Energy stocks have crushed every other major sector this year, with the State Street Energy Select Sector SPDR ETF (XLE) up over 33% as I write this.

And naturally, as the AI boom reaches euphoria, the tech sector is nipping at its heels.

The State Street Technology Select Sector SPDR ETF (XLK) is up 25%, with virtually all of that movement coming in the past two months alone.

After that, it’s essentially a three-way tie between the materials, industrials and real estate sectors, each of which is up a little over 10%.

Today, we’re going to zero in on real estate.

The State Street Real Estate Select Sector SPDR ETF (XLRE) was one of the strongest-performing sector ETFs last week, finishing 3% higher and muscling out the flashier tech and energy sectors.

So, why are investors suddenly warming to real estate investment trusts (REITs)?

It comes down to bond yields.

Along with utilities, REITs are traditionally the most “bond-like” of all major market sectors. When bond yields rise, bond prices fall… as do the prices of income-focused bond substitutes like REITs and utilities.

But when bond yields fall, the opposite happens. The prices of bonds and other income investments tend to rally.

Bond yields spiked following the onset of the Iran war, with the 10-year Treasury yield jumping from 3.9% to just shy of 5%. Over the past week, yields have fallen, giving the REIT sector a strong tailwind.

Of course, REITs are more than just interest-rate trades. They own real brick-and-mortar properties that throw off monthly rents.

So… what’s the story here?

Is the move in REITs sustainable? And should we consider jumping in?

Let’s do a deep dive into the sector to find out!

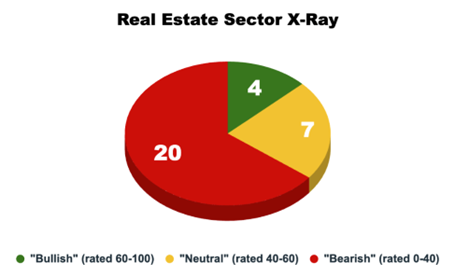

Taking a high-level view, REITs rate exceptionally poorly on my Green Zone Power Ratings system. Only four out of 31 rate as “Bullish,” meaning they have a score of 60 or higher out of 100. (For those new to my Green Zone Power Ratings system, “Bullish” rated stocks outperform the S&P 500 Index by double on average over the following year.)

Another seven rate as “Neutral,” meaning my system would expect them to perform more or less in line with the broader market. The rest rate as “Bearish.”

We should remember, though, that REITs aren’t like other companies. They have quirky accounting that tends to depress their Green Zone rating. Specifically, their debt levels (most real estate is mortgaged) and high non-cash expenses like depreciation tend to depress their quality, value and growth factors.

With that in mind, might there be a few hidden gems in the real estate sector?

Let’s keep digging.

Where Do REITs Pick Up Points?

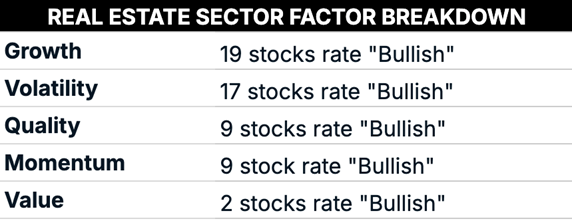

The Green Zone Power Rating is a composite score based on six primary factors: momentum, size, volatility, value, quality and growth, each of which is composed of several sub-factors. (As we are looking at large-cap constituents of the S&P 500, I don’t consider size when doing the sector X-ray.)

Let’s take a look at where REITs are putting points on the board.

It’s telling that, despite their handicap on the growth factor due to their quirky accounting, fully 19 out of 31 still rate as “Bullish” on growth. Another 17 rate as “Bullish” on their volatility factor.

The sector rates exceptionally poorly on value, but we know that this is normal for REITs given their unique accounting.

I’m most interested in the nine stocks that rate as “Bullish” on their momentum factor. It takes more than a strong week or two to generate a “Bullish” rating here. My proprietary momentum factor is a composite that covers multiple time horizons.

So, the REITs rating as “Bullish” here have managed to maintain their uptrends throughout what has proven to be a wildly chaotic year.

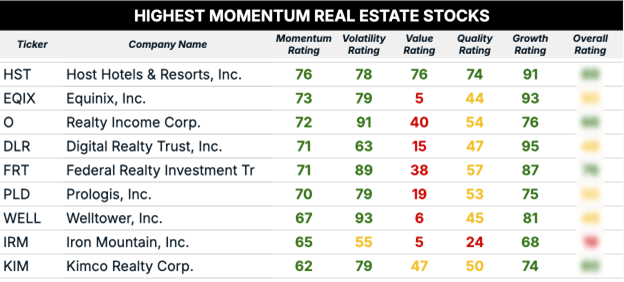

Below, I ranked the nine REITs that were “Bullish” on momentum by their momentum factor score.

The REITs Leading the Pack

One of these REITs is clearly head and shoulders above the rest. Host Hotels & Resorts (HST) rates as “Bullish” across all of its individual factors as well as “Bullish” overall.

I first mentioned Host Hotels back in February, and the shares are up a little over 13% since then. The shares have also paid a $0.20 dividend.

Host is interesting for multiple reasons. To start, it benefits from the “K-shaped” economy, in which wealthier, higher-income Americans continue to spend while middle- and working-class Americans are forced to scale back.

Its product is also scarce and hard to replicate. As I wrote back in February, “AI may soon create an economy of massive, virtually unlimited material abundance. But it can’t make a paradise on the coast of Hawaii appear out of thin air.”

The stock isn’t a super high yielder, but at 3.6%, its dividend is competitive with T-bills and other short-term bonds.

Given the bullishness toward tech, it’s not at all surprising to see Equinix (EQIX), Digital Realty (DLR) and Iron Mountain (IRM) rating strongly on momentum. Each of these REITs has a major presence in data centers. They’re essentially the landlords of the AI infrastructure boom.

Note that none of these three is cheap, however. Even in the world of REIT accounting, these data center REITs rate poorly on value.

To good profits,

Adam O’Dell

Editor, What My System Says Today