I’ve been digging into hedge fund manager Paul Singer’s latest letter to his investors. Singer is more insightful than many pros, having delivered market-beating returns to his clients for decades, and one of his thoughts stands out.

Singer told his investors that:

“Trouble ahead” is signaled by a rare combination of low-quality securities, staggering valuation metrics, overleveraged capital structures, a scarcity of honest profits, a desperate dearth of understanding evinced by the most active traders, and economic macro prospects that are not as thrilling as the mobs braying ‘Buy! Buy!’ seem to think.

I’ve looked at the strength of low-quality securities, valuations and the scarcity of honest profits. Today, I want to review the problems associated with overleveraged capital structures.

Leverage means companies are borrowing money and expect future profits to be enough to pay off the debt and deliver an adequate return on investment. A little leverage can be good. Too much creates problems.

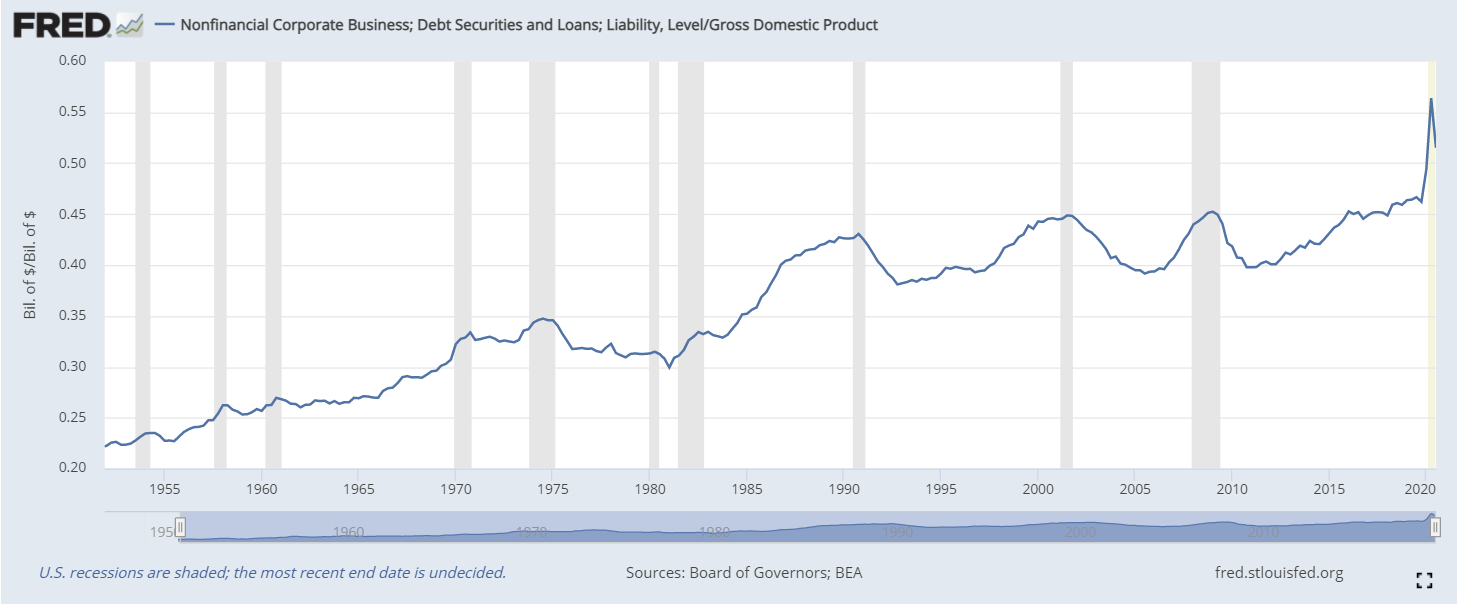

For companies, you can measure leverage by comparing the amount of debt to the value of the equity in the company.

For the economy, one measures leverage by comparing the amount of debt to the economy’s size. The chart below shows how much money companies borrowed as a percent of GDP.

Economic Debt as a Percentage of GDP

Source: Federal Reserve.

Investors Are Overlooking the Leverage Threat

By the end of 2019, corporate debt was at all-time highs. During the recession, companies borrowed even more.

Some borrowing makes sense. Low interest rates make debt cheap. But a significant amount of corporate debt is priced at variable rates — the cost of servicing these loans increases when rates rise.

Higher interest expenses will reduce earnings. It will also threaten the survival of companies that have low profit margins. That fight for survival could threaten the finances of stronger companies.

If a company is on the edge of bankruptcy, it may start a price war. Competitors could be forced to lower prices, which lowers their profits — reducing earnings for those companies and could lead to a stock market selloff.

Lowering prices will most likely only delay the inevitable, and weak companies will eventually go out of business — increasing unemployment and lessen the pace of economic growth. This could also lead to a stock market selloff.

Singer is right to be worried about leverage. This is a concern many investors are overlooking.

Michael Carr is a Chartered Market Technician for Banyan Hill Publishing and the Editor of One Trade, Peak Velocity Trader and Precision Profits. He teaches technical analysis and quantitative technical analysis at the New York Institute of Finance. Mr. Carr is also the former editor of the CMT Association newsletter, Technically Speaking.

Follow him on Twitter @MichaelCarrGuru.