The stock market is taking a beating through afternoon trading on Thursday due to U.S. Treasury yields jumping, with the Dow, S&P 500 and Nasdaq indeces all down at least one percent or more about an hour-and-a-half before market close.

JPMorgan strategist Nikolaos Panigirtzoglou says investors shouldn’t panic and actually should remain bullish in the face of a little adversity in an interview with MarketWatch and a report to clients.

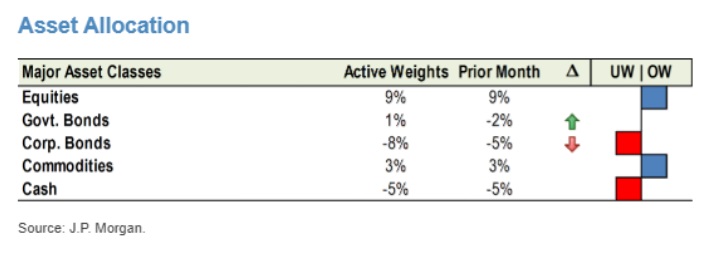

“We still recommend investors to be overall overweight equities vs bonds. The current selloff in bonds is helping this trade cushioning the decline in equities,” said Panigirtzoglou, a strategist at JPMorgan Chase & Co.’s London office.

Panigirtzoglou said investors should hedge positions by rotating out of corporate bonds and into government debt. He noted emerging risks like political unrest in Italy and the ongoing trade war between the U.S. and China.

Italy’s government is at odds with the EU over a budget deficit that exceeded EU regulations, and Washington recently levied an additional 10 percent in tariffs on Chinese imports that will rise to 25 percent on Jan. 1 if a new deal isn’t reached.

“With a hefty arsenal of hedges against the above risks, we are comfortable retaining a still large equity vs. bond overweight of 16% in our model portfolio, hoping that the third quarter outperformance in equities vs. bonds will continue into fourth quarter by encouraging both retail and institutional investors to resume or increase their equity buying,” said Panigirtzoglou in the report.

His bullish stock call will be a hard sell, MarketWatch notes, with the S&P 500 and Dow Jones on track for their worst day in months while the Nasdaq sinks about 2 percent.

Meanwhile, the 10-year U.S. Treasury yield BX:TMUBMUSD10Y+0.34% climbed 4.4 basis points to 3.20%, hitting its highest level since 2011, as robust economic data lend credence to the widespread belief that the Federal Reserve will remain hawkish to prevent the economy from overheating.