Welcome to another earnings Friday at What My System Says Today.

Before I get into “bullish” and “bearish” earnings, I want to start with revenue.

Every company aims to grow its revenue every quarter and every year.

It doesn’t always work out that way, but the goal remains the same.

Revenue growth is important because it indicates market demand, ensures financial stability and drives long-term shareholder value.

It also gives companies the capital needed to expand, innovate and hire more personnel.

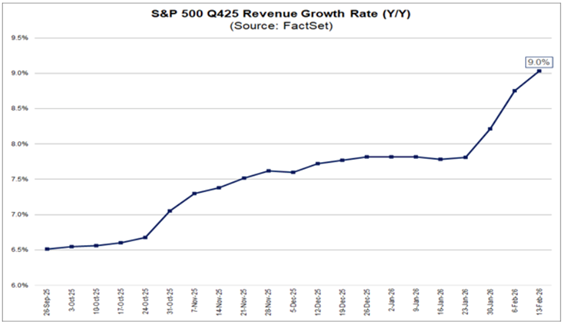

Members of the S&P 500 Index have done an admirable job expanding their revenue over the past several months:

In September 2025, the revenue growth rate for S&P 500 companies was just 6.5%. Today, that growth rate stands at 9%.

According to FactSet, if that growth rate holds, it will be the highest figure reported by the index since it hit 11% in the third quarter of 2022.

At the sector level, information technology, health care, communication services and industrials have been the largest contributors to the expanded growth rate since the start of the year.

Companies like Apple Inc. (AAPL), Super Micro Computer (SMCI) and Microsoft Corp. (MSFT) have seen their revenue grow exponentially so far in 2026.

While this is good news for these sectors and their investors, projections call for revenue growth rates to begin falling to 8.7% in the first quarter of 2026 and to 7.3% by the third quarter of 2026.

While that’s still strong, it’s not nearly as impressive as 9%.

Now, let’s examine potentially “bullish” earnings for next week…

“Bullish” Earnings to Watch

These stocks are expected to beat their previous quarter’s earnings per share (EPS). And if those expectations are met or exceeded, they could potentially trade higher.

For this screen, stocks must meet four criteria:

- 10 or more analysts cover the stock.

- The average analyst recommendation is a “Buy.”

- It BEAT analysts’ EPS estimates for the previous quarter.

- The average analyst estimate for the current quarter’s EPS is greater than the previous one.

Here are eight companies that made this week’s list:

While there are many retailers on this list, I want to focus on The Kroger Co. (KR).

The Cincinnati, Ohio-based grocery chain has struggled over the past few quarters on both sales and earnings.

Last quarter, Kroger reported EPS of -$2.02 on revenue of nearly $34 million. It was the fifth consecutive earnings beat, but marked the fifth straight revenue miss.

However, the chain has shifted its focus to higher-margin e-commerce and has implemented cost-management systems to trim expenses.

If it hits analysts’ estimates (and I believe it will), it will not only be a significant improvement over the previous quarter, but also a nice year-over-year increase of 42.8%.

With consumer spending holding steady (or slightly rising, depending on the data you are looking at), Kroger should top estimates and even surpass them this quarter.

Plus, another earnings beat would go far to lift KR out of the “High-Risk” zone of Adam’s Green Zone Power Ratings system.

Now, let’s look at potentially “bearish” earnings for next week…

“Bearish” Earnings to Watch

For our “bearish” earnings screen, we’re only looking for two things:

- 10 or more analysts must cover the stock.

- The average analyst estimate for the current quarter’s EPS is less than the previous quarter’s.

We want companies that are covered by a sufficiently large group of Wall Street analysts who collectively expect the company to report a quarter-over-quarter earnings decline.

And since we are nearing the end of the earnings season, I expanded this screen to include companies not listed on the S&P 500.

Here are 10 companies that passed this screen:

AutoZone Inc. (AZO) posted its lowest EPS in the last three years, at just $22 in Q2 2022.

Looking at the company’s earnings, it’s important to note that its fourth-quarter earnings are traditionally its best.

The bad news is, it reports its second-quarter 2026 earnings next week – traditionally its weakest earnings quarter.

So, history shows this projected decline in earnings is par for the course.

Another important thing to note is that AZO has missed EPS estimates in each of the last five quarters and revenue in four of the last five.

I believe AutoZone will miss earnings and come in below analysts’ expectations once again.

That puts it in danger of falling further down the line on Adam’s Green Zone Power Ratings system.

Either way, despite the season winding down, next week’s earnings promise to be interesting.

That’s all from me today.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets