Ernest Hemingway is known as a great author, but he’s also an expert financial analyst.

In his novel The Sun Also Rises, he explained how Silicon Valley Bank (SVB) failed.

One character asks another: “How did you go bankrupt?”

The answer describes the bank’s downfall: “Two ways. Gradually, then suddenly.”

The Gradual: Easy Money Flowed In

SVB’s failure started in 2009 when the Federal Reserve dropped interest rates to historic lows.

It accelerated in 2021 as low interest rates made it easy for the bank’s tech startup clients to raise money. They held that money in SVB’s coffers because they didn’t need it.

But SVB needed to put that money somewhere.

Managers decided to lock up billions of dollars in long-term bonds, the same bonds that will fall the most if rates rise. Banks have sophisticated risk models, and SVB’s models must have said: “buy.”

The Sudden: Tech Bank Runs

In 2022, the Fed raised rates. Tech startups couldn’t raise cash from investors anymore, so they drew down deposits. That meant SVB needed cash, so it sold some of those bonds at a large loss. This was the beginning of the “sudden” part of the bankruptcy.

Of course, there are thousands of other banks. It’s important to ask if they’re also on the verge of collapse.

Some are. Regulators have already shut down a couple of establishments. Traders are selling shares of others that they’re worried about.

But there’s something to keep in mind: The system as a whole should be able to withstand this crisis.

What’s Next for the Broader Banking System After SVB’s Crash

Banks can carry bonds on their balance sheet without acknowledging the losses. This is allowed when the bank plans to hold the bonds to maturity.

If banks sell the bonds, they face large losses. If managers even plan to sell the bonds, they must recognize the loss. That’s what happened at SVB. It was forced to sell bonds at a loss. This created the problem that led to its collapse.

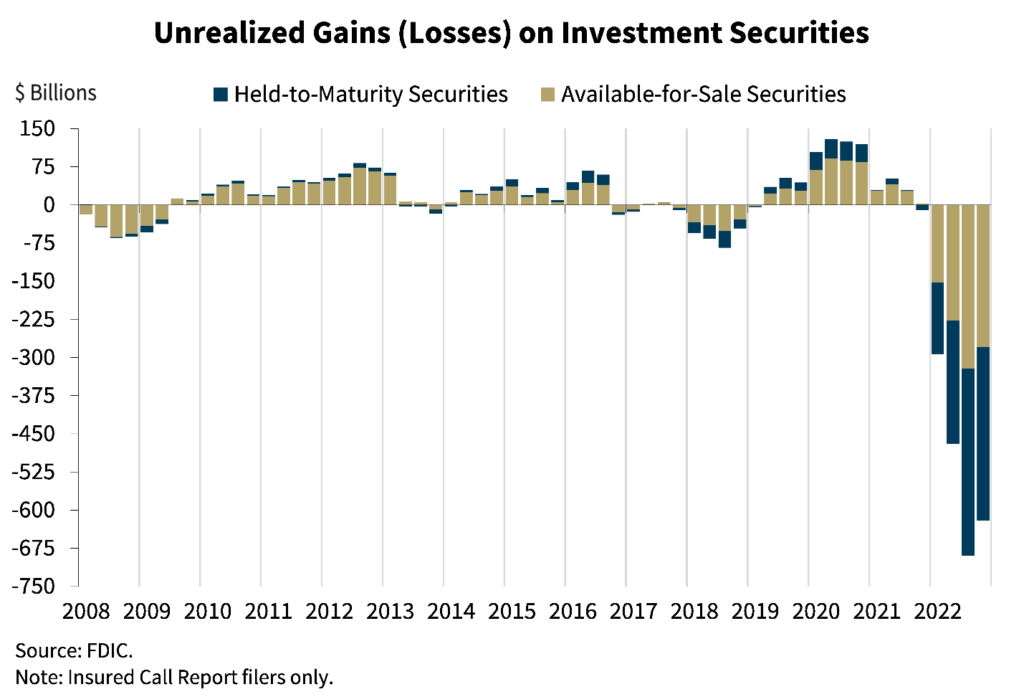

Other banks undoubtedly face the same problem. But the banking system as a whole should be able to weather the storm as the chart below shows.

Banks had about $620 billion in losses on bonds they owned at the end of last year. This might be closer to $700 billion now.

That sounds big, but banks own about $5.4 trillion in bonds. Losses represent about 11% of assets.

Big banks will hold the bonds to maturity and never recognize the loss. Small banks are the most at risk.

Regulators have stepped in. They agreed to offer loans based on the face value of the bonds rather than the market value. This lets the banks pretend the losses aren’t real. The Fed can then move the bonds to its balance sheet and allow them to mature so it’s not complete fiction.

Bottom line: With that decision, most banks should survive this stage of the crisis. Of course, the next stage that’s on the horizon will be more challenging.

If you want to know why, you need to check out my “Silicon Shakeout” presentation now.

Michael Carr, CMT, CFTe is the editor of two investment trading services — One Trade and Precision Profits — and a contributing editor to The Banyan Edge. He teaches Technical Analysis and Quantitative Technical Analysis at the New York Institute of Finance. Follow him on Twitter @MichaelCarrGuru.

Check out Mike’s latest insights in his Chart of the Week piece.