We’ve got a pullback-driven (and tax-free!) dividend opportunity waiting for us now, and we can thank the Federal Reserve’s looming rate hikes for it.

It’s a “safety first” closed-end fund (CEF) paying a 4.5% tax-free dividend and trading at a rare 8.4% discount to its “true” value.

This opportunity comes our way through municipal bonds, or “munis.” If you follow the market for these bonds, which are issued by state and local governments to fund infrastructure projects, you know that they’ve pulled back this year:

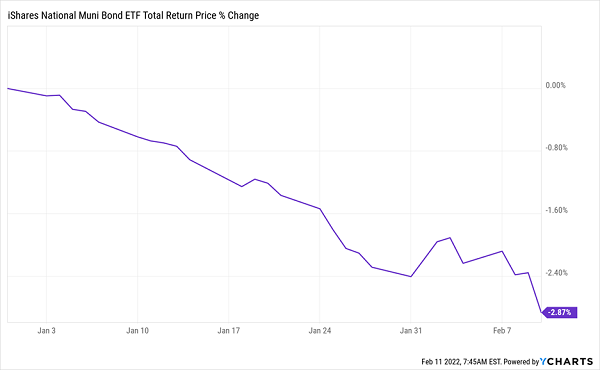

Munis Pull Back

Munis Slip, Giving Us an “In”

A 2.9% drop, as we see here in the iShares National Muni Bond ETF (NYSE: MUB), the benchmark exchange-traded fund (ETF) for the space, is small compared to the much bigger declines in stocks, but this is pretty rare: As an asset class, muni bonds are less volatile than other kinds of bonds, let alone stocks, which is why any short-term drop tends to be a buying opportunity.

And when you add this 2.9% decline to the 7.7% discount on the muni-bond CEF we’ll discuss in a second, it comes out to a 10.6% “double discount” on some of the safest investments around!

This “double discount” opportunity is particularly attractive when you look at the reason behind munis’ decline. As the Fed has made clear (and especially in light of last week’s hot inflation report), interest rates are going to rise in 2022. That tends to make bonds less desirable than in periods when rates fall.

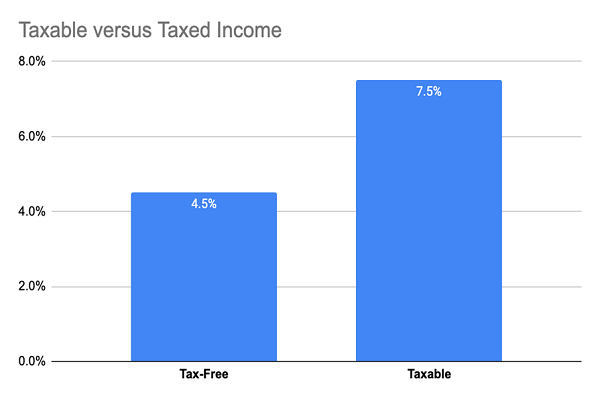

But there’s more to the story here, starting with muni bonds’ (and by extension muni-bond CEFs’) tax-free dividends. Right now, these funds already offer us high payouts of 4.5% and up. But thanks to their tax exemption, those payouts are worth a lot more to most Americans. Let’s say you’re in the highest tax bracket and you snag a 4.5% yielding muni-bond fund. After taxes, that’s the same money in your pocket as a 7.5% yielding stock!

Source: CEF Insider.

Let’s be honest: Even with the recent jump in Treasury yields, it’ll be a long time — if ever — before “safe” investments like Treasuries will be able to rival a payout like that.

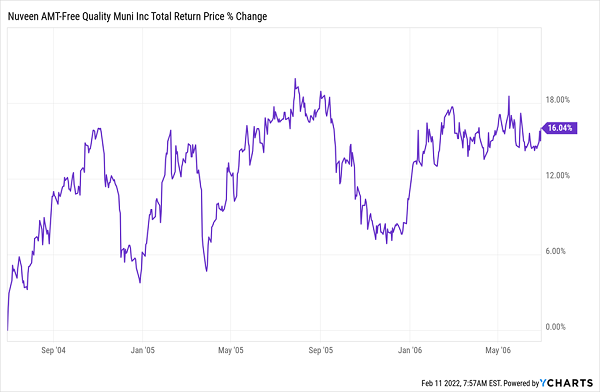

It’s only a matter of time before other investors realize this. And they will, going by historical precedent. Take the rapid rate-hike cycle that ran from 2004 to 2006. In the space of two years, the Fed raised rates from 1% all the way to 5.25%. An earthquake. And far higher than what we’re expecting this time around.

The benchmark ETF for municipal bonds, iShares Municipal Bond ETF (MUB) wasn’t around back then, but the biggest CEF in the space, the Nuveen AMT-Free Quality Municipal Income Fund (NYSE: NEA), which boasts a $4.4-billion market cap today, was — and it performed well.

Leading Muni CEF Did Fine in the 2004-2006 Rate Surge

And with history likely to repeat itself, now is a great time to get in.

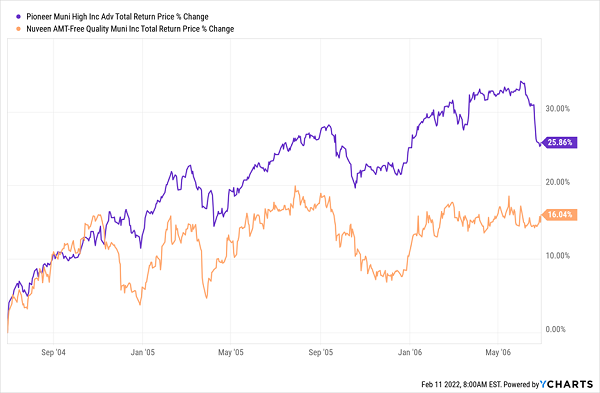

A good choice here is a CEF called the Pioneer Municipal High Income Advantage Fund (NYSE: MAV). It yields 4.5% today, which, as mentioned above, is actually 7.5% if you’re in the highest tax bracket. That’s far ahead of Treasury rates and the S&P 500’s paltry 1.3% payout, too.

And in our 2004-2006 test period it, too, defied rising rates and outperformed NEA:

MAV Soared the Last Time Rates Rose Fast

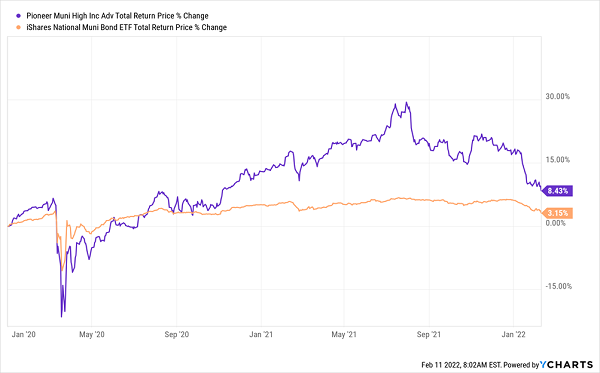

MAV’s payout also tops the 1.9% payout on the go-to muni-bond ETF, MUB, which is one reason to go with a CEF in a market like municipal bonds. Another is that muni funds’ managers often get the first call when new issues come out, which lets them grab the best ones. An automated ETF can’t match that advantage. MAV’s “human edge” has helped it outperform the benchmark during the COVID-19 crisis, with the latest pullback giving us a nice window to buy in:

MAV Outraces Its Benchmark, Then “Rolls Down” Our Buy Window

Thanks to its much higher income stream and management’s record of choosing the right bonds, MAV has outperformed by a wide margin — a margin that was much wider before the recent pullback in muni bonds broadly. That, in turn, makes MAV a compelling muni-bond CEF right now.

Add to that MAV’s 8.4% discount to net asset value (NAV, or the value of the municipal bonds in its portfolio), which is far more generous than the 3.7% average premium over the last decade, and MAV is an attractive buy during this rare downturn in the muni-bond market.

And MAV is just the start — there are even higher dividends waiting for us in muni-bond CEFs, with some even yielding above 5%, which obviously boosts your tax-free take even further.

To learn more about generating monthly dividends as high as 8%, click here.