If you’re worried about inflation … well, I get it.

Anyone younger than 50 or so likely has no real memory of chronic, destabilizing inflation. You would have had to have lived through the disco era of the 1970s to have a frame of reference here.

Those days were marked by gas lines, soaring costs of food and basic necessities and a general sense of economic malaise.

I was born in the late ‘70s, and the really dated shag carpet that still adorned my house well into the mid-80s was a reminder of a period of U.S. history that I had no interest in experiencing firsthand.

To get a feel for what we might be in for in the coming months stateside, I want to see how Japan has dealt with a unique inflation situation for decades.

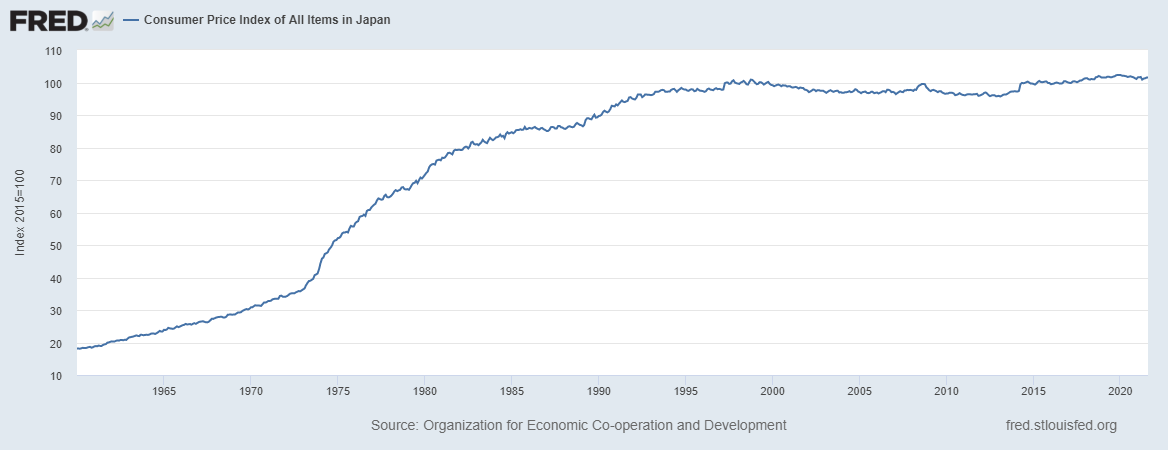

What We Can Learn From Japan’s Inflation Fight

Well, if Japan’s experience is any indication, we shouldn’t expect this little spate of inflation to stick around for very long.

Japan’s consumer price index came in at 101.5 in August. That wouldn’t be noteworthy except for the fact that the index was sitting at 100.9 in late 1998 and at 94.2 in August of 1991.

Prices in Japan are essentially unchanged in 23 years and have moved a whopping 7.3% over the past 30 years. That’s not 7% per year, mind you. It’s 7% … in total.

Bill Clinton was still the governor of Arkansas the last time inflation in Japan was significant.

Decades of Stagnant Inflation in Japan

Source: Federal Reserve.

And let’s be clear, Japan hasn’t been the model of fiscal or monetary discipline over that stretch. Japan hasn’t had a balanced budget since 1992. For most of the past 30 years, its budget deficits have been as large or larger than ours in the U.S. Japan ran a budget deficit of 12.3% of gross domestic product (GDP) last year. Its accumulated national debt is now 266% of GDP … about double the 132% if GDP that our government has borrowed.

Japan Has Tried It All

Zero interest rates? Japan’s interest rates have been zero or close to zero since 1999. Japan also invented “quantitative easing.” The term was coined to describe Japan’s aggressive bond buying in the late 1990s and early 2000s.

Zero interest rates? Japan’s interest rates have been zero or close to zero since 1999. Japan also invented “quantitative easing.” The term was coined to describe Japan’s aggressive bond buying in the late 1990s and early 2000s.

We were all aghast when the Federal Reserve ballooned its balance sheet following the pandemic. But even after gobbling up trillions in U.S. government debt, the Fed’s balance sheet is “only” a little over 40% the size of the U.S economy. The Bank of Japan’s holdings of Japanese government debt is now close to 100% of the size of its economy.

And it’s not just government bonds. The Bank of Japan is now the largest single shareholder of Japanese stocks and owns massive holdings of real estate via real estate investment trusts (REITs) as well.

Japan hasn’t taken Ben Bernanke’s old advice to dump yen out of helicopter… yet. But that’s just about the only thing the country hasn’t done. And it still can’t sustain inflation. The country continues to struggle with deflation instead.

The U.S. isn’t Japan, and we shouldn’t assume that we’ll follow the exact same path. But this does suggest that maybe — just maybe — today’s inflation is transitory. Once the post-COVID supply chain mess gets worked out we may have to deal with falling prices instead.

To safe profits,

Charles Sizemore

Co-Editor, Green Zone Fortunes

Charles Sizemore is the co-editor of Green Zone Fortunes and specializes in income and retirement topics. He is also a frequent guest on CNBC, Bloomberg and Fox Business.

P.S. Live on November 4, Adam O’Dell will reveal how millions of new investors have accidentally opened a perfect trading window, and the system he designed to exploit this anomaly for massive gains. To sign up for the live event, go here.