The COVID-19 pandemic took its toll on every sector of the market.

It hit consumer discretionary and consumer cyclicals hard as stores worldwide closed to help stop the spread of the virus.

This was more apparent in the clothing industry. Spending dropped 7.7% globally.

But now the industry is making a comeback. Stores are reopening and welcoming customers back with open arms. And just in time for the busy holiday season.

Using Adam O’Dell’s six-factor Green Zone Ratings system, I found a clothing stock that rates in the green in four of the six factors we use to analyze stocks.

The stock has risen more than 130% in the last year. And I think it still has room to run.

We are “Strong Bullish” on this stock, which means it is poised to outperform the broader market by at least three times over the next 12 months.

Let’s see why investors should buy this clothing stock now.

Clothing Spending to Surpass Pre-COVID Levels

The COVID-19 pandemic hit consumer spending hard.

According to a study by the research firm Deloitte, personal consumption spending dropped 3.9% in 2020, compared to a 2.4% expansion the year before.

The clothing industry was slammed as consumers spent 7.7% less in 2020 than they did in 2019.

But forecasts show a sharp rebound in global clothing spending over the next four years.

Globally, per capita spending on clothing and footwear dipped from $277.50 in 2019 to a 10-year low of $239.80 in 2020 due largely to stores closing brick-and-mortar operations during the COVID-19 pandemic.

Forecasts suggest, however, with the pandemic subsiding and stores reopening, spending on clothing will pick up and reach pre-COVID levels by next year.

What’s more, spending is expected to increase 37% to new highs of $329.10 by 2025.

Investors can find big profits in this spending trend.

A Specialty Clothing Stock Play: Oxford Industries Inc.

Oxford Industries Inc. (NYSE: OXM) is a specialty apparel company that distributes clothing and footwear globally. It owns several different brands, including:

- Tommy Bahama.

- Lilly Pulitzer.

- Southern Tide.

- Beauford Bonnet.

- Duck Head.

Full disclosure: I don’t own this company’s stock, but I do love Tommy Bahama apparel. You can see me wearing it in several of our videos on YouTube.

The Atlanta-based company sells clothing and footwear for men, women and children along with furniture, swimwear, toiletries and even cigar products and stationery.

It operates 187 brand-specific full-price retail stores, 20 Tommy Bahama restaurants and 35 Tommy Bahama outlet stores.

Oxford’s total annual revenue grew slowly from 2017 to 2019 — reaching a company high of $1.12 billion in 2019.

However, due to the COVID-19 pandemic, the company elected to close its brick-and-mortar locations in 2020, resulting in a 33.3% decline in total revenue in 2020.

Oxford is reopening its on-ground locations as the world looks past the pandemic.

This will bring customers back into stores to spend more money.

Projections are for Oxford to reach nearly $1.2 billion in total annual revenue by 2023 — an increase of 57% from 2020 lows.

In November 2020, Oxford’s stock price was around $40 per share.

In the eight months that followed, the stock jumped up 165% to over $100 per share.

It pared back some of those gains into October but has started showing signs of increased momentum in November after testing support at around the $85 level.

Oxford Industries’ Stock Rating

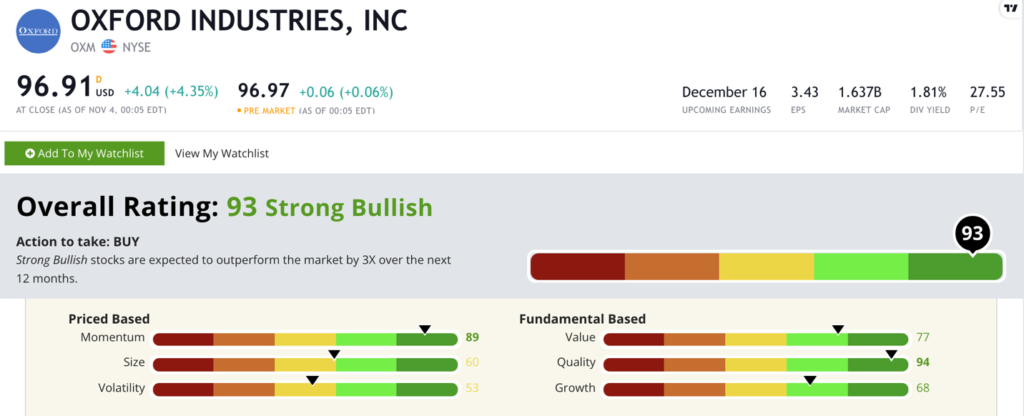

Using Adam’s six-factor Green Zone Ratings system, Oxford Industries scores a 93 overall. That means we are “Strong Bullish” on the stock and expect it to outperform the broader market by three times in the next 12 months.

Oxford Industries’ Green Zone Rating on Nov. 4, 2021.

Oxford Industries’ stock rates in the green in four of our six factors:

- Quality — The company has positive returns on assets, equity and investment. More importantly, it operates with a gross margin of 63.1% compared to the apparel and accessory industry average of 47%. Oxford earns a 94 on quality.

- Momentum — Oxford’s stock jumped 165% from November 2020 to June 2021 and, after paring back, is starting to regain its price strength — indicating it is in line with what Adam calls “maximum momentum.” The company scores an 89 on momentum.

- Value — Oxford trades with price-to-sales, price-to-book and price-to-earnings ratios that are on par with the rest of the industry. The company earns a 77 on value.

- Growth — The company has a prior quarter sales growth rate of 71.2% and prior quarter earnings per share growth rate of a whopping 929.7%! Oxford earns a 68 on growth.

The company earns a 60 on size, which is neutral, as it has a market cap of $1.64 billion.

Oxford scores a 53 on volatility, which is also neutral, but after testing some support at $85 per share, the stock is starting to inch closer to its 52-week high, suggesting it’s starting a run for “maximum momentum.”

Bottom line: The clothing industry took a serious hit due to the COVID-19 pandemic.

Sales suffered as brick-and-mortar stores closed to curb the spread of the virus.

But, as we return to normal, these stores are opening back up. Sales are projected to surpass pre-COVID highs in short order.

That’s why Oxford Industries Inc. is a clothing stock worth considering for your portfolio.

Safe trading,

Matt Clark, CMSA®

Research Analyst, Money & Markets

Matt Clark is the research analyst for Money & Markets. He is a certified Capital Markets & Securities Analyst with the Corporate Finance Institute and a contributor to Seeking Alpha. Prior to joining Money & Markets, he was a journalist and editor for 25 years, covering college sports, business and politics.