Wall Street has always cared about earnings surprises — but this quarter, the stakes got noticeably higher.

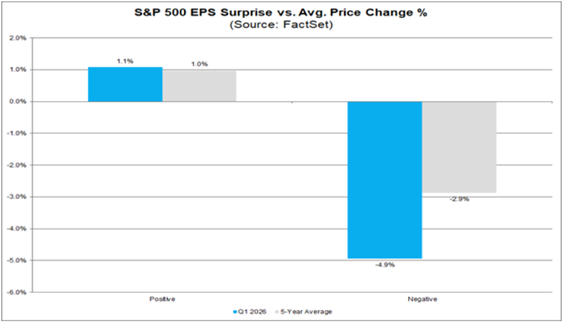

According to fresh data from FactSet, S&P 500 Index companies that missed earnings estimates in first-quarter 2026 saw their stock prices fall an average of 4.9% in the days surrounding their reports.

That’s a dramatic jump from the five-year historical average punishment of just 2.9% for a miss. In other words, the market is now penalizing earnings disappointments nearly 70% more harshly than it has over the past five years.

On the flip side, companies that beat expectations were rewarded with a modest 1.1% average price gain — barely a tick above the five-year average of 1.0%.

So while beating estimates still earns you a pat on the back, the real story this season is how unforgiving investors have become when companies fall short.

What’s driving this asymmetry? It likely reflects a broader shift in market sentiment.

After years of relatively easy comparisons and low-bar expectations, investors are holding companies to a higher standard.

With interest rates remaining elevated and economic uncertainty clouding the markets, there’s less patience for execution stumbles. The market appears to be pricing in a “prove it” mentality — rewards for beating are modest, but the penalty for missing is steep.

For investors, this data carries a clear message: the risk/reward of holding individual stocks through earnings has become more lopsided.

The upside of a positive surprise is roughly the same as it’s always been, but the downside of a miss has grown considerably.

This is a good time to review your positions heading into earnings announcements, consider whether your portfolio has outsized exposure to companies with uncertain outlooks and carefully think through position sizing during report season.

Now, with earnings season ramping up next week, let’s break down which calls have us feeling bullish — and which ones have us watching carefully.

“Bullish” Earnings to Watch

These stocks are expected to beat their earnings per share (EPS) from the previous quarter. And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are six companies that made this week’s list:

Keysight Technologies Inc. (KEYS) is the one that stands out the most to me.

Analysts are projecting a 43% quarter-over-quarter (QOQ) increase in the company’s EPS.

But I believe it could beat that estimate…

Keysight makes the electronic test and measurement equipment that engineers use to design and validate semiconductors, 5G networks, electric vehicles and defense systems.

That puts the company at the intersection of several long-cycle spending trends that have been accelerating.

As chip design complexity grows and 5G infrastructure buildout continues globally, demand for Keysight’s testing tools tends to be both resilient and sticky — customers don’t easily switch vendors mid-project.

Additionally, Keysight has a strong software and services revenue mix that provides recurring income and typically carries higher margins than hardware. If that segment continues to grow, it could provide a nice earnings cushion, pushing results past analyst estimates.

A beat for KEYS will certainly help its already “bullish” rating on Adam’s Green Zone Power Ratings system.

Now, let’s look at potentially “bearish” earnings for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a QOQ decline in earnings.

Here are four companies that passed this screen:

Target Corp. (TGT) is probably the easiest one to understand just from living life.

Walk into any Target right now, and you can kind of feel the story — shoppers are being more careful with their money, and Target sits in an awkward spot.

It’s not quite the “cheap” option like Walmart (WMT), but it’s also not a specialty retailer with a devoted niche. That middle ground has been a tough place to be lately.

The EPS estimate drops from $2.30 last quarter down to $1.42 — that’s a pretty notable step down.

And with tariffs making a chunk of Target’s imported goods more expensive to stock, margins could get squeezed further. They either eat the cost or pass it to shoppers who are already pulling back. Neither option is great.

There’s also a lot of competition breathing down the company’s neck right now. Amazon (AMZN) keeps improving its fast delivery, and Walmart has been winning over budget-conscious consumers in a big way.

Could Target still beat the $1.42 estimate? Sure, anything’s possible. But the headwinds are real and very visible, which is probably exactly why it made this list.

Should be another fun week of earnings.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets

P.S. Inflation may be cooling in the headlines, but for most Americans, everyday costs still feel stubbornly high — and that’s forcing a lot of investors to rethink what they actually need from the market.

Instead of focusing purely on long-term gains, What My System Says Today editor Adam O’Dell spent the last year developing a more cash-flow-oriented approach built around simple “deals” designed to create consistent income opportunities in virtually any market environment.

And he’s going LIVE on May 19 at 1 p.m. ET to demonstrate exactly how this process works in real time, including how these deals are identified, structured and managed from start to finish.