Consumers aren’t happy, but they feel a sense of relief. Gas prices are down over the past month.

At a national average of $4.66 per gallon, it’s still painful. But prices have fallen 7% from a month ago when they topped $5.

Remember, that’s a national average.

You might be paying more or less. In California, the average is more than $6 a gallon. In Georgia, it’s just $4.16.

The lowest-priced states are still high compared to a year ago, especially when compared to what we’ve historically paid for gas.

The Cure for High Gas Prices

Economists tell us that the cure for high prices is high prices.

Another way to say that is that higher prices reduce demand, and producers respond by cutting prices.

For gas, it doesn’t work that way. We need gas to get to work, take the kids to school and buy groceries. Many people have little room to cut back.

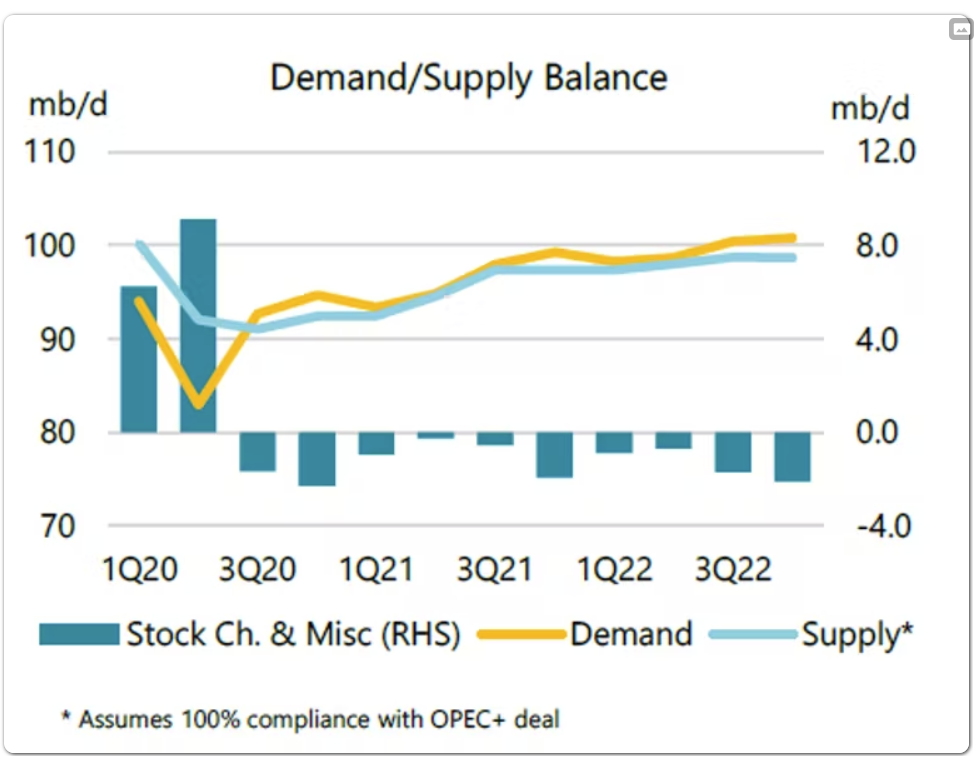

Unfortunately, consumers need to enjoy the price dip while it lasts. The chart below shows that prices are likely to rise again.

Source: Oil & Gas Journal.

Demand (yellow line) is above supply (blue line). Stock, the downward bars, represent inventories.

Basic economics tells us that prices will rise when demand exceeds supply and/or supply is declining.

Temporary Lower Gas Prices

It’s unfortunate that there is little chance of a significant supply increase.

In theory, producers should rush to drill to benefit from higher prices. But oil wells take time to develop.

In many countries, stringent permitting processes mean new wells can take years to get up and running. In other countries, the infrastructure is already delivering oil at near-maximum capacity.

Without room to increase supply and no reason to expect a significant decrease in demand, oil prices should move back up.

And gas prices should follow.

Bottom line: The current situation may be the new normal at the gas pump, and we will all have to suffer through high prices for some time.

Click here to join True Options Masters.