Hands up if you’ve heard of the Strategy Shares Nasdaq 7Handl Index ETF (Nasdaq: HNDL).

Right. I thought not. And I can’t blame you for overlooking this one. It’s a relatively obscure ETF, with a bit over $700 million invested across a number of assets (just what those assets are I’ll get to in a minute).

Nonetheless, HNDL is worth discussing today because it highlights a couple things we need to look out for when picking high-yield funds for our portfolios.

First up, the yield and the strategy: HNDL pays a 6.9% dividend today and promises diversification, both of which sound great. A dividend that big will get you a lot of income on a relatively small investment, and diversification holds the promise of lower volatility.

In the case of the best high-yield funds, it works out great: If the managers can get a 7% total return, net of fees from the assets their fund holds, they can pass that return over to you. That, in turn, lets investors do seemingly impossible things, like retire on $500,000 or less, on dividends alone.

In some cases, though, this doesn’t work out so great. For instance, you wouldn’t want to invest in a fund that underperforms the market so much that you end up with $30,700 in profits over three years instead of the $65,200 you’d have gotten from a low-yielding index fund like the SPDR S&P 500 ETF Trust (NYSE: SPY).

This is the first problem with HNDL.

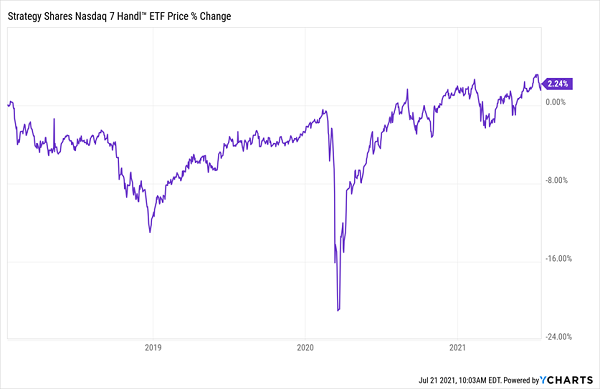

HNDL Underperforms, Even With Its High Dividend …

With a total return half that of the S&P 500, HNDL is not only underperforming the market, it’s barely earning enough to maintain its dividend, which is why its market price is up just 2.2% in the same time period.

… While Its Price Goes Nowhere Fast?

This isn’t too big of a deal if you just want dividends, but note how the fund’s price fell dramatically in the March 2020 crash. Luckily that was a short-lived calamity (at least as far as the stock market was concerned), so HNDL was able to maintain its payout without being forced to sell too many of its assets to do so.

But what about the next time? A long-term crash could mean HNDL is forced to sell to keep its payouts going, resulting in a smaller fund, a lower market price and real losses for investors despite the income.

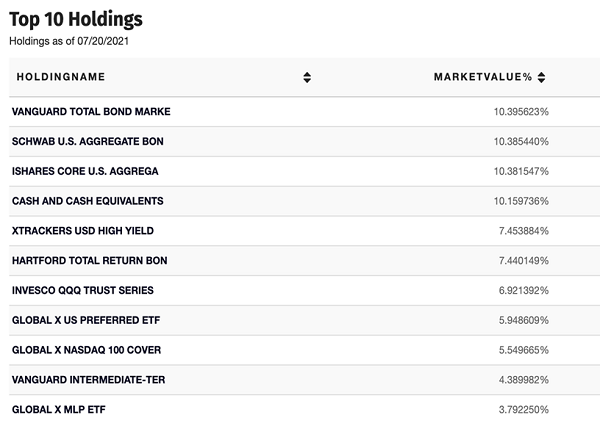

Source: Strategy Shares.

HNDL’s susceptibility to a crash isn’t the only concern here. As you can see above, the fund’s entire portfolio consists of 19 other ETFs. That’s a portfolio anyone could assemble pretty easily without paying HNDL’s fee of 1.62% of assets.

Too Aggressive and Too Conservative at the Same Time

The fact that HNDL’s constituent assets all charge fees is a problem; for instance, the Global X MLP ETF (NYSE: MLPA) charges 0.46% fees, has lost money since its inception and underperformed other ETFs holding master limited partnerships (MLPs, a type of company that mainly owns pipelines and oil and gas storage facilities), such as the more established Alerian MLP ETF (NYSE: AMLP).

When HNDL doesn’t go for more aggressive ETFs like those two, it errs (too far) on the side of caution. For example, it invests in the Vanguard Total Bond Market ETF (Nasdaq: BND) and the Schwab U.S. Aggregate Bond ETF (NYSE: SCHZ), neither of which has earned a profit in 2021.

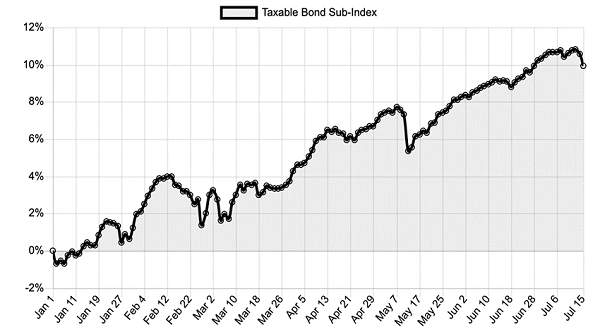

Bond ETFs Struggling

Meantime, the average bond CEF is performing much better, according to my CEF Insider service’s taxable-bond sub-index.

Bond CEFs Are on a Tear

Source: CEF Insider.

If HNDL had chosen better assets, it could be a compelling option for investors looking for a high income stream. As it stands, though, this collection of funds is too expensive and isn’t delivering the returns necessary to justify HNDL’s fees.

To learn more about generating monthly dividends as high as 8%, click here.