Most banks make money from loans. One way to do that is to borrow money at 2% and lend it to consumers at 12%.

This shows the potential profit in banking.

It also raises the question of how much banks pay to borrow and how they price loans to customers.

When banks pay a lower rate to borrow, their potential profits are larger.

That led to a rather unsophisticated scheme to cheat in pursuit of profits.

LIBOR Scandal

For many years, banks borrowed at the London Interbank Offered Rate (LIBOR). Only banks and large financial firms borrowed at LIBOR. This rate was among the lowest-cost source of funds available in the world.

Trillions of dollars change hand in this market. So, we would expect banks to set the rate based on risk and market conditions.

LIBOR proves finance isn’t always as sophisticated as we think it is.

To set LIBOR, an obscure organization called the ICE Benchmark Association calls 16 of the world’s largest banks and asks for “the rate at which it could fund itself at 11:00 a.m. London time with reference to the unsecured wholesale funding market.”

The highest and lowest values are thrown out, and the remaining answers are averaged. That’s all there is to determining the interest rate on the cost of an estimated $300 trillion in loans.

With trillions of dollars at risk, many of us would expect a rigid process. Instead, the bank is being asked to guess an interest rate that could have worked at 11:00.

Banks are allowed to make any assumptions they want to. They could make billions of dollars by guessing low. And they often did.

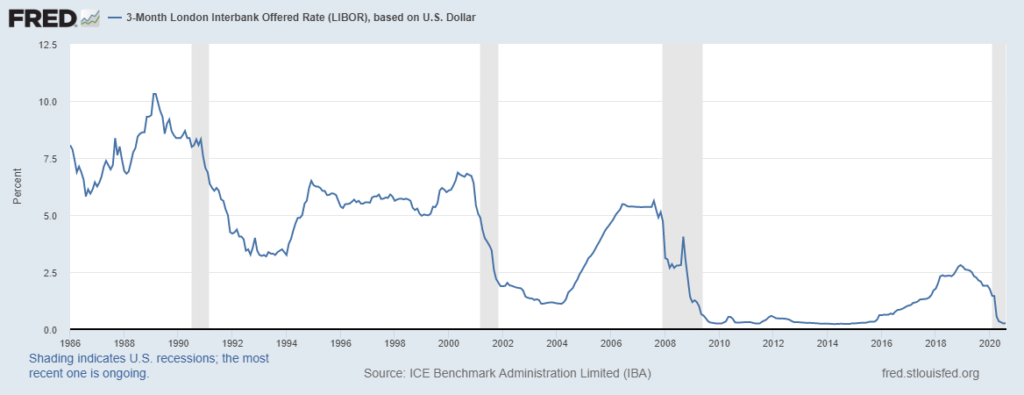

We know they were guessing because LIBOR is a smooth data series. Spikes are rare, even though market data tends to spike during crises.

LIBOR Doesn’t Spike Often

Source: Federal Reserve

After the 2008 financial crisis, regulators realized the data looked a little too smooth.

They asked if banks were making assumptions that favored their open trades. The answer was yes; bankers answer questions in ways that maximize their profits.

After catching banks cheating over several decades, regulators in the U.S., the U.K. and the European Union fined banks over $9 billion for rigging LIBOR.

LIBOR’s Replacement

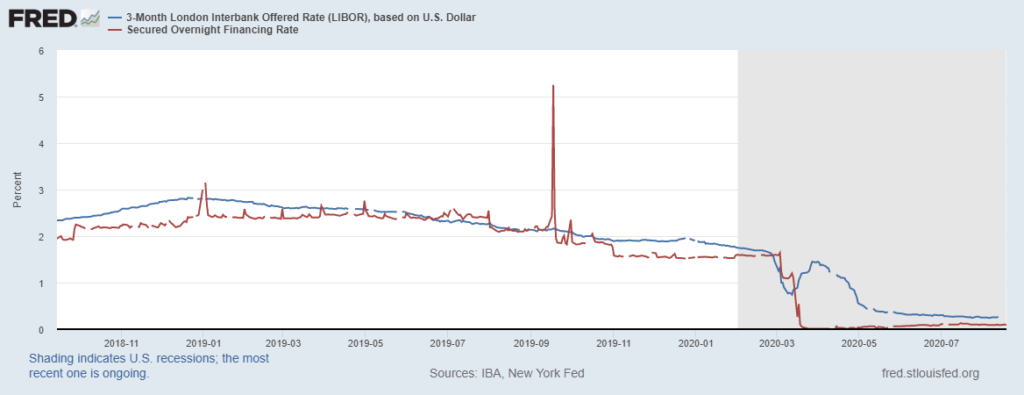

As part of the reform efforts to ensure we never see another crisis like 2008, LIBOR is being replaced by the Secured Overnight Financing Rate (SOFR) in the U.S. This is a market-based rate.

We now have about three years of SOFR history, and the index reflects market reactions much better than LIBOR.

SOFR: A Better Reflection of Markets

Source: Federal Reserve

And banks weren’t the only group caught cheating on price surveys. The Georgia Dock Price Index was a survey of poultry companies used to set the price of chicken. This index was also rigged to favor the biggest players in the market.

In the end, regulators tend to do the right thing. Unfortunately, they often do the right thing after consumers pay billions of dollars more than they should have.

Michael Carr is a Chartered Market Technician for Banyan Hill Publishing and the Editor of One Trade, Peak Velocity Trader and Precision Profits. He teaches technical analysis and quantitative technical analysis at New York Institute of Finance. Mr. Carr is also the former editor of the CMT Association newsletter, Technically Speaking.

Follow him on Twitter @MichaelCarrGuru.