If you blinked in early April, you might have missed one of the sharpest reversals in recent memory.

Growth stocks — the same names that had been punished heavily since the start of the year — snapped back with force, as if the prior sell-off had never happened.

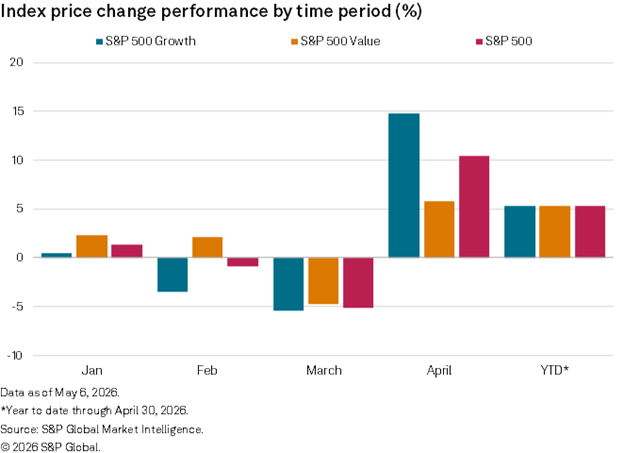

By month-end, the S&P 500 Growth Index had surged nearly 15% in April alone. Fifteen percent. In one month.

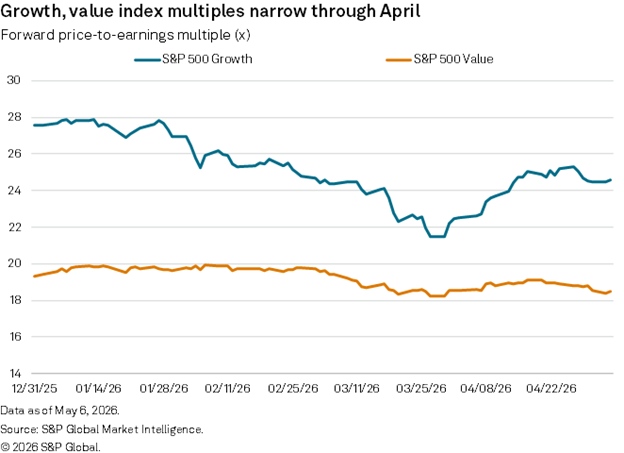

Meanwhile, the same stocks had been shedding multiple points off their forward price-to-earnings (P/E) ratios since December, sliding from lofty 27X to 28X to around 21X at the March lows.

That’s the story of 2026 so far — not one narrative, but two markets running side by side.

The first stage ran from January through March and belonged to value investors. They didn’t exactly win; they just lost less.

While growth stocks absorbed most of the drawdown, value held relatively steady, with forward P/E largely anchored in the 18X to 20X range .

February stood out as the only month where value stocks posted gains while growth stocks were sliding into the red – a quiet stretch of relative stability in an otherwise volatile period.

Then April happened, and the whole narrative flipped overnight.

April Was a Rocket Ship — But Only If You Were Holding the Right Stocks

The April bounce didn’t lift all boats equally.

Yes, the S&P 500 Index posted a stunning month, up about 10.5% — erasing most of the brutal losses from the first quarter. But growth stocks led the charge.

That roughly 15% monthly gain for the S&P 500 Growth Index compares with just 5% to 6% for the S&P 500 Value Index.

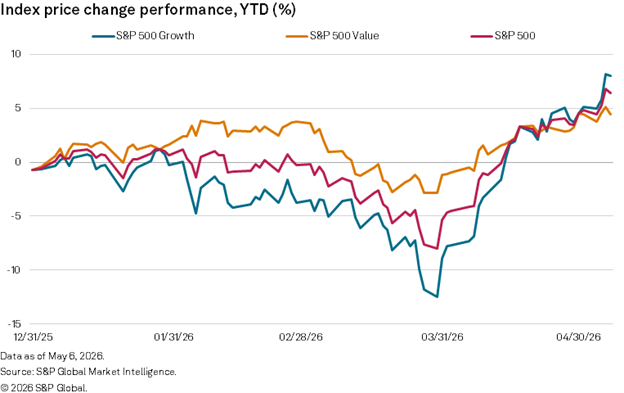

And when you zoom out to the full year-to-date (YTD) picture through April 30, all three indexes — Growth, Value, and the broad S&P 500 — were sitting in roughly the same neighborhood, up around 5%. They just got there using completely different routes.

That divergence matters more than the destination.

Growth stocks clawed back from a trough of nearly -13% YTD in late March.

Value, by contrast, never fell that far — its worst stretch was maybe -3% to -4% before recovering.

So while the scoreboard looks roughly even right now, the journey was a gut punch for anyone heavily concentrated in high-multiple growth names.

Think about the investor who panicked and sold growth in March. They missed a 15% jump in April. That’s the tax you pay for not having a plan when volatility strikes.

What drove the April surge?

A shift in sentiment around trade policy, some better-than-feared earnings and probably a healthy dose of short covering.

When the market decides it overshot on the downside, growth stocks — with their higher betas and more elastic valuations — tend to snap back harder than everything else. That’s exactly what we saw.

The Valuation Gap Is Narrowing, Which Changes the Calculus

Here’s the part of the chart that I keep coming back to.

Even after April’s massive bounce, growth stocks’ forward P/E has recovered to around 24X to 25X. That’s meaningfully lower than the 27X to 28X where the year started.

Value sits right around 18X to 19X — basically unchanged from where it opened in 2026. So the premium you’re paying for growth has compressed, but it hasn’t disappeared.

You’re still paying roughly six extra turns of earnings for growth over value. Whether that’s worth it depends entirely on what you believe the earnings trajectory will be from here.

This is exactly why Adam’s Green Zone Stock Power Ratings system doesn’t just chase momentum or screen for fast-growing names.

The quality and value ratings built into the system exist precisely for moments like this … when the market is swinging between extremes, and it’s tempting to just pile into whatever worked last month.

Quality metrics help identify companies with the financial durability to survive a March-style sell-off without permanently destroying shareholder value.

Value metrics keep you anchored to what you’re actually paying for a business, not just what the market is willing to pay in a given week.

The stocks that tend to score well across both quality and value are the ones that don’t make headlines when the market craters — and they don’t need to.

They hold their ground, preserve capital and let the high-flyers do their volatile thing.

And when the dust settles, you find out those quietly strong companies have been compounding along the whole time. That’s not a boring strategy.

That’s the strategy.

Until next time…

Safe trading,

Matt Clark, CMSA®

Chief Research Analyst, Money & Markets