In addition to being highly volatile, the energy sector has been hammered by the COVID-19 pandemic so we have a list of four energy stocks to avoid right now.

Against the benchmark S&P 500, the energy sector has taken a beating.

Energy’s total returns year-to-date are a staggering negative 50.45% compared to the index’s negative 19.6% total returns.

With the outbreak of the coronavirus and the current oil price war, energy stocks have been battered to the point where some companies may not survive.

As an investor, while it’s important to know what stocks are good buys, it’s equally important to know what stocks to avoid.

That’s why we have our list of four energy stocks to avoid right now.

4 Energy Stocks to Avoid Right Now

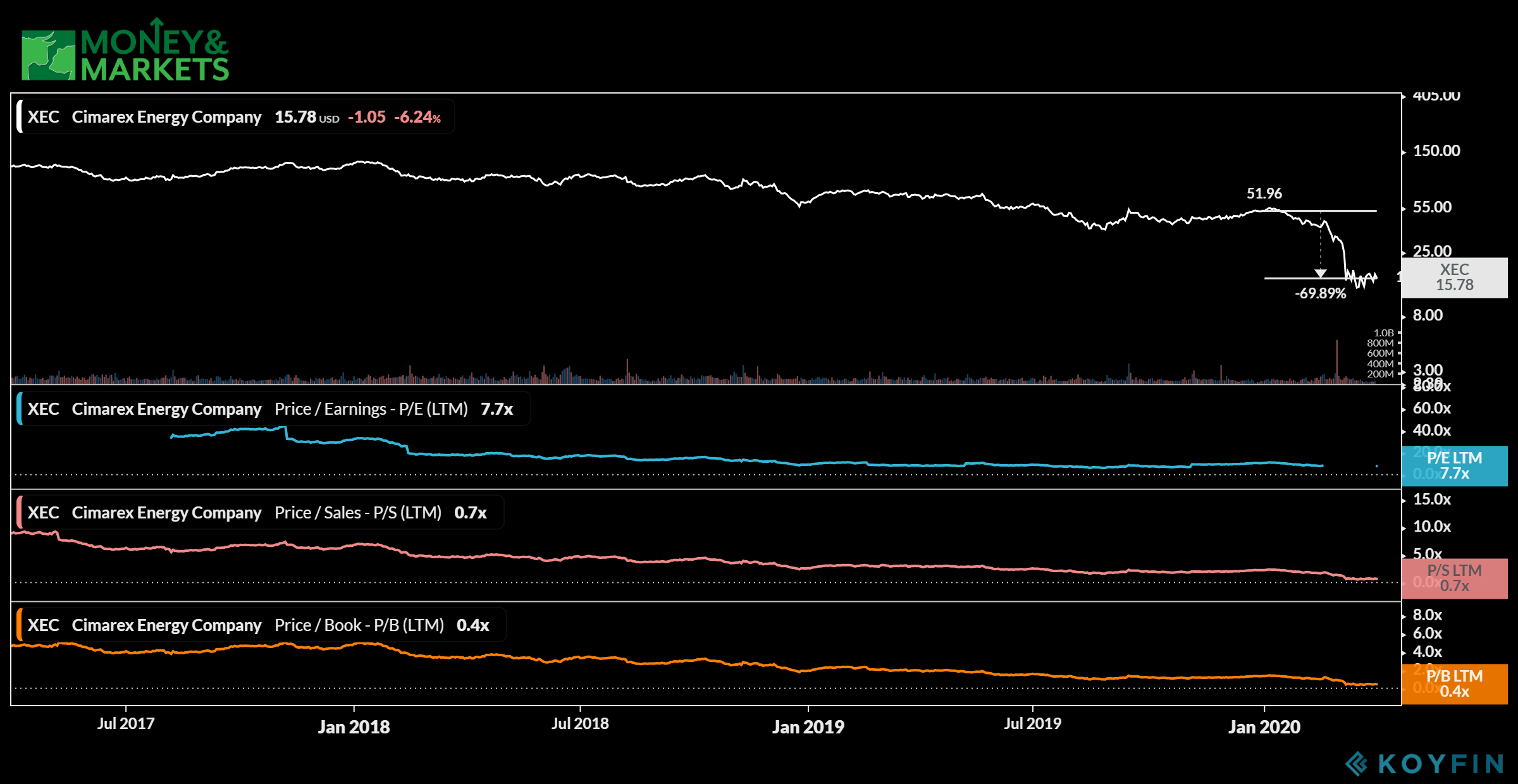

1. Cimarex Energy Corp.

Market Capitalization: $1.7 billion

Annual Sales (2019): $2.3 billion

Annual Dividend Yield: 4.75%

Denver-based Cimarex Energy Corp. (NYSE: XEC) is one of the many oil and gas companies that have significantly pared back capital investment due to market uncertainty.

In March 2020, the company said it expects a 40% to 50% reduction in its 2020 capital investment program from the original guidance of $1.25 million to $1.35 million.

Cimarex drills primarily in the Permian Basin, but the problem with demand for oil dropping means no one is buying what the company is selling.

But Cimarex’s problems started well before the COVID-19 outbreak.

Since January 2020, the company’s share price has dropped by almost 70%. That’s on top of the 15% decline it experienced in 2019.

Cimarex is extremely undervalued at the moment with a price to earnings at 7.7, price to sales at 0.7 and price to book at 0.4.

However, the longer the oil price war and coronavirus outbreak continue, the more pressure it will put on Cimarex stock.

That’s why Cimarex Energy Corp. is one of the four energy stocks to avoid right now.

2. Chesapeake Energy Corp.

Market Capitalization: $337 million

Annual Sales (2019): $8.5 billion

Annual Dividend Yield: 0.00%

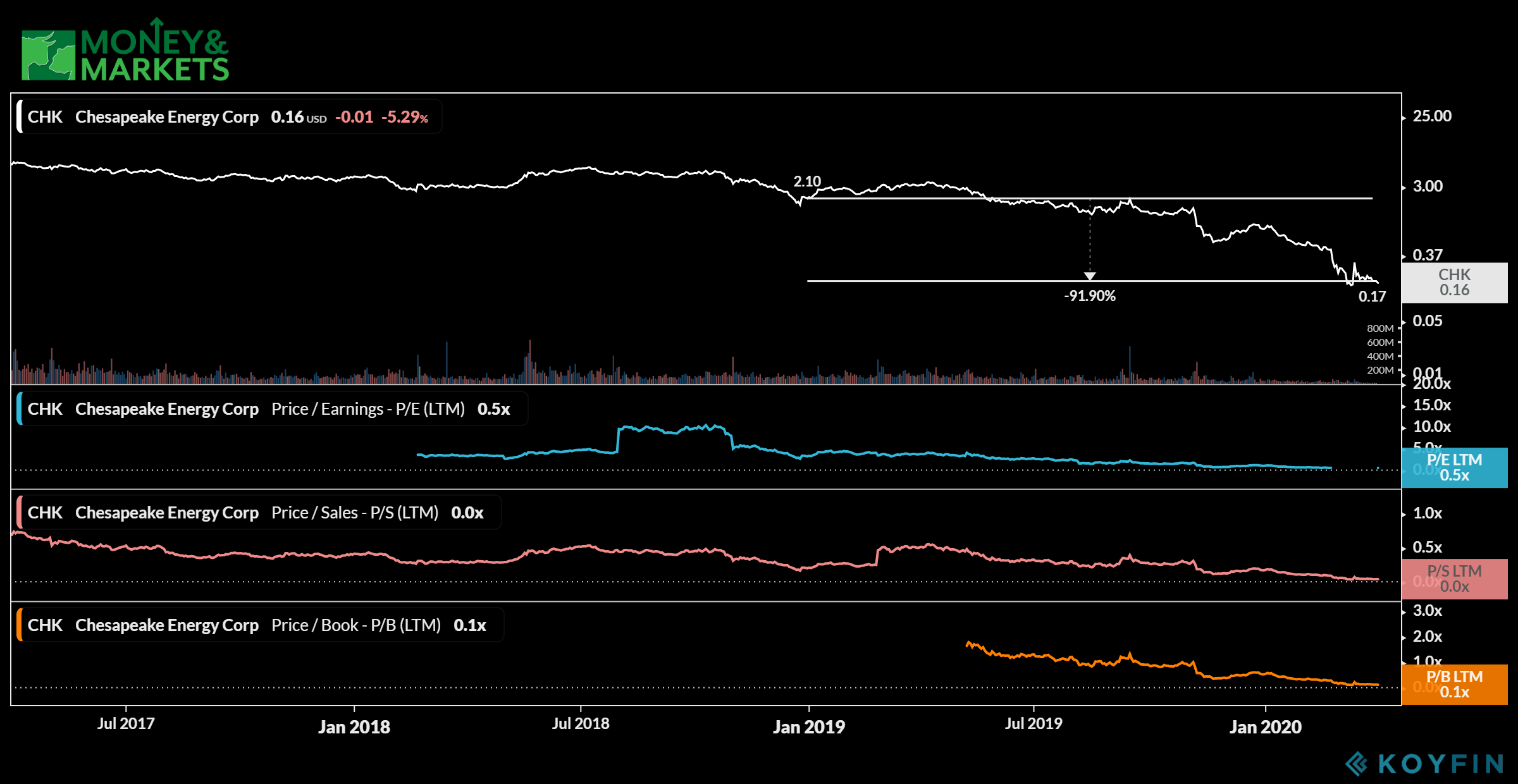

One of the most active drillers of new oil wells in the U.S. is Chesapeake Energy Corp. (NYSE: CHK).

It is the second-largest producer of natural gas and one of the top 15 in oil and natural gas liquids production.

But the Oklahoma City-based company fell into hard times in 2019. Its balance sheet went negative after boasting a small profit in 2018. All of this happened before the coronavirus.

Because of the recent drops in oil and natural gas prices, Chesapeake shares have fallen into penny-stock territory, trading around $0.16 per share.

From 2019 to the end of March 2020, Chesapeake shares fell a whopping 91%. It was already on the decline when oil prices were over $50 a barrel. Things look even more rough with those prices hovering around $20 a barrel.

Another problem for Chesapeake is its debt. At the end of 2019, the company reported outstanding debt of $8.9 billion — up almost $800 million from the previous year. It also borrowed nearly $1.6 billion from its credit facility.

It’s going to be extremely difficult to pay all of that debt off, especially as oil and natural gas prices continue at the bargain-basement level they are at.

That’s why Chesapeake Energy Corp. is one of the four energy stocks to avoid right now.

3. Transocean Inc.

Market Capitalization: $710 million

Annual Sales (2019): $3 billion

Annual Dividend Yield: 0.00%

In 2019, Transocean Inc. (NYSE: RIG) had an annual income of negative $1.25 billion — and 2020 isn’t looking any better.

Based in Switzerland, the company specializes in international offshore contract drilling services for oil and gas wells. Basically, if you are looking to drill for oil in the ocean, you’d likely call Transocean.

That made for good business when oil prices were high. But, but with the recent drop, the phone isn’t likely ringing as much.

In 2019, shares of Transocean only fell about 15%, which isn’t bad in comparison to some of the other companies on our list. However, since January 2020, the stock price has cratered by more than 84%, putting Transocean close to under $1 per share.

The company lost about $1.3 billion, or $2.05 per diluted share, in revenue last year and the recent drop in oil demand is putting a big strain on companies Transocean normally does business with.

Transocean CEO Jeremy Thigpen said in his quarterly statement the company is “mindful of the risks COVID-19 presents to near-term oil demand,” but no one knows just what “near-term” really means.

Because oil and gas companies have little need for new drilling operations, Transocean Inc. is one of the four energy stocks to avoid right now.

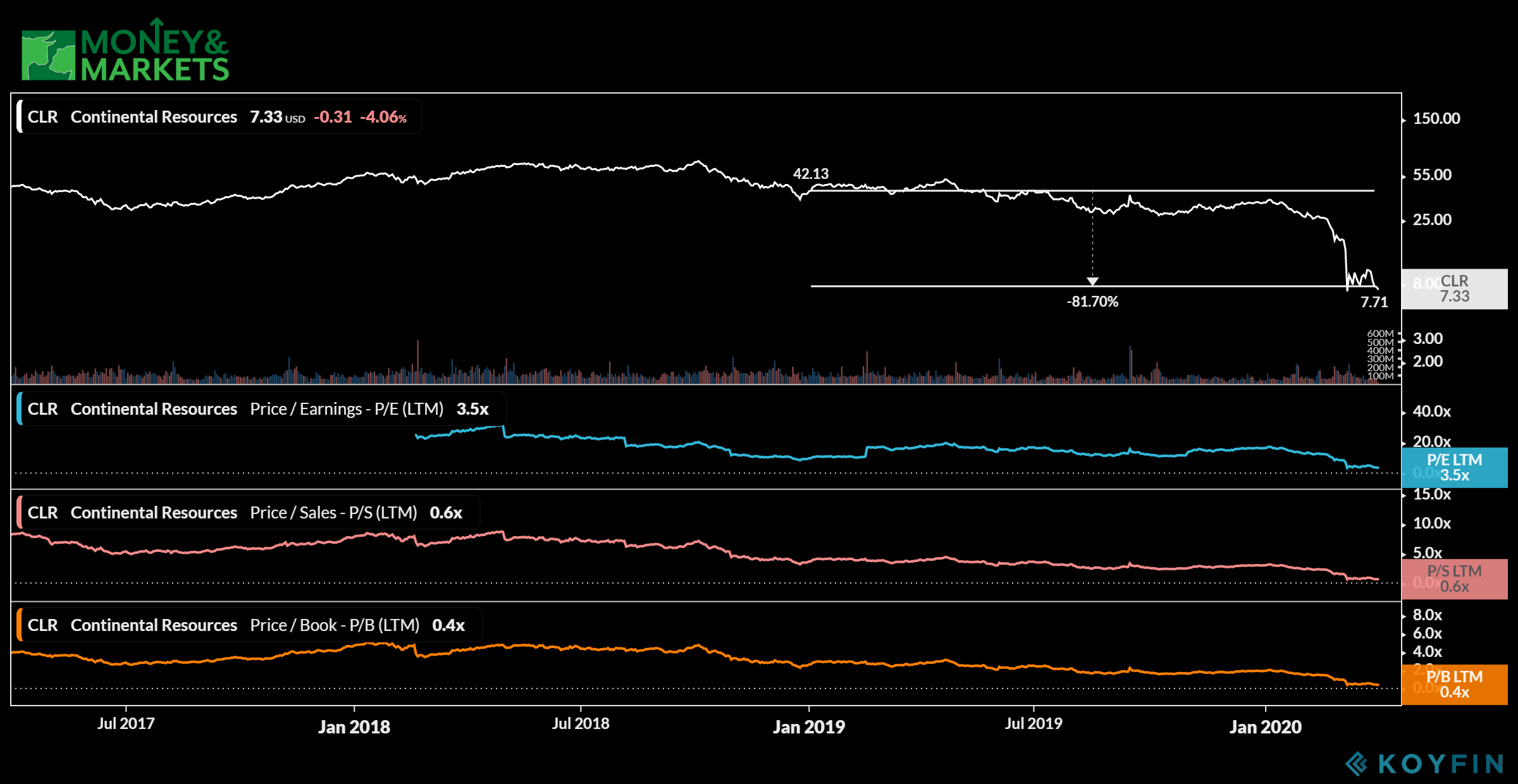

4. Continental Resources Inc.

Market Capitalization: $2.8 billion

Annual Sales (2019): $4.6 billion

Annual Dividend Yield: 2.62%

The biggest company on our list by market capitalization is Continental Resources Inc. (NYSE: CLR). Its market cap is close to $3 billion.

In 2019, Continental upped its oil production by 14%, specifically in the Bakken shale region of Montana. But the drop in oil prices has forced the company to significantly cut back in 2020.

In March 2020, Harold Hamm, Continental’s executive chairman, said the company was slashing capital expenses by 55% and its average rig count by two-thirds.

While the oil price war and COVID-19 have turned the company’s share price down in a hurry, it was already trending downward before.

From January 2019 to March 2020, the stock tumbled more than 81%.

With an immediate reduction in drilling and capital expenses, the stock is likely to continue trending downward for the immediate future.

That’s why Continental Resources is one of the four energy stocks to avoid now.

Editor’s note: Looking for stocks to buy not on our list or have some good suggestions? Let us know in the comments section below.

Related:

- 3 Stocks to Buy After the COVID-19 Crash

- 3 Defense Stocks to Buy in 2020 — Invest in These Bulwark Companies

- The 3 Stocks to Buy in a Bear Market — Now to Capitalize When Markets Turn South

- 6 Stocks to Buy and Hold for the Next Decade

- 3 Gold Stocks to Buy Now — Investing in the Precious Metal

- What Is the Best S&P 500 ETF to Buy?

- 3 Cheap 5G Stocks to Buy Right Now

- 4 Artificial Intelligence ETFs to Buy Now

- 5 5G ETFs to Buy Now

- 6 5G Dividend Stocks to Buy Now

- 4 Tech Dividend Stocks to Buy Now

- The 4 Cloud Software Stocks to Buy Now

- 4 Semiconductor Stocks to Buy Now

- 7 5G Stocks to Buy Right Now

- Top 5 ETFs to Buy in 2020

- 4 Stocks to Buy and Hold for 2020

- 5 Tech Stocks to Buy in 2020