It’s Thursday, and you know what that means. I’ll be reporting on stocks that have officially crossed the threshold into “Bullish” territory this week, meaning their Green Zone Power Rating is 60 or higher.

My research has found that “Bullish” rated stocks outperform the market by double on average over the following year. But that’s not the only information I’m looking to glean.

I also monitor this list to look for changes in trend.

If several stocks in a given sector are trending “Bullish,” that suggests we should probably dig into that sector for potential investments. And if there is a distinct dearth of “Bullish” rated stocks in a sector… Well, that’s good to know, too!

It’s an eclectic collection this week, covering everything from yoga pants to West Texas wilderness and everything in between.

So, with no further ado, let’s jump into it.

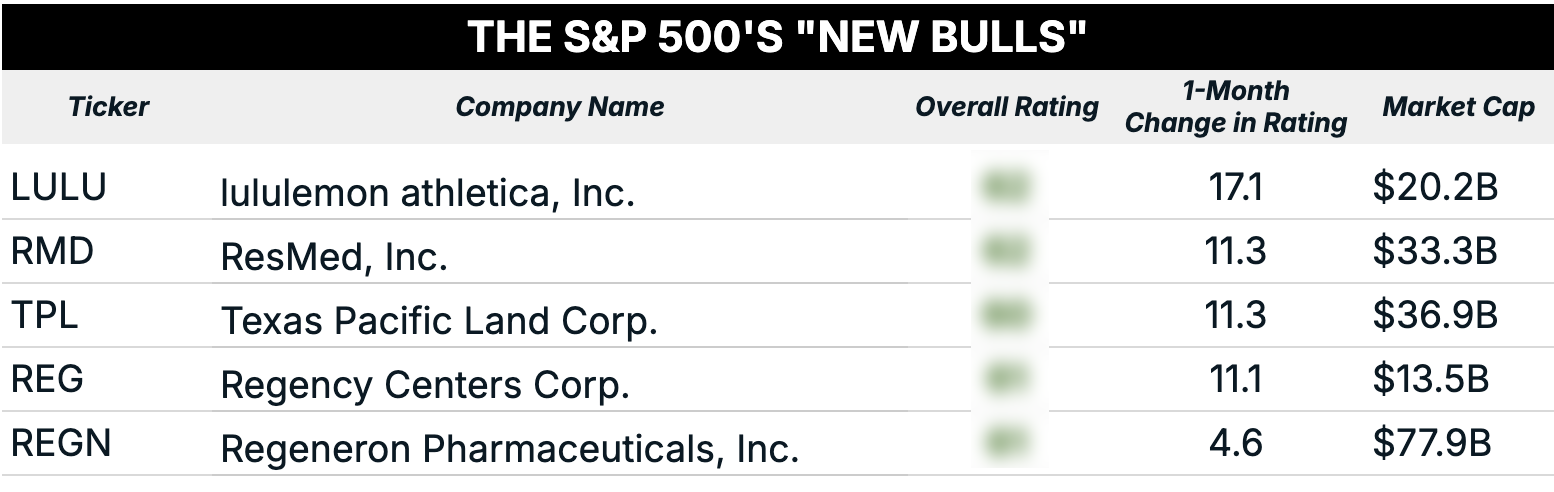

S&P 500 New Bulls

I ran my usual screen for S&P 500 Index companies that popped up as “Bullish” this week, and this is what I came up with:

We have an interesting collection of companies making the cut this week. At the top of the list, seeing its Green Zone Power Rating jump by 17 points, is athleisure pioneer Lululemon Athletica (LULU).

It seems like a lifetime ago, but there was a time, before Lululemon came along, when it would have been considered strange to be seen walking around town in yoga pants or gym clothes. Today, it’s not unusual to see them in office buildings.

LULU’s rating gets more interesting the deeper you dig. Its “Bullish” rating is due completely to its “Strong Bullish” scores on its fundamental factors: a perfect 100 on quality, a 93 on growth and an 81 on value.

Meanwhile, it’s technical scores are abysmal. It rates a 26 on momentum, a 12 on size and a 12 on volatility.

What conclusions can you draw from this?

It tells us that Lululemon is a fantastic company… but it’s also a risky stock.

LULU shares have been trending lower for all of 2026, so you might want to wait for its price to stabilize and start trending higher before buying.

Texas Pacific Land Corp (TPL) is also an interesting case study.

The company traces its roots back to 1888, when Texas Pacific Land Trust was formed to hold title to vast tracts of West Texas land. The original idea was simple: sell off the land over time and wind things down. Instead, what happened is one of the greatest accidental business models in history.

Today, TPL owns roughly 882,000 surface acres in the Permian Basin, the most prolific oil patch on earth. But TPL is not an oil and gas producer… it’s a landlord. And TPL collects a toll on everyone else’s activity without ever having to pick up a drill bit.

TPL collects royalties from operators who extract oil, natural gas and related products from its land. It also leases out land for pipelines, power lines and materials like sand and gravel. Plus, the company supplies both fresh and recycled water for drilling operations and charges fees for disposing and transporting it.

The financial profile is almost absurdly lean. The company carries zero debt and ended 2025 with $145 million in cash. Its operating margin runs around 75%, and net margins approach 62%.

These are numbers you’d normally associate with software companies, not an old-timey Texas land trust… and they explain why TPL sports a quality rating of 99 out of 100. My quality factor is a composite of profitability, balance sheet strength and capital efficiency (being “asset light”).

And the story actually gets better…

At the end of last year, TPL committed $50 million to a partnership with Bolt Data & Energy, a firm co-founded by former Google CEO Eric Schmidt aimed at developing large-scale data center campuses on its West Texas land. At that moment, TPL stopped being just a West Texas “oil story” and became an AI infrastructure play. And the stock reacted as you might expect, blasting higher by more than 80% this year.

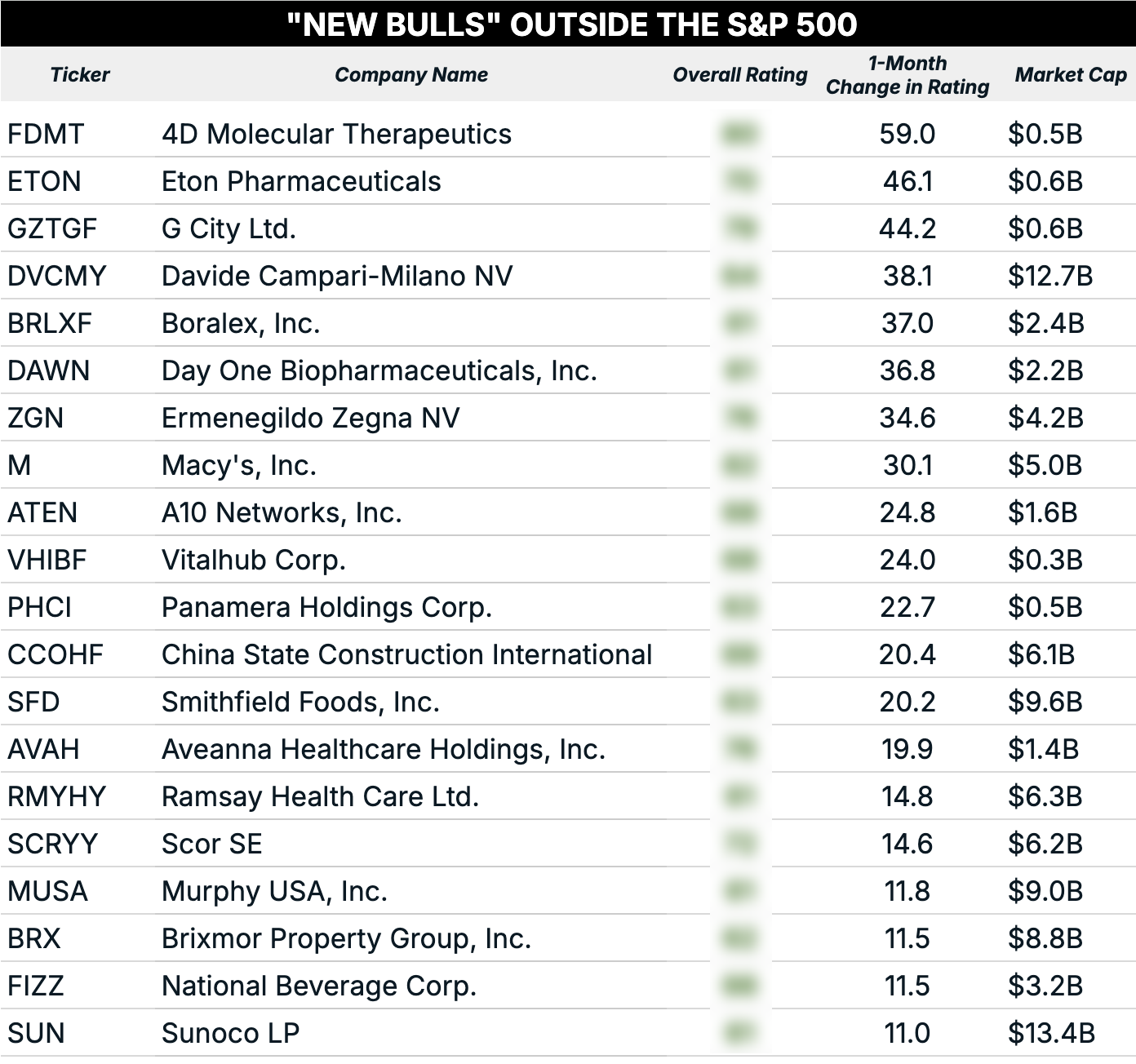

New Bulls Outside the S&P 500

Let’s cast the net a little wider and look at the newly “Bullish” stocks outside of the S&P 500.

I ran a screen for the top 20 stocks with the largest score increases over the past month.

As I’ve commented for the past several weeks running, brick-and-mortar retail has been trending “Bullish.” Department store chain Macy’s (M) continues that trend, as its Green Zone Power Rating jumped 30 points over the past month. Macy’s now rates as “Strong Bullish” and has a particularly strong value factor rating at 99.

Italian fashion house Ermenegildo Zegna (ZGN) also made the cut, continuing the retail theme.

One noteworthy addition this week is National Beverage Corp (FIZZ), the maker of LaCroix sparkling water.

I have a soft spot for National Beverage…

It’s one of the most successful trades in the early days of my Green Zone Fortunes investment newsletter.

I recommended it back in December of 2020… and sold half the position at a 100% profit just five weeks later. When I originally made the recommendation, I believed that the shares would be the potential beneficiaries of a short squeeze, and that’s exactly what happened.

Those conditions don’t exist today, and I wouldn’t expect to double my money in five weeks. But FIZZ is still a solid “Bullish” rated stock with an exceptional quality rating of 99.

It’s not hard to see where it comes from.

National Beverage is a case study in branding. It costs the company practically nothing to make sparkling water. But it can add a splash of fruit flavor, slap a branded label on it and then sell it at a premium price. It’s a license to print money.

Not a bad business model!

To good profits,

Adam O’Dell

Editor, What My System Says Today