Yesterday, I told you about a small cybersecurity company to avoid.

Today, I’m thinking bigger. I have a massive cybersecurity company you want to stay away from.

As I mentioned before, cybersecurity is big business. Companies spent 24% of their IT budgets guarding against threats in 2022.

While cybersecurity has been one of the hottest tech sectors to trade, trends indicate that growth is slowing.

The reason: Recession concerns and higher interest rates are forcing businesses to spend less.

Cybersecurity remains a long-term growth industry as we become more reliant on tech and need stronger ways to protect our data. But growth will slow with a weaker economy.

Cybersecurity stocks are taking a massive hit.

This is the case with Palo Alto Networks Inc. (Nasdaq: PANW).

Sales Grew, but Palo Alto Networks Stock Didn’t

PANW’s business is simple: It utilizes internal cyber threat analysis to provide businesses with the products they need to thwart risks.

It’s based in the heart of Silicon Valley … Santa Clara, California.

Palo Alto Networks is making money, sure. But its biggest issue is that it isn’t turning a profit. More money is flowing out than in.

And it’s created a stock that’s not worth investing in right now.

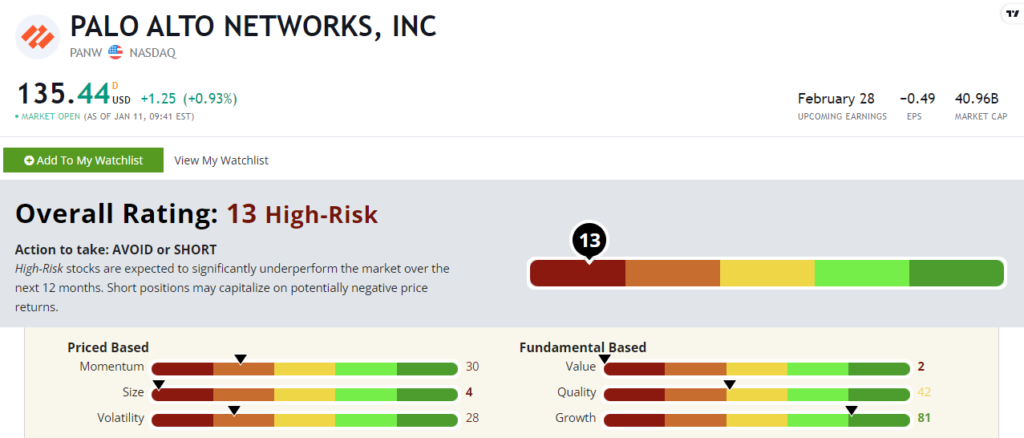

PANW’s Stock Power Ratings in January 2023.

PANW stock scores a “High-Risk” 13 out of 100 on our Stock Power Ratings system. We expect it to underperform the broader market over the next 12 months.

PANW Stock: Abysmal Value + Weak Momentum

Looking at Palo Alto Networks’ financials tells the story of a tech stock that got caught up in the incredible bull market that ended last year:

- Of its $1.5 billion in sales reported in its most recent quarter, the company managed just $20 million in net income!

- PANW increased its spending on research and development, sales and marketing in the last quarter … accounting for its weak net income.

While PANW scores in the green on our growth factor (81), it slumps on value (2).

Its price-to-earnings ratio is negative. That’s proof that the company isn’t making money.

What’s more, its price-to-sales ratio is nearly six times higher than the industry average.

Even more glaring … PANW’s price-to-cash flow ratio is 18 times higher than its communication equipment peer average … earning it a 2 on our value factor.

So, PANW is growing its revenue, but its value is horrendous … especially compared to its peers.

Investors bid the stock’s price up in hopes for future returns. But now it’s coming back down to Earth.

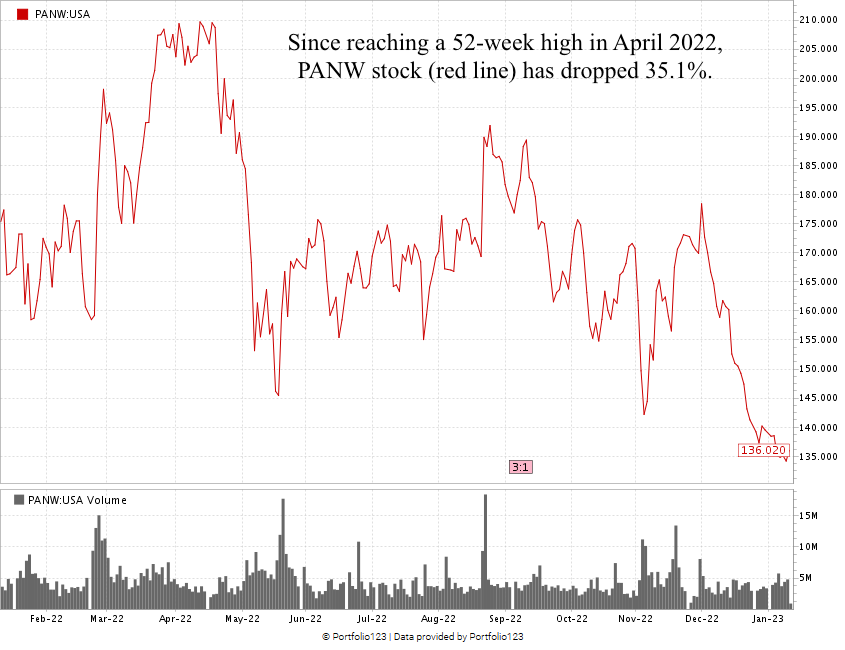

Another telltale sign to avoid the stock is its recent momentum (or lack thereof) … Palo Alto Networks stock fell 25% since last month:

Created in January 2023.

From its 2020 pandemic low to its 52-week high in April 2022, PANW rocketed 374.5% higher.

Since reaching that high, the stock has nosedived 35.1% to a 52-week low.

PANW stock scores a horrendous 13 overall on our proprietary Stock Power Ratings system.

That means we consider it “High-Risk” and expect it to underperform the broader market.

Bottom line: Cybersecurity is a long-term growth industry. We will need more ways to protect our digital data as we rely more on tech every day.

Investors, however, can’t ignore the short-term implications of increased recession pressures.

Sluggish profits and outrageously high valuations mean PANW is a stock you should stay away from.

Note: Mike Carr is about to show you his newest strategy to profit during the “Silicon Shakeout.”

Tech stocks struggled during 2022, and Mike sees more losses on the horizon. But that’s the perfect environment for his trades that he believes have the opportunity to gain 442%, 564% and even 824% before the summer!

Click here to sign up for his free presentation later today.

Stay Tuned: A Promising Wind Energy Stock

Tomorrow, we’re returning to our original Stock Power Daily form.

Stay tuned — I’ll share all the details on a renewable energy stock that’s capitalizing on the global growth of the offshore wind energy market.

Safe trading,

Matt Clark, CMSA®

Research Analyst, Money & Markets

P.S. I’d love to hear what you thought about my “Stock to Avoid” article today. Was it valuable? Would you like us to continue sharing high-risk stocks on occasion, so you know what to stay away from?

Would you prefer that we only share “Bullish” and “Strong Bullish” stocks?