When we think about artificial intelligence (AI), we think robots, computers, smart devices … maybe even Amazon’s Alexa or Apple’s Siri.

What we don’t think about is hamburgers. And yet, McDonald’s Corporation (NYSE: MCD) just dolled out a reported $300 million for decision-logic firm Dynamic Yield Ltd.

“Technology is a critical element of our velocity growth plan,” McDonald’s CEO Steve Easterbrook said in a statement following the announcement.

Indeed, McDonald’s already has begun to revamp its restaurants with an “Experience of the Future (EOTF) remodels and digital ordering via smartphone and kiosk,” says Andrew Charles at Cowen & Co.

It’s an ingenious plan. McDonald’s is already rolling out it’s in-store kiosks to speed up ordering and cut down on labor costs.

With the acquisition of Dynamic Yield, the fast-food giant can now better suggest meals appropriate to your personal tastes, including add-on items, and adjust those offerings to the local weather. For instance, offering ice cream or shake options on a hot summer or more coffee options during colder days.

The potential for loyalty program growth also is astounding. With Dynamic Yield’s technology, McDonald’s could have even greater control on just what coupons and special offers are made directly to you, based on your ordering habits and preferences.

By being better able to adapt to personal tastes and local conditions, McDonald’s stands to provide not only better service, but also higher ticket margins on orders.

In short, by investing in technology, McDonald’s is laying the groundwork for higher returns and revenue down the road.

And, with its deep pockets, $300 million is a blip in McDonald’s total market capitalization of $143.26 billion. So investors worrying about the cost of the deal have nothing to fear.

For the time being, McDonald’s is expected to see earnings rise 7.2 percent for the current quarter, and 5.5 percent for fiscal 2019. Revenue growth isn’t as impressive, with the current quarter sales expected to decline 4 percent to $4.93 billion, and full-year growth nearly flat at $20.9 billion.

However, McDonald’s spending on restaurant revamps and EOTF rollouts are the likely culprits for the shortfalls. Value investors should not shy away from this kind of spending on the company’s future, especially in a market where stock buybacks are the norm.

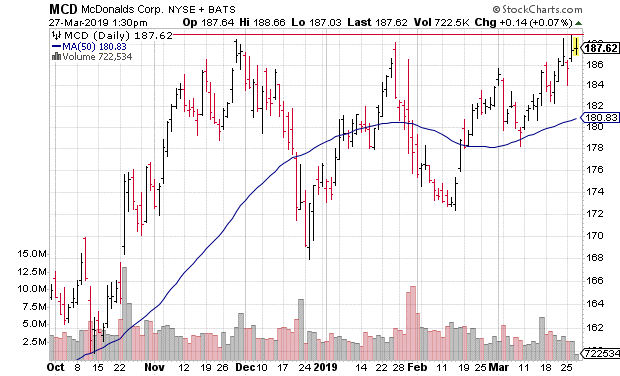

MCD’s price action shows that most investors have a positive outlook for the company. The shares are up more than 6 percent year-to-date, and up more than 20 percent in the past 12 months.

But while long-term growth is solid for McDonald’s, the short-term outlook for the stock is in question.

Right now, MCD shares are battling price resistance near $190. This is the third time since November that MCD has encountered resistance in this area, indicating it could be a significant hurdle. This is especially true given U.S. economic growth concerns and the increased market volatility.

The bottom line is that there are plenty of reasons to be excited about McDonald’s growth in the extremely lucrative AI field. The long-term growth prospects are more than enticing. However, given MCD’s current technical outlook, there are sure to be better entry prices down the road.

Keep scrolling to read more investment tips from Thomas Lancaster on Money & Markets.