If there’s one positive that has come out of the whole coronavirus ordeal, it’s that I’ve had a chance to look at my own expenses and how they are hurting or helping my retirement goals.

I’m still a long way off from exiting the workforce, and my retirement plan has a few kinks that need to be smoothed out. The lockdown has me thinking long and hard about ways I can modify my own spending so my retirement goals can become a reality.

This has probably happened for a lot of folks that have been stuck at home: You’re not going out as much and you’re noticing the numbers in your bank account slowly ticking up — or at least not going down as much as when you were going out a lot more.

It’s a nice thing to see, and it’s opened my eyes to some changes I can start making so I can meet my retirement goals.

Now I’m not advising everyone to become a miser and sock away every penny you earn, but this situation has helped me realize where I can cut back a bit and put those dollars to work toward my future.

Being mindful of your spending can create major saving opportunities for your retirement goals.

Let’s look at one spending category that we could all probably work on: eating out. The average American household spent $3,459 a year at restaurants in 2018, according to the Bureau of Labor Statistics. Surely there’s room to cut some of the fat off that yearly expense.

Once again, I am not calling for everyone to completely cut themselves off from their favorite local burger joint or coffee runs to Starbucks. But being mindful of what you are spending every time you go out to eat can be a powerful tool.

How Trimming Expenses Can Help You Meet Your Retirement Goals

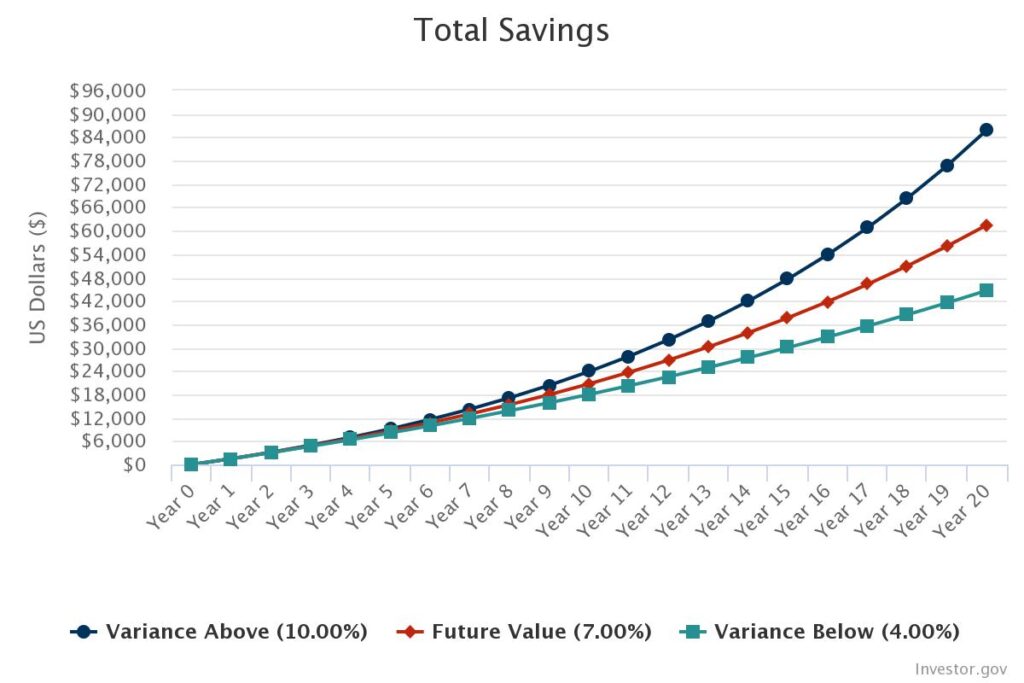

Let’s say you cut that total down to just under $2,000 and decide to reinvest that extra $1,500 a year into an S&P 500 index fund. Since 1920, the S&P 500 has averaged around 7% returns when adjusted for inflation, so we’ll use that as a baseline for some quick math.

By saving an average of $125 per month ($1,500 divided by 12) and putting it into an index fund that tracks the S&P 500, you’re looking at around $61,493 saved in 20 years. That’s huge!

If you didn’t touch that $1,500 per year, you’d still have an extra $30,000 by the end of two decades. But compounding interest almost doubles your savings, and that’s a beautiful thing to see.

That’s just one example of how analyzing your spending now can help you achieve your retirement goals later. If you start looking at other areas that can be trimmed down, all of a sudden you have a nice chunk of change that could be reinvested in a smarter way to fund your future.

So how can you do this?

Creating a budget and sticking to it is the first thing I would try to do. By creating a budget that is tailored to you, it’s possible to meet your retirement goals while still having funds for things you enjoy.

Get down to the nitty-gritty and really examine what you are spending your money on. Tracking your spending can be eye-opening — and incredibly beneficial.

And remember budgets can be flexible. My wife and I have been focused on our budget for almost two years now, and it’s gone through so many iterations as we’ve figured out areas where we want to save or spend more.

The point is budgeting doesn’t have to feel like you’re in prison and locked into a system that can’t be changed — make your budget work for you.

Thinking about your expenses now can make hitting your retirement goals a reality.