In 1996, President Bill Clinton famously said: “The era of Big Government is over.”

Since then, we’ve had two Republican presidents along with two Democratic presidents, and the size and scope of the government never stopped growing … regardless of who was running the show.

Now, I’m not a fan of sprawling government. But at this point, it’s inevitable. We can at least identify the relevant trends and profit from them.

Big Government, Big Real Estate

Ever-expanding government means growth in the metro Washington and Baltimore area. The larger the government, the more people you need to manage the bureaucracy. But this also means more demand for everything from dry cleaning to grocery stores.

And that brings me to Saul Centers Inc. (NYSE: BFS).

Saul is a real estate investment trust (REIT) based in Bethesda, Maryland. It owns and manages a portfolio of 61 properties, 50 of which are community and neighborhood shopping centers. The rest of the portfolio consists of mixed-use properties and a handful of land and development properties.

Here’s the kicker: 85% of Saul Centers’ rental income is generated by properties in the metro Washington and Baltimore area.

If you believe the government only gets bigger from here, then BFS is a good way to play that growth.

Saul also has the benefit of being a smaller, mostly under-the-radar REIT. Most investors have never heard of BFS.

Yield isn’t particularly easy to find these days, but Saul yields a respectable 4.2%. And the REIT has raised its payout nearly every year since 2014.

Saul Centers Is Bullish for the Future

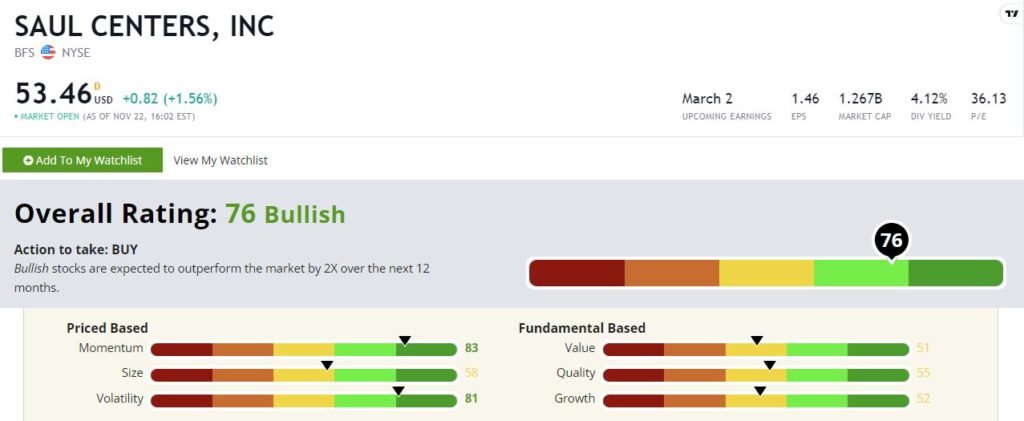

Saul Centers rates a competitive 76 on our Green Zone Ratings system, putting it well within “Bullish” territory. (Anything over a 60 is considered Bullish or Strong Bullish.)

Saul Centers Inc.’s Green Zone Rating on November 23, 2021.

That’s a great score for a REIT! These assets get punished in our system due to quirky accounting that creates artificially low earnings data.

Let’s dig into the details.

Momentum — Saul Centers rates highest on our momentum factor at 83. Many REITs are enjoying a post-COVID recovery, and Saul is no exception. It lost more than half its value in the early stages of the pandemic. While shares have now more than doubled since October of last year, they’re only now returning to pre-pandemic levels. Saul’s high momentum should have further to run.

Volatility — BFS also rates well on our volatility factor with a score of 81. This makes sense. Disruptions of the pandemic notwithstanding, shopping centers are boring, conservative businesses. They collect rent from Main Street tenants, rinse and repeat each month. That’s an attractive quality in a dividend stock.

Size — Saul Centers isn’t a large REIT. Its market cap is about $1.3 billion. This is a stock that most investors haven’t heard of, which is good for us. An undiscovered stock is less likely to be overvalued. Saul rates a 58 on our size score.

Quality — Saul Centers rates a 55 on quality. REITs get punished here due to quirky accounting. Our quality score is based on profitability and balance sheet stretch. REITs tend to have low reported earnings due to depreciation and high debt levels due to financing of their properties. All things considered, a 55 quality rating is good for a REIT.

Growth — Saul isn’t a growth dynamo by any stretch, but its growth rating of 52 puts it in line with average market performance. That’s not bad for a conservative REIT in an otherwise aggressive, growth-obsessed market.

Value — As with quality, REITs get punished on our value score. But all the same, Saul rates a 51 here.

Bottom line: Are you going to get rich in Saul Centers? Probably not.

But would BFS make for a nice addition to a gritty, workhorse dividend portfolio? You bet it would.

To safe profits,

Charles Sizemore

Co-Editor, Green Zone Fortunes

Charles Sizemore is the co-editor of Green Zone Fortunes and specializes in income and retirement topics. He is also a frequent guest on CNBC, Bloomberg and Fox Business.