s going to disappear soon.

Before I explain why, let me tell you something else about this fund: It boasts a huge 8.4% dividend yield. In other words, you’d get $700 per month — or $8,400 a year — in income on every $100,000 invested. And you should consider getting in now, because ISD is set to soar.

A New Fund

For years, ISD provided a solid and reliable return, thanks to its strategy. The fund would buy corporate bonds that expired in just a couple years (or less), so there was less risk of any company going bankrupt or defaulting.

In addition, this lowered the fund’s risk of losing market value when the Federal Reserve hiked rates (higher interest rates tend to cut the value of bonds, especially corporate bonds).

This strategy worked well from late 2015 to the start of 2019, when the Federal Reserve hiked interest rates by a whopping 900%. U.S. Treasuries and corporate bonds could not compete with the short-term focus of ISD (in blue below):

ISD’s Short-Term View a Long-Term Win

While investors in the iShares 20+ Year Treasury Bond ETF (TLT) — in orange — and the iShares iBoxx Investment Grade Corporate Bond ETF (LQD) — in red — thought they were getting a less volatile investment, they were really just getting underperformance, as well as a lower yield (both yield about three times less than ISD).

The biggest reason for this underperformance? They tried to fight the Fed — and lost.

But things are different now, because the Fed has started cutting interest rates, and the market expects rates to fall further in the future.

ISD’s managers are sharp, though. In response to the Fed’s pivot from hiking to cutting, they simply changed the fund’s mandate. As of March 8, ISD got a name change (it used to be called the “Short-Duration High Yield Fund”, hence the S and D in the ticker) and a new mandate to invest “in instruments of any duration or maturity.”

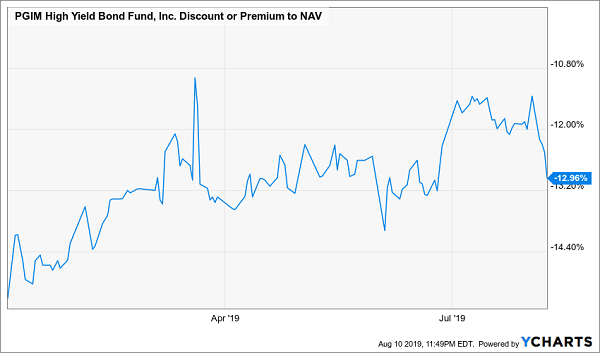

In other words, ISD changed with the Fed, adapting to the new monetary policy. When the news hit, the market rejoiced, causing a short-term spike in ISD’s discount:

The Market Approves of ISD’s Pivot

That response meant ISD wasn’t a great buy right after the news was announced, but as you can see, that spike has disappeared, and following the recent market volatility, ISD is about as cheap as it was before the fund’s mandate changed.

Yet ISD deserves a much narrower discount than its current 12.9% discount to NAV, which is one of the highest of any bond-focused closed-end fund (CEF).

Higher Payouts

Here’s why the fund deserves a higher valuation than it’s getting.

For one, ISD’s pivot with the Fed shows the fund’s managers are on the ball. They know when to get out of a strategy that no longer works for the current market, and that means ISD’s discount should disappear over time as it continues to outperform alternatives.

Since its mandate change, we’ve already seen ISD start to outperform the high-yield junk bonds in the SPDR Bloomberg Barclays High Yield Bond ETF (JNK) by a growing margin.

ISD’s Shift Starts to Kick In

That makes ISD a compelling fund to look at now, since its outperformance isn’t priced in. But there’s another reason to take a closer look: its improving dividend-growth potential.

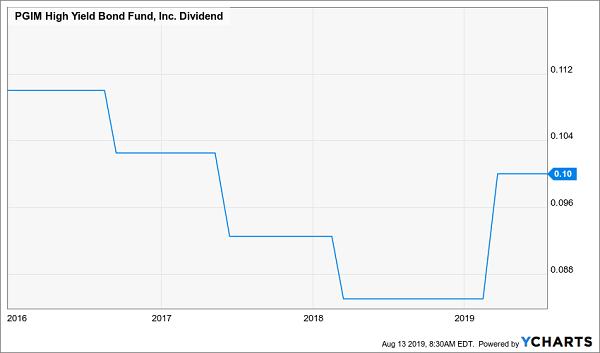

One of the problems with the Fed’s policy is that, although short-term corporate bonds didn’t fall in value from the rate hikes of 2015 to 2018, yields on those bonds didn’t rise, either. As a result, ISD saw a consistent bout of dividend cuts over the years:

Note, however, that this changed in 2019. With its new strategy in March, ISD also raised payouts slightly as its new mandate resulted in higher income to pass on to investors. If ISD continues to outperform, this may be the first in a series of payout hikes that make the fund an even bigger yielder.

As soon as those dividend increases are made public, expect ISD’s big discount to vanish, resulting in capital gains on top of its already generous income stream.

21 “Fed-Proof” Dividends — Up to 11.1% — Waiting for You Here

If you’re like most folks, the thought of falling rates leaves you in a tough spot — with Treasuries already yielding less than 2%, where the heck are you going to find the steady, high yields you need for a secure retirement?

Don’t worry. There are still plenty of terrific high-income plays out there; we just need to go a little deeper than the plain-vanilla bonds and blue chip stocks most folks limit themselves to. (And I’ve actually done that for you, as I’ll show you in a second.)

This is where CEFs come in — especially CEFs with market caps under $1 billion, which are my stock in trade.

Why?

Because this is where the biggest mispricings in investing happen. And they happen on the regular (ISD is a textbook example). We can jump on these silly discounts for maximum upside and safe, growing 7%+ dividends.

I should know: I’m the only CEF analyst in the world focused exclusively on smaller CEFs. And I’ve assembled a fully stocked portfolio of 21 funds yielding 7.6%, on average (with 6 throwing off monster payouts of 9% and up — all the way to 11.1%!).

Just click here to get instant access with no risk and no obligation.

This portfolio is the beating heart of my CEF Insider service. The buys you’ll find there are poised to hand you 7% to 15% price upside in the next 12 months, along with their massive cash dividends, thanks to the unusual discounts they’re trading at now.

There’s more: because I’ve distilled my 5 very best CEF buys now into an exclusive Special Report you’ll also get FREE. These incredible 8%+ yielders are the best of the best— the ones I see as absolute musts for every investor’s retirement portfolio.

The entire wealth-building package is just a click away: Go right here to discover my 21-fund CEF Insider portfolio for yourself and get your Special Report revealing the 5 best 8%+ yielding CEFs to buy now.

To learn more about generating monthly dividends as high as 8%, click here.

• This article was originally published by Contrarian Outlook. You can learn more about Brett Owens and Contrarian Income Report right here.