With oil prices surging into the end of this week on the back of a number of tweets by President Donald Trump, it’s important to take a quick look at the backdrop of this and what it may mean for the future of oil and the global politics it affects.

One of the subplots of the Trump administration has been the president’s desire to be the price-setter in oil, rather than the price-taker. Trump’s formative years as a businessman and adult were the oil shock years of the 1970’s.

And they had a big impact on his thinking about creating a U.S. independent from foreign energy sources. He believes strongly in surging U.S. production as a strategic strength, and has gone to extreme lengths to protect it and help it gain market share globally.

In fact, you could make the credible claim that nearly all of Trump’s controversial decisions in foreign policy were in service to this end. His extreme antagonism of China, Russia, Iran, Europe and Venezuela all fit this thesis.

So it should come as no surprise that Trump returned to the issue of oil prices very quickly once the COVID-19 pandemic became something stressing the U.S. economy to the hilt.

Trump and Putin: Unlikely Allies Against OPEC

He’s been on the phone with all the major players trying to get them to discuss a new balance in the oil markets. And he may have found an unlikely ally — Russian President Vladimir Putin.

It is hard to underestimate how important it is for Trump and Putin to come to a deal over sending medical aid to the U.S. so quickly and easily. It shows real humility on Trump’s part, and great humanity and political acumen on Putin’s.

And this is why I’m intrigued by the sudden turn of events which now has oil prices putting in a significant counter-trend rally back into the mid $30’s for Brent Crude.

There’s a lot of smoke that Putin and Trump have agreed to significant production cuts on global supply, more than 10 million barrels per day. But with U.S. production not slacking off for months due to the nature of unconventional drilling, the big question is where are these cuts going to come from?

China is beginning to emerge from its COVID-19 lockdown and production there is picking up. Reports I’ve seen have them preferentially buying Russian oil over that of the Saudis, regardless of price.

Trump has obviously put the pressure on Saudi Crown Prince Mohammed bin Salman to reconvene OPEC+ and get them to the table to discuss a cut. That meeting, according to TASS, may happen next week.

The fact that the rest of OPEC is willing to meet but the Russians, officially, are not committing to any further meetings should tell you who holds the balance of power here.

Trump needs the oil and gas industry to stay reasonably solvent, not only through the election but into his potential second term. If he is to complete the realignment of domestic distribution, which will see the U.S. import less than it currently does — even though it is a net exporter — he needs more time.

Moreover, Russia was there for Trump with much needed help while Americans are dying from COVID-19. He’s attacking the Chinese on every front rhetorically and the Chinese are giving as good as they get, unfortunately.

It speaks to a new Cold War brewing.

So Putin now emerges as someone Trump can do business with when the chips are down. He found out Putin’s character when presented with a real crisis while MbS reacted with belligerence and, worse from Trump’s perspective, incompetence.

MbS has been incapable of wrangling OPEC into any kind of regional force. He’s started a price war while Trump is paying for defense of his oil fields from Yemeni attacks.

So, right now it seems to me the perfect opportunity for Putin and Trump to put MbS and the rest of OPEC in its place and dictate terms as to how the oil markets of the future will look. A lot rests on next week’s OPEC+ meeting. I don’t expect Putin to give the Saudis an inch.

It’s not in his or Russia’s best interest.

Cutting 10 million barrels a day from global production may be necessary, but it also means the potential for regime change in a lot of these nations as oil is their lifeblood. And without that revenue there is little to stop social unrest from overwhelming them.

So, giving the market hope that there is a light at the end of the tunnel and not a flood of oil is the right message to peddle at this point, even if it is a bit premature or unrealistic.

Where Oil Prices are Headed

The bottom line is, however, don’t believe this bounce in oil will signal the return to $50 to $60 per barrel anytime soon. At the same time, don’t believe the doom porners who are calling for $4 to $8 per barrel either.

This is a dead cat bounce in oil prices that comes as a result of a move into Q2, and traders lifting shorts after booking profits or meeting marginal calls. The next leg of this bear market will be the most interesting. It will tell the tale of where we’re headed.

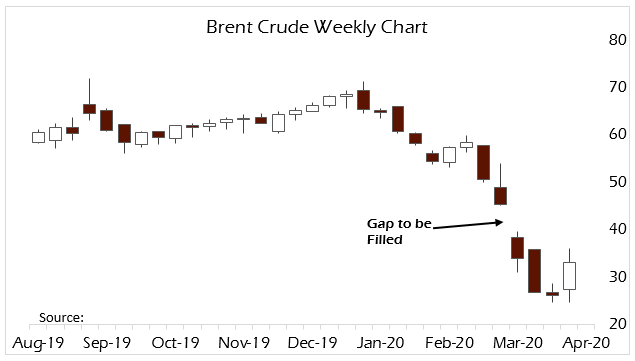

I would watch carefully for how this rally ends and at what price. There is a gap on the weekly chart of Brent Crude that takes it all the way back to $45.27. Markets hate gaps. It will take a weekly close above that gap to make me rethink my position here.

Anything below that level and there’s no new “bull” market on the horizon. But there will be a concerted effort to get you to think there is. Every little move by Trump, Putin and OPEC will be reported on to bring hope rather than reality.

The COVID-19 global lockdown will necessitate a significant production cut globally. I’m sure Putin will be willing to take his share offline with a guarantee from Trump, who he doesn’t trust, that some other concession will come Russia’s way.

The more these two men can agree on important issues like this, the more it bodes well for a more rational second term from Trump on the world stage. Trump has a long memory.

And helping him save not only lives in New York but jobs in Texas will be something he’ll remember.

• Money & Markets contributor Tom Luongo is the publisher of the Gold Goats ‘n Guns Newsletter. His work also is published at Strategic Culture Foundation, LewRockwell.com, Zerohedge and Russia Insider. A Libertarian adherent to Austrian economics, he applies those lessons to geopolitics, gold and central bank policy.