In the long run, fundamentals matter in all financial markets.

Stocks can be overvalued for a time. But eventually a price decline or a surge in earnings reverses that condition.

Bonds can also be overvalued or undervalued. In these markets, analysts focus on cash flows instead of earnings to determine value.

Just as in the stock market, cash flow is measured with inflows and outflows.

In the municipal (muni) bond market, inflows consist of tax revenues. Outflows are expenses for government services.

A security could be undervalued, for example, if a tax increase is about to be implemented, that will ensure a state can repay its debt. If revenues decline suddenly, the bond could be overvalued.

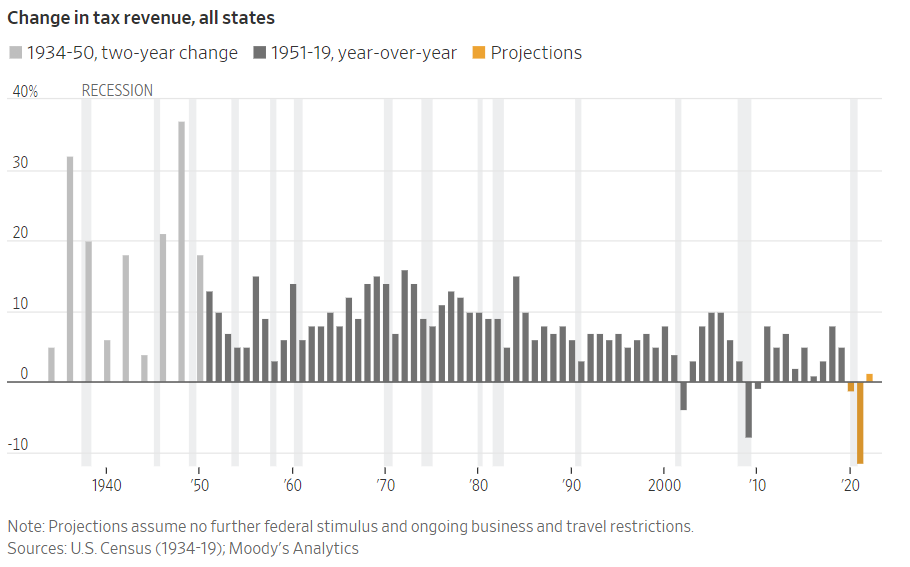

Over the next few years, inflows for states should fall. The chart below shows that revenue is expected to drop by more than 11% in 2021.

Tax Revenue Should Fall in 2021

Source: The Wall Street Journal.

In 2022, a small increase of 1.2% is expected. Assuming these projections are accurate, at the end of 2022, revenues will be 88% of the 2019 level.

This has negative implications for the economy and the muni bond market.

According to The Wall Street Journal:

State and local governments spent or invested $3.1 trillion in 2019, equivalent to 14.7% of gross domestic product.

They employ 13% of U.S. workers, whose spending fuels economic growth and who help deliver essential services and safety-net programs, such as unemployment insurance and nutrition assistance.

Those safety-net programs will need more money in the current crisis, but revenue is decreasing at the same time. In other words, outflows will increase at the same time inflows decrease.

Muni Bond Investors Ignore the Risks

Analysts generally agree on these broad facts. But the municipal bond market seems to be ignoring them.

The iShares National Muni Bond ETF (NYSE: MUB), an exchange-traded fund (ETF) tracking the market is near record highs.

Muni Bond ETF Trades Near Record High

Source: Optuma.

Traders panicked in March as states faced a budget crisis. Promises of aid from the federal government and the Federal Reserve led to a recovery in the market.

The depth of the shortfall is coming into focus. Federal aid to states is likely to go to local services rather than bondholders. Fed relief is limited.

The risks in the muni bond market are high. Yet traders seem to be ignoring it. Put options on MUB are attractive. And avoiding municipal bonds entirely seems prudent.

Michael Carr is a Chartered Market Technician for Banyan Hill Publishing and the Editor of One Trade, Peak Velocity Trader and Precision Profits. He teaches technical analysis and quantitative technical analysis at the New York Institute of Finance. Mr. Carr is also the former editor of the CMT Association newsletter, Technically Speaking.

Follow him on Twitter @MichaelCarrGuru.