I’m being polite when I say that 2020 has been challenging.

It’s more accurate to say it’s been a punch to the gut, particularly if your business centers on anything in the entertainment and leisure segment.

When you hear that the COVID-19 pandemic “changed everything,” that’s not quite true. But it has massively accelerated trends that were always in place.

Take the retail apocalypse. The COVID-19 lockdowns didn’t kill the retail economy. Amazon.com Inc. (Nasdaq: AMZN) dealt the mortal blow years ago. The pandemic just finished it off with the coup de grâce.

Movie theaters? Similar story. COVID-19 didn’t bury the movie theater. It was Samsung (large-screen TVs) and Netflix (cheap, abundant content to stream) that crippled that industry. American movie theater attendance hit a 25-year low in 2017. That’s three years before the virus hit.

I could go on all day. But you get the point. COVID accelerated trends — it didn’t create them.

Enter the Fed’s Low Interest Rates

The Federal Reserve has been fighting the good fight to juice the economy. It is keeping interest rates anchored at zero and flooding the market with freshly-printed dollars.

This stopped the bleeding. The Fed’s moves stabilized the stock and bond markets and brought a little order to the chaos. But it didn’t do much to boost the real economy. And I don’t expect that it will.

It comes back to those trends that were already in place.

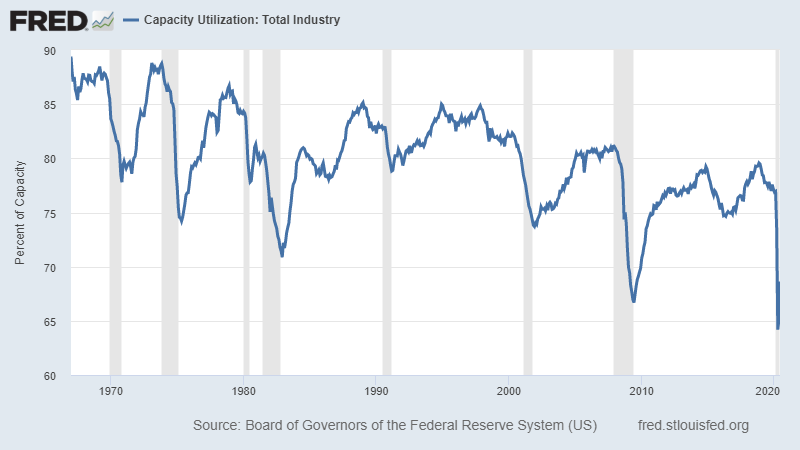

Manufacturing Took a Nosedive

Consider capacity utilization. If you don’t speak like an economist, don’t worry about it. You can think of this as the percentage of manufacturing capacity actually getting used.

Capacity utilization dropped like a rock earlier this year when the economy shut down. But it has been trending lower for decades.

After the tech wreck of the early 2000s, capacity utilization recovered. But it never returned to pre-crisis levels. The same happened in 2008. It hit multi-decade lows, and then never recovered to pre-crisis levels.

This gets us back to interest rates. Low interest rates are supposed to spur new production. But why would you build a new plant if you’re not using the one you already have?

The Fed’s low-interest-rate policy isn’t working as planned. Rather than spur new expansion plans, companies just hoard the cash or use it on buybacks. Why wouldn’t they? They already have too much of everything.

The Fed Has 2 Bad Choices

The Fed is painted into a corner. It can’t raise rates without destabilizing the stock market again. But keeping rates pegged at zero encourages more speculation and pushes asset prices higher.

I don’t envy the Fed. It has two bad choices:

- Break the economy now.

- Inflate the bubble even larger, and break it worse later.

It’s not a great situation.

As I’ve said for the past several months, I don’t particularly want to be a long-term investor in this situation. But there’s nothing wrong with trading this market and scalping profits along the way.

As I recently discussed with my colleagues Adam O’Dell and Matt Clark, I also think owning a little gold here makes sense. If we really are reaching the end of the road for modern monetary theory, owning some of the barbarous relic is smart.

• Money & Markets contributor Charles Sizemore specializes in income and retirement topics, and is a frequent guest on CNBC, Bloomberg and Fox Business.

Follow Charles on Twitter @CharlesSizemore.