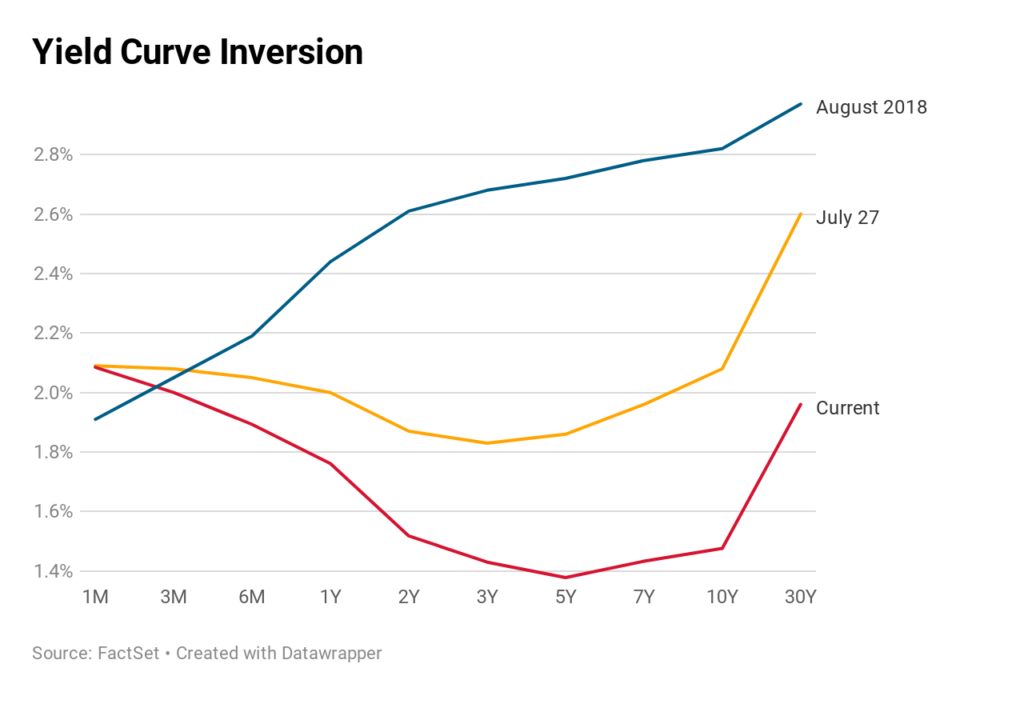

Long-term Treasury yields continued to struggle Tuesday, with the key curve between the 2-year and 10-year yields inverting once again to levels not seen since 2007, the last time it also ended the trading day inverted.

the bond market just closed with inverted yield curve for Treasuries – a key indicator of looming recession – for the first time since 2007

— John Harwood (@JohnJHarwood) August 26, 2019

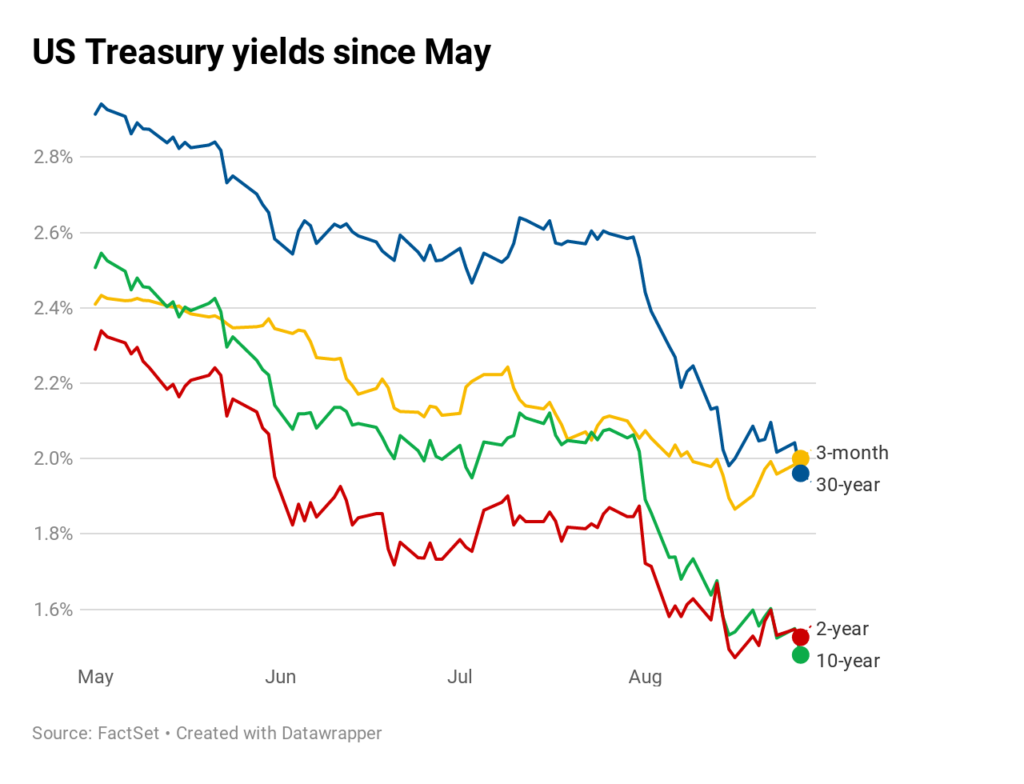

The yield on the benchmark 2-year Treasury note fell to 1.526% Tuesday, while the 10-year note was at 1.479%. When the long-term yield falls below a short-term yield it’s compared to, it’s known as an “inverted yield curve,” and the last time the 2/10 inverted like this was in December 2005, two years before the Great Recession, according to CNBC.

The 2-and-10 inversion has a good track record, too. Every recession over the last 50 years has been preceded by this particular yield curve inversion, according to Credit Suisse. Timing that recession is tricky, though, and it typically takes an average of 22 months to reveal itself.

But the fact that the 2-year/10-year keep inverting is only helping the case.

The worsening inversion is “certainly validating that a recession has a great chance of being here a year, year and a half from now,” Kevin Giddis, head of fixed income capital markets at Raymond James, told CNBC.

That isn’t the only curve inverting, either. The Fed’s inversion of choice is the comparison between the 3-month Treasury yield and the 10-year, which slumped to -50 basis points, its lowest level since March 2007.

The 30-year bond yield was sitting at 1.961% Tuesday, on track to finish below the 3-month yield as well. With the 30-year yield at such a low point, investors were actually earning more from stock dividends than from the long-term bond. It was the first time that had happened since March 2009, when the world was in the middle of recession, according to Bespoke Investment Group.

“The outlook is much better for stocks than it is for long-term Treasurys right now,” Bespoke co-founder Paul Hickey told CNBC on Tuesday. “For an investor looking to hold something for the long term, it makes equities relatively attractive.”