Tesla stock has been on a upward tear after its most recent earnings report, and at least one analyst thinks it’s just getting started.

ARK Invest analyst Tasha Keeney updated the firm’s outlook for Tesla over the weekend and based on its valuation model, Tesla stock is on pace to hit $7,000 by 2024. That’s just the base case, too. A bullish outlook could send shares to $15,000, and even a bearish take shows positive growth to $1,500.

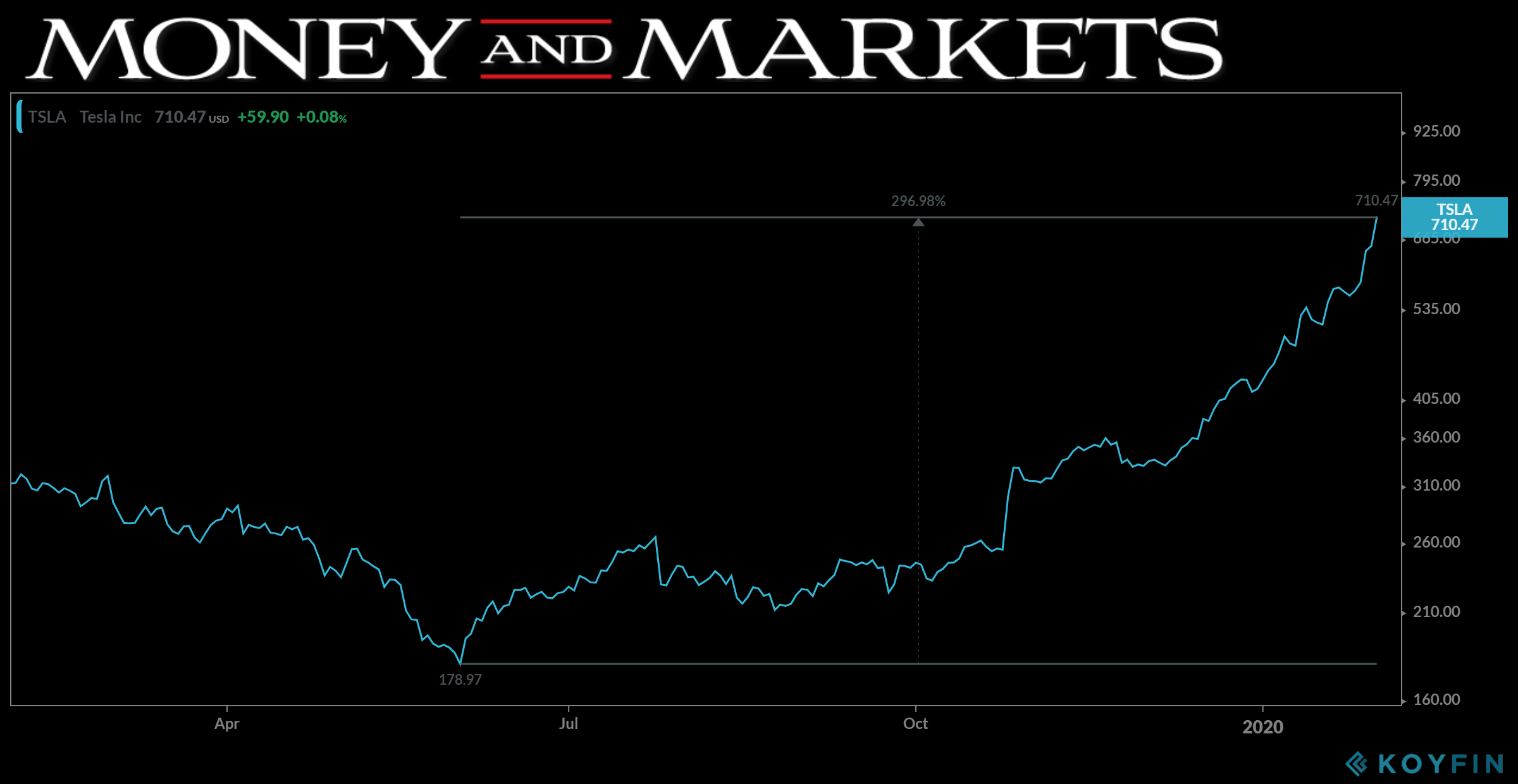

The stock continued its upward tear Monday morning with a 10% gain to $710 around 10:40 a.m. on the East Coast. By 3 p.m., it was up 16.7% to $759.06. Even the lowest valuation from ARK has the stock more than doubling that mark in five years.

Turning the calendar back to August 2018, ARK Chief Investment Officer Catherine Wood had written to Tesla CEO Elon Musk advising him not to take the company private after the stock hit $420 around that time.

“Tesla should be valued somewhere between $700 and $4,000 in five years,” Wood wrote in her letter. “Taking Tesla private today at $420 would undervalue it greatly.”

ARK, which is made up of active managers that handle a bevy of exchange-traded funds (ETFs) believes there are many factors that will drive Tesla’s value up, but there are three variables that are most important, per ARK:

- Gross Margins – Will Tesla’s cost of manufacturing vehicles continue to fall in line with Wright’s Law? If so, what will be the average selling price of Tesla’s vehicles?

- Capital Efficiency – What is Tesla’s cost per unit to build new production capacity?

- Autonomous Capability – Can Tesla launch a fully autonomous taxi service successfully?

Wright’s Law is a predictor that gauges cost declines over time as technology is further developed, and 80% of ARK analysts believe that the automaker can achieve 40% margins that are “consistent with a dominant brand that is an innovation cycle ahead of commoditized competitors.”

ARK analysts are most bearish on Tesla’s ability to build a fully autonomous car, with around 70% saying the automaker will fail.

When looking at capital efficiency, the high-end valuation of Tesla shows the company driving costs of factories down to $11,000 per unit volume of capacity. On the low end, ARK’s model has Tesla building factories at $16,000 per unit, which is $2,000 higher than the average gas-powered automaker today.

Wood’s broader evaluation of Tesla is that investors should look at the company as more than an automaker, and in her 2018 letter to Musk she called Tesla a “deep value stock today.” She compares it to Amazon two decades ago, because it is a revolutionary technology company that has the potential to become a player in many different sectors.

Wall Street as a whole is much more skeptical. FactSet’s average price target for the stock is $536, but most analysts in that metric only model around one year into the future.

Short sellers have posted major losses recently after Tesla’s shares soared in January. The automaker broke through the $500 barrier Jan. 13, and has continued to rocket upward after last week’s earnings report. Short sellers who bet against that rise lost almost $6 billion last month.

ARK isn’t betting against the company, though. Two of its ETFs that are heavily weighted with Tesla stock (Autonomous Technology & Robotics ETF and Next Generation Internet ETF) are up 15.7% and 27.4% respectively over the last 12 months.

It doesn’t look like Tesla is slowing down any time soon, so maybe it’s time to consider hopping on board.