Federal Reserve Chairman Jerome Powell made it official: The Federal Reserve will change the way it targets inflation because it is too low.

Fed officials believe inflation should average 2%. But why is that a good number?

According to one Fed official, there are three reasons the inflation target should be 2%:

- The Fed doesn’t think it does a very good job of measuring inflation. Economists think official measures overstate inflation. By targeting 2%, they argue, inflation is closer to zero in the real world.

- Higher inflation allows the Fed to cut interest rates. When inflation is low, interest rates are low. That makes it harder to fine-tune the economy.

- Economists believe that deflation (in the form of falling prices) is bad for the economy.

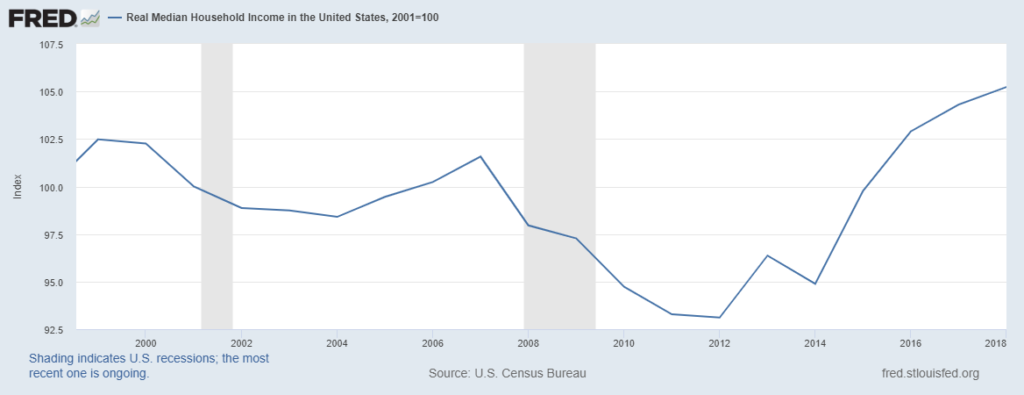

While these arguments make sense to an economist, many families will disagree that inflation is too low. The chart below shows that average incomes have only increased about 2% in the last 20 years. Not 2% a year — 2% in total.

Income Isn’t Rising Fast Enough

Source: Federal Reserve

Even with low inflation, the average household is exactly where it was 20 years ago.

How an Inflation Target Hurts Income

It might be a coincidence, but the Fed adopted its policy targeting 2% inflation, at least informally, around that time. It became an international standard for central bankers.

Prior to inflation targeting, economic growth was less stable. There were wider swings in both inflation and unemployment.

This may not be a problem. The safety net is stronger than ever and could be improved if the Fed allowed booms and busts to unfold.

However, real income growth averaged about 1% per year when the Fed responded to growth rather than actively tried to prevent it.

With more money, in the late 20th century, families were able to improve their standard of living.

Fed officials decided they will make decisions for families and limit upside potential while hoping to limit downside risks. It’s a gamble, but it’s one they’re willing to take for Americans who get no choice.

Michael Carr is a Chartered Market Technician for Banyan Hill Publishing and the Editor of One Trade, Peak Velocity Trader and Precision Profits. He teaches technical analysis and quantitative technical analysis at New York Institute of Finance. Mr. Carr is also the former editor of the CMT Association newsletter, Technically Speaking.

Follow him on Twitter @MichaelCarrGuru.