I’ll go out on a limb and assume you’ve seen, or at least heard of, It’s a Wonderful Life. It was basically required viewing for any American kid who grew up in the last 70 years. The film resonates whether you celebrate Christmas… Have ever felt the pressures of everyday life mounting… Or if your savings are stored at a small regional bank and are worried if they’re safe.

In the film, lead character George Bailey goes through the ringer a few times as the owner of the local Building & Loan. One particularly bad episode has half the town knocking at his door to withdraw their savings, after rumors spread about the bank’s solvency.

George, of course, doesn’t have their money. Like virtually every banker, he’s lent it out to generate a return that helps him stay in business. Through charm and quick thinking, he’s able to rally them into accepting a just the savings they immediately need now, lest they risk losing it all for good.

It’s a Wonderful Life never claimed to be a grounded, realistic film. It’s an inspiring piece about the value of community and reflecting on the impact you make on it.

But if there’s one idea you should not take form it, it’s that the regional bank around the corner will take drastic, self-sacrificing measures to protect your savings.

In fact, if you do business at such a place, you may soon find yourself as one of the distressed crowd huddled outside the branch. Only for you, there’s no George Bailey waiting to open the doors and compromise.

Regional banks are in serious trouble right now. And the reasons why go all the way back to March 2020, a period of time we’re still very much feeling the impacts of.

Today, I want to shed some light on the troubles facing the regional banking industry. More than that, I want to share my plan to prepare my readers for what I believe is coming… and share a way to profit as this trend plays out.

Empty Offices Make Empty Coffers for Regional Banks

Right now, commercial real estate owners are facing the headache of their lives. And even that is nothing compared to what their lenders face.

The shutdowns in March 2020, in response to the worsening COVID pandemic, emptied out office space across the United States. Office-space leasers had to suck it up and pay their bills throughout the remote-first shift. But now, with COVID mostly in the rear view, remote work has become much more the norm than it ever was before.

Soon, office leases are set to expire. Many business owners can’t wait to get out of them, or at least downsize to a more appropriate space. Suffice to say, CRE owners will struggle to find new tenants… and afford their loan payments.

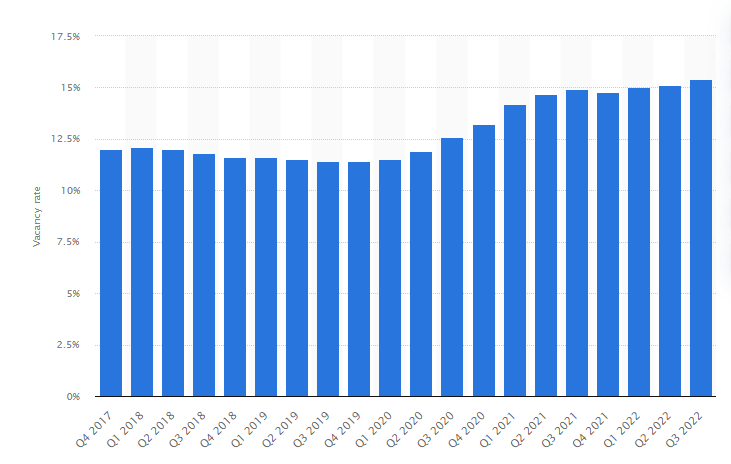

This chart from Statista sums up the issue. It shows that U.S. office vacancy rates are a) over 15%, the highest rate in over five years b) higher than they were at the peak of pandemic shutdowns and c) rising.

U.S. Office Vacancy Rates

Source: Statista

This has naturally weighed on the value of commercial property. The average price per square foot of Manhattan commercial property, for example – one of the hardest-hit regions of this trend – is down 22.4% over the last year, and at its lowest level since 2012.

Amid all this is the steepest rise in interest rates since the 1980s, which has had a cascading effect on outstanding CRE loans – $1 trillion worth of them are up for refinancing over the next few years.

What does this have to do with regional banks? Too much.

A report from JPMorgan shows that small regional banks hold 4.4 times more exposure to U.S. commercial real estate loans than their larger peers. And a recent Citigroup analysis found that small-size lenders hold 70% of CRE loans.

Commercial real estate isn’t the sole focus of these banks, either. Many of them have individual banking services that everyday people use.

These banks will face liquidity problems as these CRE loans come due for refinancing. They may need to take possession of commercial property and have a tough time offloading it. That could impact their ability to meet withdrawals. And depositors are already sweating.

Right after Silicon Valley Banks’ problems were exposed in March, some $119 billion of midsize bank deposits were withdrawn for safer alternatives. These kneejerk reactions may prove to be correct in the long run.

If you find yourself in a position where you have money in a small or midsize regional bank, your greatest strength is in knowledge. Look up the bank and see how exposed it is to commercial real estate. If it’s an uncomfortable level, the simplest thing to do is consider moving your savings to a bigger bank. Large banks don’t hold anywhere near the level of risks that the smaller banks do right now.

Then, once your money is safe, I have another idea…

Profit on the Regional Bank Crisis

John F. Kennedy popularized the idea that the Chinese word for “crisis” is made up of two characters: one meaning “danger” and the other meaning “opportunity.”

Linguists contest the accuracy of this, but the point stands. Often, dangerous situations can spell lucrative opportunities for shrewd investors.

Right now is one of those times.

Recently, in my options trading advisory Max Profit Alert, I recommended a put option trade that took direct advantage of the stresses in regional banking. Within just three weeks, we locked in a 75% profit on a third of the position.

As the crisis accelerates, I expect that to translate into even bigger gains for my subscribers.

Max Profit Alert is not currently open to new subscribers. But, in the coming weeks, I do plan on releasing new research on specific regional banks that I believe hold substantial risk and could provide interesting short trade opportunities.

To learn how you can get access to that research, stay tuned to Stock Power Daily. We’re looking to put it out in the coming weeks.

In the meantime, just keep a close eye on the commercial real estate slowdown and regional banking crisis. Taking steps now to ensure it won’t impact your wealth will help put you in position to profit immensely down the line.

To good profits,

Adam O’Dell

Chief Investment Strategist, Money & Markets