Stagflation.

It’s the last word you want to hear creeping into a conversation.

But with the Iran war threatening to push oil prices higher and growth lower, it may be exactly what’s ahead later this year. There are two ways you get inflation: from a “demand pull” or from a “supply push.”

Demand-pull inflation is relatively simple.

When the economy is running hot, perhaps due to interest rates being low or an excess of government stimulus, there’s more money sloshing around the system and more demand for goods and services.

This kind of inflation is easy enough to remedy. Raising interest rates or cutting government stimulus sucks excess demand out of the system.

If there were ever such a thing as “good inflation,” this would be it because prices are rising, but living standards aren’t necessarily falling.

On the other hand, supply-push inflation is another animal…

This is where prices rise not because people are flush with cash… but because shortages have suddenly made everything more expensive. This is the kind of inflation we had in the 1970s following the OPEC oil embargos.

We also experienced supply-push inflation during the pandemic as a result of port closures and supply-chain issues. This is inflation without growth… otherwise known as stagflation.

And with markets grappling with persistent geopolitical uncertainty, it could once again become our reality…The longer the war in Iran drags on, the more the potential for stagflation to take hold. Every extra dollar spent on higher gas or food prices is a dollar not available for other spending.

So, how can we protect ourselves from a stagflationary malaise?

To start, we should follow my system.

Long before the war started, my Green Zone Power Ratings system was flashing “Bullish” in energy stocks. As I wrote yesterday, energy stocks are the best-performing sector in 2026, and I see no signs they are slowing down.

Traditionally, real estate has also been a good inflation hedge.

And given how tight supplies are in most markets, real estate prices should be largely immune to a slowing economy. Apart from its role as an inflation hedge, real estate is among the industries best insulated from AI.

As I wrote back in February, the HALO trade – heavy assets, low obsolescence risk – is real and durable. You want assets that AI can’t turn upside down.

So, we’re going to do a sector X-ray of the real estate sector today.

Before I get started, I need to throw out a few caveats.

The accounting of real estate investment trusts (REITs) is “weird.”

Earnings tend to be artificially depressed by non-cash expenses, such as depreciation. This can impact their quality, value and growth factor ratings.

And because REITs also tend to hold a lot of debt, this affects their measure of balance sheet strength, which tends to depress their quality scores.

None of this is “good” or “bad.” It’s just a quirk of the industry we have to consider when analyzing real estate stocks.

With that said, let’s dig in.

A Peek Under the Hood

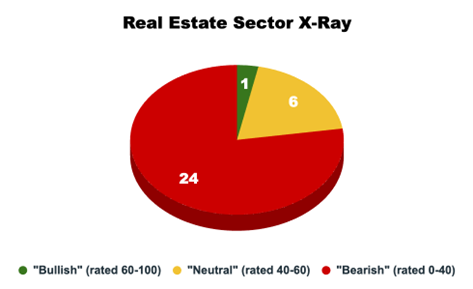

There’s a lot of red here…

Twenty-four out of 31 stocks are rated as “Bearish” on my Green Zone Power Ratings system. Six rate as “Neutral.” And only one rates as “Bullish.”

Again, we need to consider the context and understand that, generally speaking, REITs are going to rate fairly low relative to other companies due to their quirky accounting.

That’s exactly why we’re doing this X-ray. We’re going to dig into the factors that matter most for this sector…

Where Does Real Estate Pick Up Points?

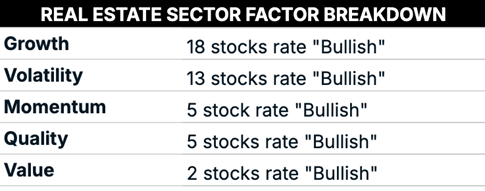

As a practical matter, we can discard the value and quality factor for REITs. I designed those factors for “normal” companies with standard accounting.

They don’t make sense for REITs, and no fundamental analyst would use a value subfactor like the price-to-earnings ratio or a quality subfactor like asset turnover to evaluate a REIT.

Let’s focus instead on growth, volatility and momentum. We want healthy real estate businesses with growing rents and not too many wild swings in the stock price. And naturally, we want to see them trending higher.

Well, 18 REITs rate as “Bullish” on growth, 13 rate as “Bullish” on volatility and five rate as “Bullish” on momentum.

Top-Rated Real Estate Stocks

With that backdrop in mind, let’s take a look at the highest-rated REITs today, paying special attention to those rated “Bullish” on momentum, volatility and growth.

The highest-rated REIT – and the only one with a “Bullish” overall Green Zone rating – is Host Hotels & Resorts (HST). I mentioned Host Hotels last month when it popped up as newly “Bullish.”

As I wrote then, Host Hotels is a classic HALO trade. AI can’t replace prized trophy assets like a Hawaiian Ritz-Carlton. And in an inflationary environment, I would expect trophy assets to more than hold their value.

Conservative retail REIT Realty Income (O) is the highest-rated real estate stock that rated “Bullish” on momentum, volatility and growth.

It owns a vast portfolio of high-traffic properties like convenience stores and pharmacies, and it pays a consistent monthly dividend. It’s as close to a bond as you’re going to find in the stock market.

At current prices, its dividend yields just under 5%, and the REIT has a long history of raising its payout each year.

Health care REIT Ventas (VTR) is also rated “Bullish” on all three factors. Ventas has a portfolio concentrated on the “longevity economy,” including investments in senior housing, medical offices and research centers.

It traditionally doesn’t pay a super high dividend (a little over 2% at current prices), but VTR shares have more than tripled since 2020.

And with America’s baby boomers continuing to age, Ventas should continue to enjoy growth in its key segments for decades to come.

To good profits,

Adam O’Dell

Editor, What My System Says Today